Variable Insurance Products

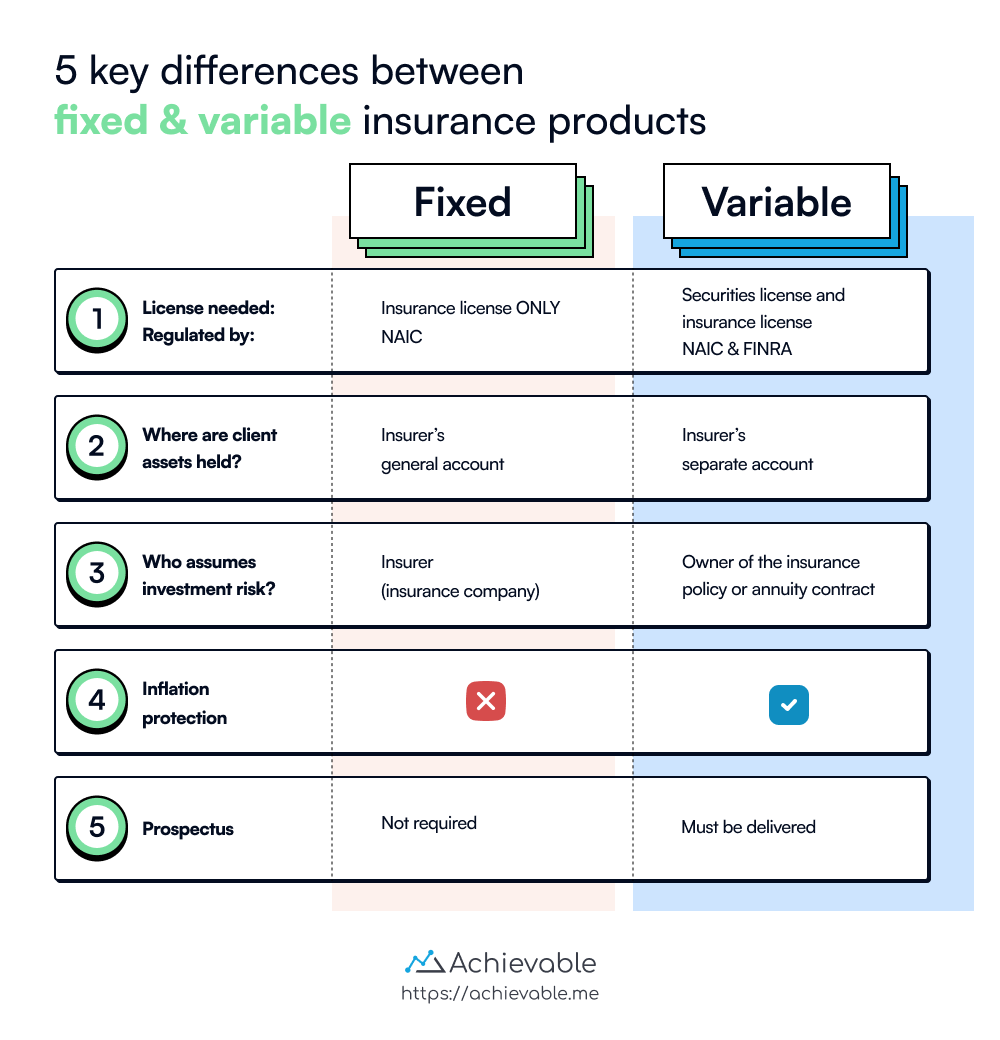

The differences between variable and fixed products are highly testable. The following 5 concepts summarize the key differences:

- Licenses needed/regulated

- Assumption of investment risk

- Separate vs. general account

- Variable contracts hedge against inflation

- Prospectus required with sale of variable contract

Licenses

The term variable contract includes variable life insurance policies and variable annuities.

- Variable contracts are insurance products, so they’re guided by the NAIC (National Association of Insurance Commissioners). An insurance license is required to sell them.

- Variable contracts are also securities, so they fall under the regulatory jurisdiction of the SEC.

Because variable contracts are both insurance products and securities, selling them requires:

- An insurance license, and

- A Series 6 or Series 7 investment license

Separate vs. general account

The assets in an insurance company’s general account are attachable by claims of the insurance company’s creditors.

