Beneficiaries

Beneficiary designation

A beneficiary is the person or entity that receives the policy proceeds when the insured dies. Insurable interest rules don’t apply to beneficiaries. As long as the policy owner had an insurable interest in the insured’s life when the policy was issued, the beneficiary doesn’t need to have one.

For example, you could be named the beneficiary of a policy on the life of a distant relative even if you don’t have an insurable interest in that person.

Revocable vs. irrevocable

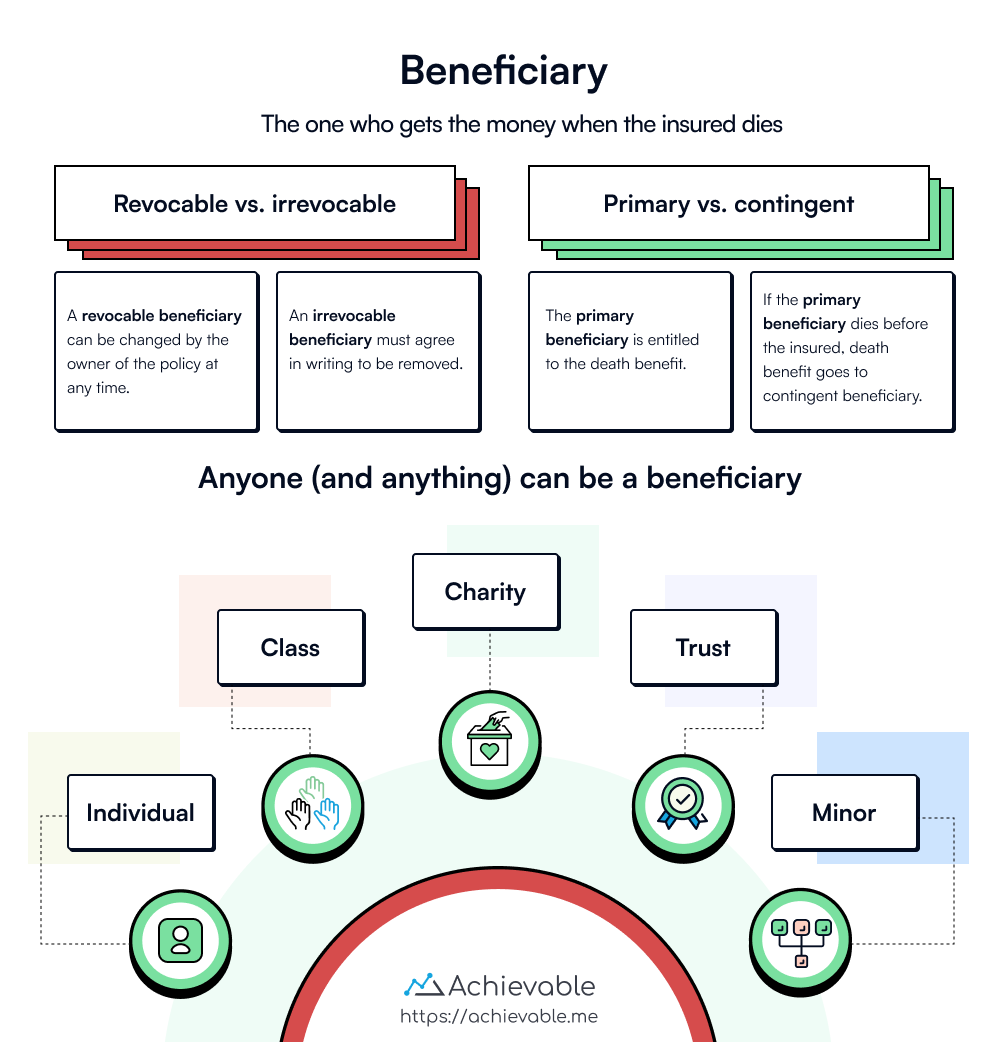

If a beneficiary is named revocable, the owner can change the beneficiary without the beneficiary’s consent. Because it offers flexibility, this is the more common designation.

With an irrevocable designation, the owner can’t change the beneficiary or assign the policy without the beneficiary’s permission. In this case, the beneficiary has a vested right to the policy benefits.

Primary vs. contingent

The primary beneficiary is the first person (or persons) entitled to receive benefits. If you name multiple primary beneficiaries, you can split the proceeds among them.

The contingent beneficiary receives benefits only if the primary beneficiary is deceased at the insured’s death. If both the primary and contingent beneficiaries predecease the insured, the final beneficiary is the insured’s estate.

Common beneficiary designations

Individuals:

- The most common designation is to name one or more individuals.

- If multiple people are named beneficiary, per capita and per stirpes are used.

- Under a per capita beneficiary designation, if one of the named beneficiaries pre-deceases the insured, the remaining beneficiaries divide that person’s share, in addition to receiving their own.

- Under a per stirpes (Latin for “through the root”) designation, the proceeds belonging to the deceased beneficiary don’t go to the other beneficiaries. Instead, they go to the deceased beneficiary’s heirs.

Class designations:

- Often used when several children are named beneficiary and the owner wants them to share the proceeds equally, such as “all my children,” rather than naming each child individually.

Estates:

- If no beneficiary is named, or if all named beneficiaries have pre-deceased the insured, the final beneficiary is the insured’s estate.

Minors:

- A minor may be named as beneficiary if a guardian or trustee is appointed to receive the funds on the minor’s behalf.

Charities:

- It is not uncommon for the owner of a life insurance policy to name a charity as beneficiary.

Trusts:

- Trusts are often established to receive proceeds from a life insurance policy. When a trust is named as a beneficiary, the trustee may manage the assets according to the trust terms but may not personally benefit from them.

Spendthrift clause

A spendthrift clause lets the policy owner choose a settlement option in which the beneficiary receives benefits over time rather than as a lump sum. It also prevents the proceeds from being assigned or claimed by the beneficiary’s creditors.

This clause is often used to protect beneficiaries from creditors or from poor money management.

Common disaster clause

Most states have enacted the Uniform Simultaneous Death Act. While details vary by state, the general rule is that if the insured and the beneficiary die at the same time, the death benefit is paid as if the insured outlived the beneficiary.

This prevents the death benefit from passing into the beneficiary’s estate (and then being distributed right back out), which can trigger unnecessary legal proceedings, costs, and estate taxes.

A common disaster clause typically adds a survivorship requirement: the primary beneficiary must survive the insured by a certain number of days (usually 30-90 days). If the primary beneficiary doesn’t survive for that period, the death benefit is paid to the contingent beneficiary.

Lesson summary

-

Beneficiary designation: The beneficiary receives the policy proceeds and may be named revocable or irrevocable. Beneficiaries can be primary, contingent, individuals, estates, minors, charities, or trusts.

-

Spendthrift clause: Offers a settlement option where proceeds are received over time and helps protect beneficiaries from creditors or poor money management.

-

Common disaster clause: Ensures that if the primary beneficiary does not survive the insured, the benefit will pass to the contingent beneficiary.