Non-Forfeiture, Dividend, and Settlement Options

Non-forfeiture options

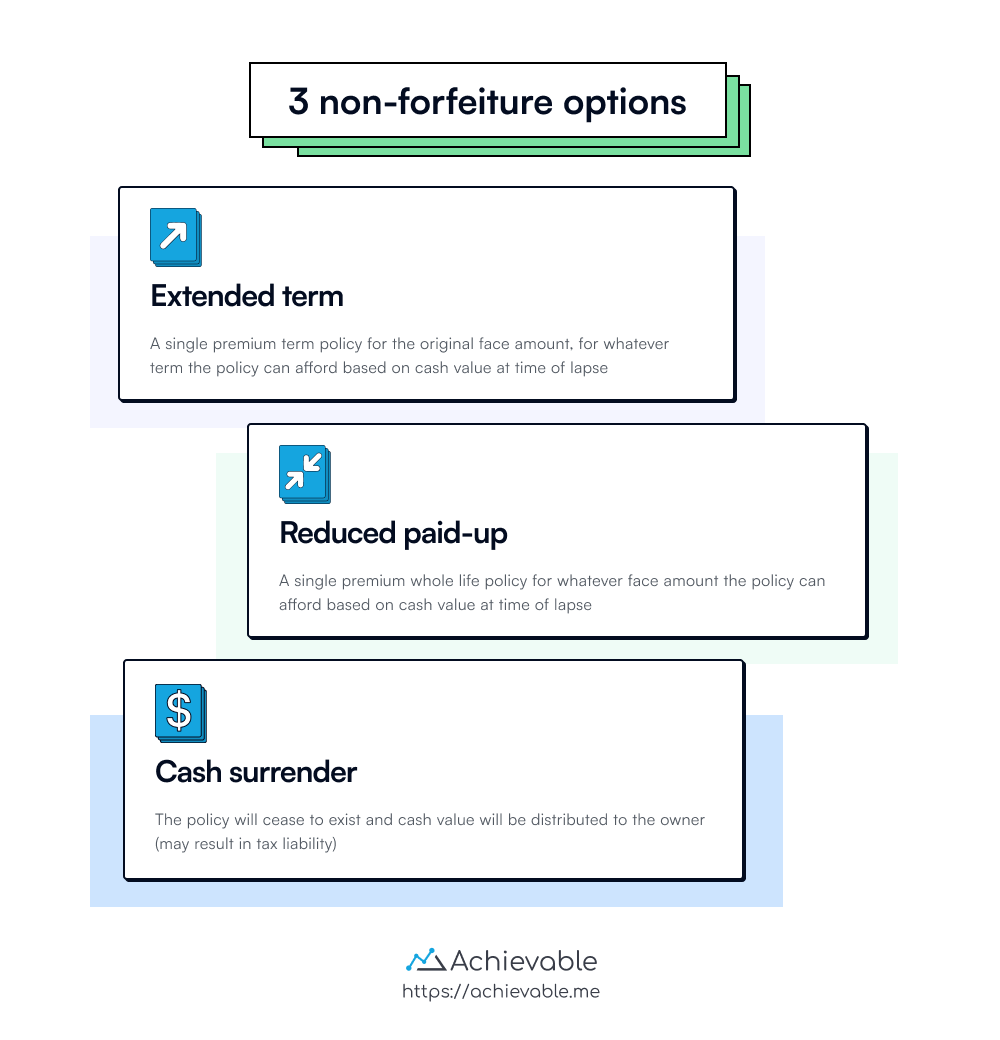

Non-forfeiture laws apply in every state, so they’re included in every whole life insurance policy. A non-forfeiture provision guarantees that if a whole life policy lapses or is canceled, the policy owner will receive a value equal to the policy’s cash value. There are three standard options:

Extended term

If the insurer doesn’t receive different instructions within 60 days after a policy lapses, the insurer uses the available cash value to purchase term insurance:

- The term insurance has the same face amount as the original whole life policy.

