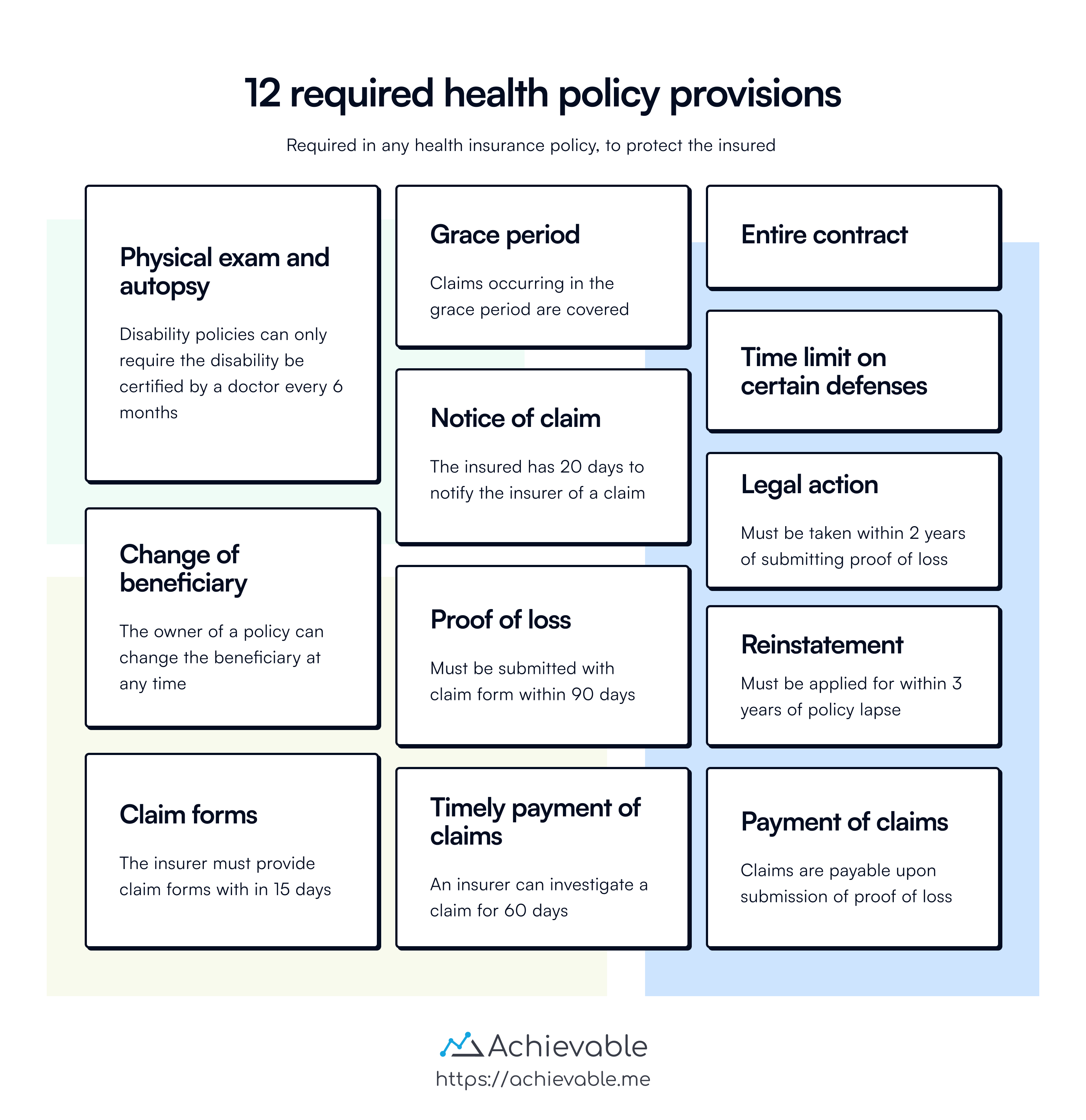

Required Policy Provisions

Just as with life insurance policies, health insurance policies include standard provisions that appear in most contracts. Over time, the National Association of Insurance Commissioners (NAIC) and state insurance departments have identified a set of uniform policy provisions.