- Premiums and cash values of traditional or fixed insurance products are held in the general account.

- If the insurance company becomes insolvent, those assets may be forfeited to the insurance company’s creditors.

A separate account is an investment fund kept separate from the insurance company’s general account.

- It is not attachable by the insurance company’s creditors.

- As required by the SEC, cash values of variable contracts are held in the insurance company’s separate account.

Assumption of investment risk

A fixed contract is issued with a stated rate of return (4%, for example). If the insurance company can’t earn 4% on the assets supporting the product, the insurer loses money.

Because a fixed contract has:

- A guaranteed rate of return, and

- A principal (cash value) that is guaranteed not to decline,

the insurance company assumes the investment risk.

With a variable contract, there are no guarantees as to rate of return or principal invested.

- The assets in a variable contract are invested in securities.

- As the market value of those securities fluctuates, the value of the contract fluctuates.

- The investor could lose some or all of their money.

All variable contracts must be convertible (at the discretion of the owner) into fixed contracts for at least 24 months from issuance. This accommodates investors who may not have initially understood the risks associated with variable contracts.

Hedge against inflation

Historically, the stock market has outpaced inflation. Theoretically, over an extended period, the market value of publicly traded securities will increase with inflation. As a result, variable contracts offer a hedge against inflation.

- If inflation is high, the return of a variable contract should increase due to the increase in the value of the underlying securities.

A fixed contract, by contrast, can produce a negative “real return” during periods when inflation exceeds the contract’s guaranteed rate.

- While the purchasing power of a fixed annuity increases during deflationary periods, a fixed rate can still lose purchasing power when inflation is higher than the fixed return.

For example, assume you have a fixed annuity paying a guaranteed rate of .

-

Inflationary period (prices are rising):

- Let’s say inflation is .

- Your annuity gives you a return.

- So, your real rate of return .

- Because prices are rising, your money buys less each year. In this scenario, during a period where inflation is , earning means you’re losing purchasing power because you aren’t keeping pace with inflation.

-

Deflationary period (prices are falling):

- Let’s say prices drop by per year (deflation ).

- Your annuity still gives you a return.

- So, your real rate of return .

- Because prices are dropping (which is rare in the real world), your money buys more every year. Purchasing power of a fixed return increases with deflation.

Prospectus

When an insurance company issues a variable policy or annuity (or when any other issuer sells a security), the transaction is called a primary market transaction.

Before securities can be offered to the public:

- A registration statement must be filed with the SEC. This announces the issuer’s intent to sell the security.

- Along with the registration statement, the issuer files a copy of the prospectus with the SEC.

The prospectus is intended to provide full and fair disclosure to the potential investor.

- It is a formal written offer to sell securities.

- It discloses facts investors need to make informed decisions.

With the sale of a variable product:

- A prospectus must be delivered at the time of solicitation, prior to accepting premium.

- Variable life insurance policies require a 10-day free-look provision from the date of policy delivery.

Lesson summary

The differences between variable and fixed products can be summarized through 5 key concepts:

-

Licenses needed/regulated

- Variable contracts are insurance products regulated by the NAIC, requiring an insurance license to sell. They are also securities regulated by the SEC, necessitating a Series 6 or Series 7 investment license in addition to the insurance license.

-

Assumption of investment risk:

- Fixed contracts have a guaranteed rate of return, where the insurance company assumes the investment risk. Variable contracts have no guaranteed rate of return on principal, relying on investments in securities that can fluctuate in value, exposing investors to potential losses.

-

Separate vs. general account:

- General accounts hold funds of fixed products, which are accessible to the insurance company’s creditors if it becomes insolvent. Separate accounts, mandated by the SEC, hold cash values of variable contracts and are not attachable by the insurance company’s creditors.

-

Variable contracts hedge against inflation:

- Variable contracts offer a hedge against inflation as their market value tends to increase with inflation, unlike fixed contracts that may result in a negative “real return” during periods of high inflation.

-

Prospectus required with sale of variable contract:

- Before offering securities, including variable contracts, a registration statement must be filed with the SEC along with a prospectus. The prospectus provides comprehensive information to potential investors, enabling informed decision-making. It must be delivered during solicitation before premium acceptance.