- Coverage lasts for as long a term as the cash value will buy.

Reduced paid-up

This option uses the cash value to purchase a paid-up policy of the same type as the lapsed policy, but with a lower face amount.

- No further premiums are due.

- The policy owner still owns a whole life policy.

Cash surrender

Insurers must make cash surrender values available after the third year for an ordinary policy, although most insurers make cash values available sooner. Insurers include a table of minimum cash surrender values in their policies.

Dividend options

As discussed earlier, mutual life insurance companies issue participating policies that may pay policy dividends. Dividends are surplus distributed to participating policy owners in proportion to the face value of their contract.

When setting premium rates, mutual companies intentionally overestimate their future funding needs. These overcharges:

- provide additional protection if operating costs are higher than anticipated, and

- help ensure that a dividend will be paid.

Policy dividends, unlike stock dividends, aren’t subject to personal income taxation because they’re considered a return of premium. Dividends can’t be guaranteed by an insurer.

A participating policy owner has several choices for how to receive or use a dividend. Common dividend options include:

Cash:

- The policy owner may elect to receive the dividend as a cash payment.

Reduce premium payments:

- The dividend may be used to offset future premiums.

Accumulate at interest:

- The dividend may be left with the insurer to accumulate interest. While the dividend is paid tax free, any interest received is taxable to the recipient as ordinary income.

Paid-up additions:

- The policy owner may use the dividends to purchase a single premium policy of the same type with no evidence of insurability.

One-year term:

- This option allows the insured to use the dividend to purchase a one-year term policy for whatever face amount can be obtained using the available dividend.

Settlement options

If a life insurance policy isn’t lapsed or surrendered for its cash value, it will eventually pay a benefit. Life insurance is unique because the covered peril is inevitable. In most states, life insurance companies must pay death claims within 60 days after receiving proper notification of claim. The beneficiary has several settlement options to choose from.

Cash:

- Most beneficiaries select this option and receive a tax-free lump-sum payment from the insurance company.

Fixed period:

- A specified amount is paid out regularly for a specified period of time. If the beneficiary dies during this payout period, the company continues payments to that person’s beneficiary for the remainder of the period. The payment amount depends on the face amount, the rate of interest, and the length of the payout period. Any portion of the payment attributable to interest on the death benefit will be taxable.

Fixed amount:

- This is similar to the fixed period option, except a predetermined payment amount is selected. Payments continue for as long as possible, based on the face amount and rate of interest.

Interest only:

- With this option, the proceeds are held by the insurance company, which pays a guaranteed rate of interest at specified intervals.

Life income:

- Instead of a lump-sum distribution, the life income option provides the beneficiary with a guaranteed monthly payment for life.

Lesson summary

Additionally, aspects of whole life insurance policies include non-forfeiture options, where policy owners receive a return upon policy lapse or cancellation:

- Extended term: Cash value is used to purchase term insurance after lapsing, for as long as the cash value allows.

- Reduced paid-up: Cash value is used to purchase a paid-up policy of lesser face amount, with no further premiums due.

- Cash surrender: Insurers provide cash surrender values after a specified period, allowing withdrawal of a portion of the policy’s value.

For participating policies that pay dividends, various dividend options are available to policy owners:

- Cash: Receive the dividend as a cash payment.

- Reduce premium payments: Offset future premiums with the dividend.

- Accumulate at interest: Leave the dividend to accumulate interest with the insurer.

- Paid-up additions: Use dividends to purchase a single premium policy.

- One-year term: Use the dividend to purchase a one-year term policy.

When a life insurance policy pays its benefit, beneficiaries have settlement options to choose from:

- Cash: Receive a tax-free lump-sum payment.

- Fixed period: Get regular payments for a set period, with benefits passed to the beneficiary if the recipient dies.

- Fixed amount: Receive predetermined payments for a specific period based on face amount and rate of interest.

- Interest only: Insurance company holds the proceeds and pays guaranteed interest at intervals.

- Life income: Receive guaranteed monthly payments for life instead of a lump sum.