There are 12 required uniform policy provisions and 11 optional uniform provisions. Insurers may vary the wording from the NAIC’s recommended language, but any changes must:

- Be at least as favorable to the insured and the beneficiary as the standard provision

- Be approved by the director of insurance

Uniform required policy provisions

Grace period

- Each policy must provide a grace period for late premium payments, during which the policy stays in force. The minimum grace period is 7 days for weekly premium policies, 10 days for monthly premium policies, and 31 days for all other premium payment modes. ACA grace periods are different and will be covered in a later chapter.

Change of beneficiary

- The policy owner has the right to change the beneficiary on accidental death policies at their discretion, unless an irrevocable beneficiary was named.

Entire contract

- All riders, attachments, waivers, notes, reports, and similar documents are part of the entire contract. As with life policies, the application also becomes part of the contract.

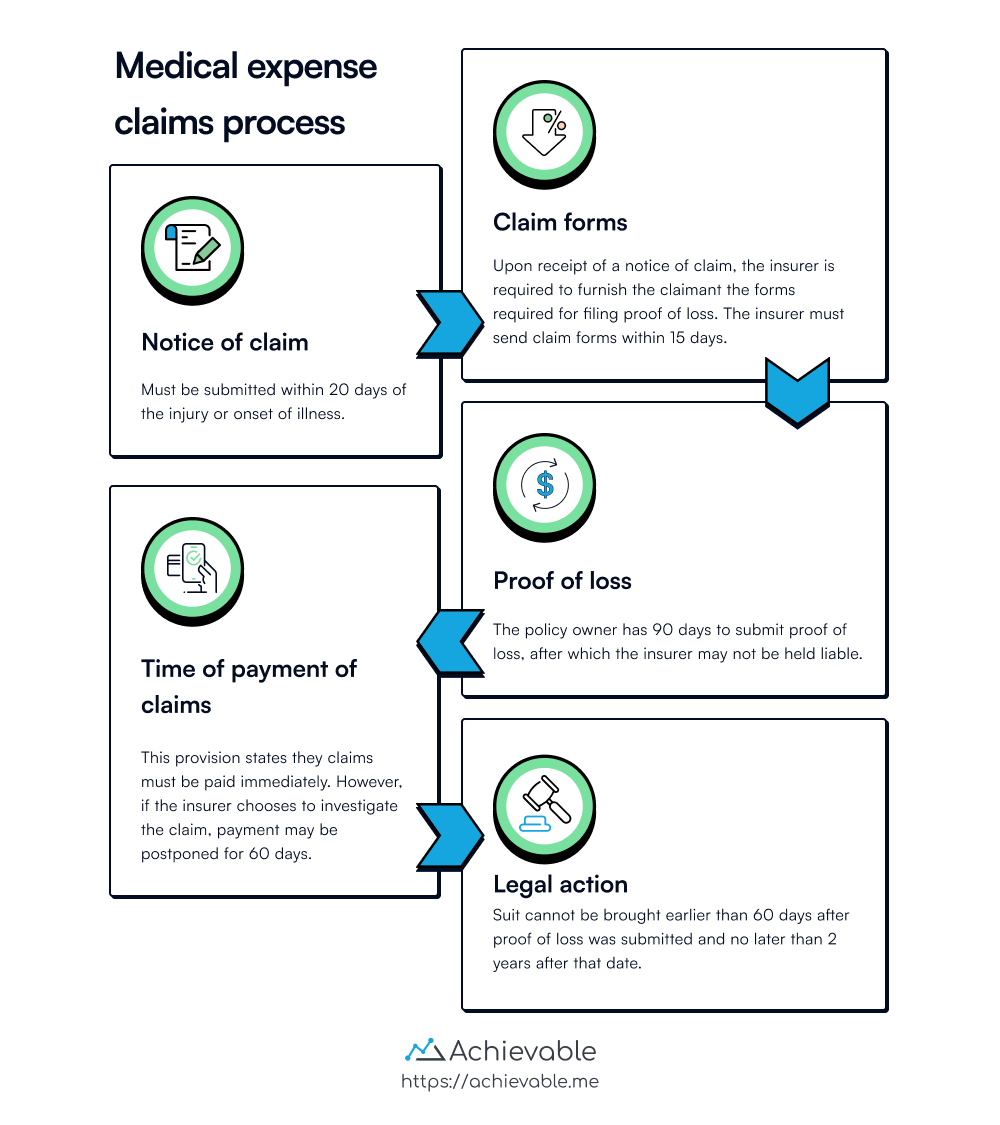

Notice of claim

- This provision explains how and when the policy owner must notify the insurer after the onset of a covered illness or injury. Written notice of claim must be sent within 20 days.

Claim forms

- After receiving a notice of claim, the insurer must provide the claimant with the forms needed to file proof of loss. The insurer must send claim forms within 15 days. If the insurer does not provide claim forms within 15 days, the claimant may submit written proof of loss in any reasonable form.

Proof of loss

- The insurer may require the policy owner to document the loss, such as through doctor and/or hospital statements. The policy owner has 90 days to submit proof of loss; after that, the insurer may not be held liable.

Time of payment of claims

- This provision states that claims must be paid immediately. However, if the insurer chooses to investigate the claim, it may postpone payment for 60 days. Disability income payments must be made at least monthly.

Payment of claims

- This provision describes how claims are paid. Death claims are paid to the beneficiary. All other indemnification is paid to the insured.

Legal action

- This provision limits when the insured may sue to collect under the policy. A suit cannot be brought earlier than 60 days after proof of loss was submitted and no later than 2 years after proof of loss was submitted.

Time limit on certain defenses

