Dental Insurance

Dental insurance is generally sold on a group basis because of adverse selection. Insurers are often reluctant to write individual dental coverage because someone who needs dental work can postpone treatment until an insurance plan becomes effective. That can make the insurer liable for larger benefits than it would otherwise expect to pay.

Dental plans base benefits on UCR (usual, customary, and reasonable) charges. Charges above this limit are the insured’s responsibility and are subject to deductibles and co-insurance. Occasionally, dental insurance is part of a health benefits package with a single deductible called an integrated deductible, which applies to both medical and dental coverage. More often, dental coverage is provided through a separate policy with its own deductible.

In addition to deductibles and co-insurance, maximums may also affect the level of benefits payable under a dental plan. Generally, there is a specified maximum dollar amount payable per year, per procedure, and sometimes per family member covered. There may also be a lifetime maximum per individual.

Some dental policies are scheduled (basic) and only cover such things as:

- Routine visits to the dentist

- Protective fluoride treatments

- Diagnostic x-rays

- Dental exams and diagnosis

- Local anesthetics

- Teeth cleanings (usually once every 6 months)

- Preventive care

Most dental policies, however, are comprehensive and work much the same way as comprehensive medical expense coverage. Dental procedures covered by most comprehensive policies include:

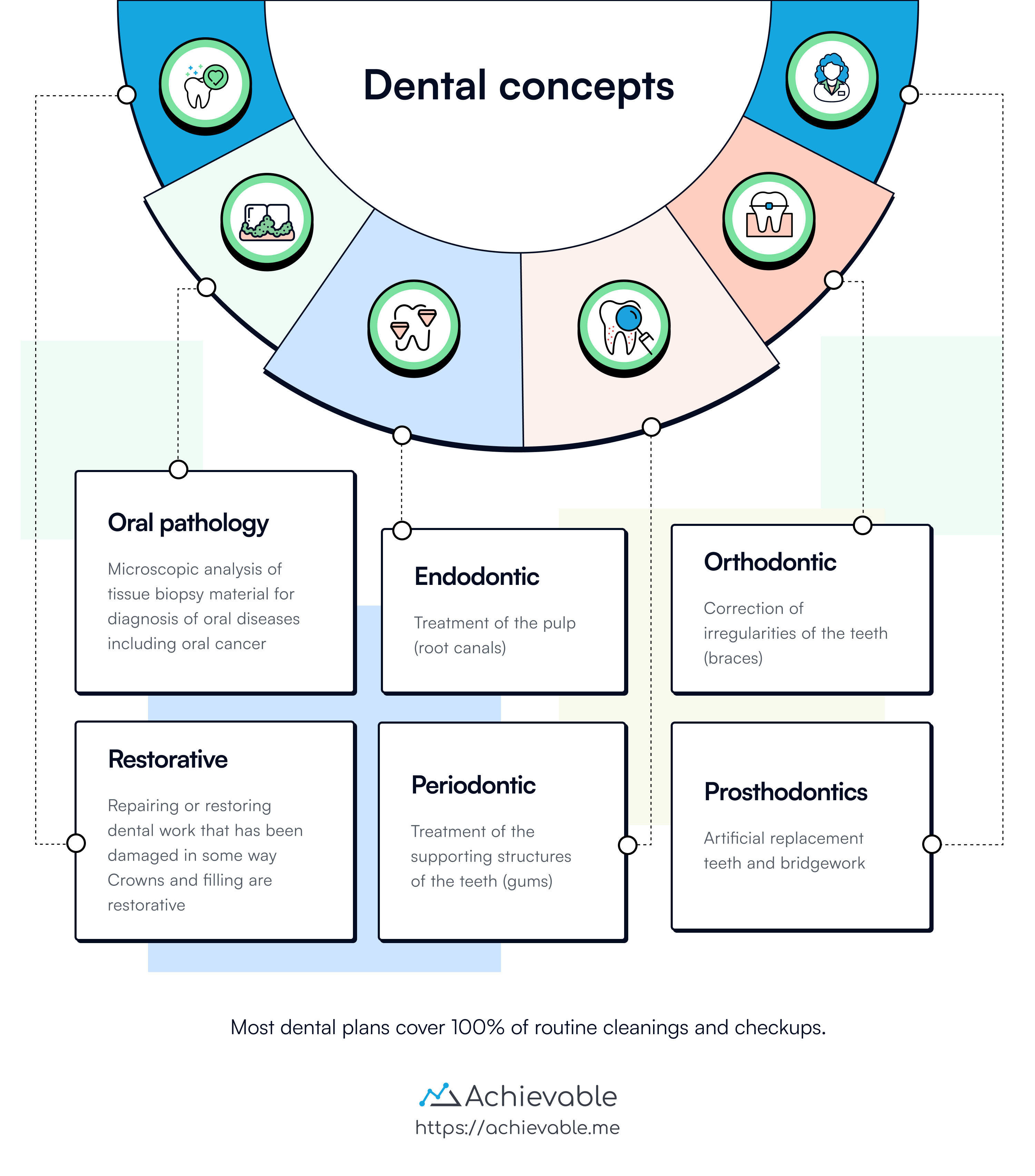

Restorative

- Repairing or restoring dental work that has been damaged in some way

Endodontics

- Treatment of the pulp (root canals)

Periodontics

- Treatment of the supporting structures of the teeth

Prosthodontics

- Artificial replacements and bridge work

Oral pathology

- Microscopic analysis of tissue biopsy for diagnosis of oral diseases including oral cancer

Orthodontics

- Correction of irregularities of the teeth (braces)

Prepaid dental plans

- In a prepaid dental plan, a corporation, partnership, or other entity provides or arranges for the provision of dental care services to enrollees or subscribers. Prepaid dental plans operate in much the same way as health maintenance organizations. They offer services based on capitation, or fixed per-member, per-month payments. Under this approach, the provider assumes the full risk for the cost of contracted services without regard to the type, value, or frequency of the services provided.

Lesson summary

Dental insurance is primarily sold on a group basis due to adverse selection. Insurers are hesitant to offer individual dental coverage because people can delay treatment until a policy becomes effective, which can lead to higher-than-expected claims.

Dental plans base benefits on UCR charges. Any amount above the UCR limit is the insured’s responsibility and is subject to deductibles and coinsurance. In addition:

- Dental insurance may be part of a health benefits package with an integrated deductible for medical and dental coverage, or it may be issued as a separate policy with its own deductible.

- Maximums may also apply, such as a specified dollar amount payable per year, per family member, or a lifetime maximum per individual.

Some dental policies are scheduled (basic) and cover routine visits, cleanings, and preventive care. Comprehensive policies cover a wider range of procedures, including endodontics, periodontics, prosthodontics, and orthodontics. Nearly all plans cover 100% of routine cleanings and checkups.

Prepaid dental plans operate similarly to health maintenance organizations and are structured as follows:

- In prepaid dental plans, a corporation or entity provides or arranges dental services.

- Services are based on capitation or fixed payments per member per month.

- The provider assumes the full financial risk for contracted services.