- This required uniform provision prohibits the insurer from contesting the validity of the policy, or from denying a claim for disability commencing after 2 years from the date of issuance, on the grounds that the applicant made misstatements in the application. This is the accident and health equivalent of life insurance’s “Incontestable Clause.” Unlike life insurance, a health insurance policy is always contestable for fraud.

Physical examination and autopsy

- The insurer has the right to request a physical exam or autopsy before paying a claim. Physical examinations are generally requested only for disability income claims, and an autopsy applies only to AD&D. The insurer is required to pay for the exam or autopsy.

Reinstatement

- This provision explains how a policy may be reinstated after it has lapsed. After reinstatement, accident coverage is effective immediately, while illness coverage begins after a 10-day waiting period. The insurer may require a new application (and proof of insurability). However, if the insurer does not request this within 45 days of the policy owner paying the reinstatement premium, the policy is automatically reinstated. Reinstatement must be applied for within 3 years.

Lesson summary

Health insurance policies, like life insurance policies, include standard provisions set by the National Association of Insurance Commissioners and state insurance departments. These provisions are designed to protect both the insured and the insurer:

- Grace period: Provides a period for late premium payments before the policy lapses (e.g., 7 days for weekly premiums).

- Change of beneficiary: Allows the policy owner to change beneficiaries unless irrevocable.

- Entire contract: Includes all attachments and the application as part of the contract.

- Notice of claim: Specifies when and how the insurer must be informed of a covered illness or injury.

- Claim forms: Must be provided to the claimant within 15 days of a claim notice.

- Proof of loss: Policy owner has 90 days to provide evidence of loss; insurer may require doctor or hospital statements.

- Time of payment of claims: Claims should be paid immediately, or within 60 days if under investigation.

- Payment of claims: Explains how death claims and other indemnification claims are paid.

- Legal action: Sets time limits for bringing lawsuits under the policy.

- Time limit on certain defenses: Prohibits contesting the policy after 2 years from issuance (except for fraud).

- Physical examination and autopsy: Insurer may request this before paying a claim.

- Reinstatement: Outlines procedures for reinstating a lapsed policy.