Term Life Insurance

While life insurance products can seem endless, they’re built from just two basic forms. Over time, insurers have created many variations of these two forms, so today you can usually find a policy to fit almost any life insurance need.

Life insurance is provided through either a term policy or a permanent (whole life) policy. No matter how complex a policy name sounds, it’s term, whole life, or a combination of the two.

Term insurance

- Term insurance provides pure life insurance protection and is designed to be used for a limited period of time (a term). It’s used to meet temporary insurance needs. Because it’s less expensive than permanent insurance, it may be the best option in many situations. There is no cash accumulation in a term policy. When a term policy expires, the policy owner should expect no financial return from it.

Permanent (whole life)

- Whole life insurance provides insurance protection for the insured’s whole life or until age 100 (or 121 in many modern policies), when the policy matures. Over time, a cash value accumulates, which is an important feature of a permanent life insurance policy.

Term life policies

Because term policies have no savings element, premiums in the younger years of a policy owner’s life are low compared to a whole life policy. However, term insurance premium rates rise each time the policy is renewed. At advanced ages, term insurance rates can be much higher than the rates for a whole life policy, assuming both policies were purchased at a younger age.

Term insurance rates mainly reflect the mortality charge. Because mortality increases with age, term premiums generally increase with age as well.

Term insurance is appropriate when a person has a short-term or temporary need for life insurance. It’s also appropriate when the insured:

- has a decreasing need for life insurance

- has a need for life insurance but has budgetary constraints

- wants to protect future insurability (through the use of the convertibility rider)

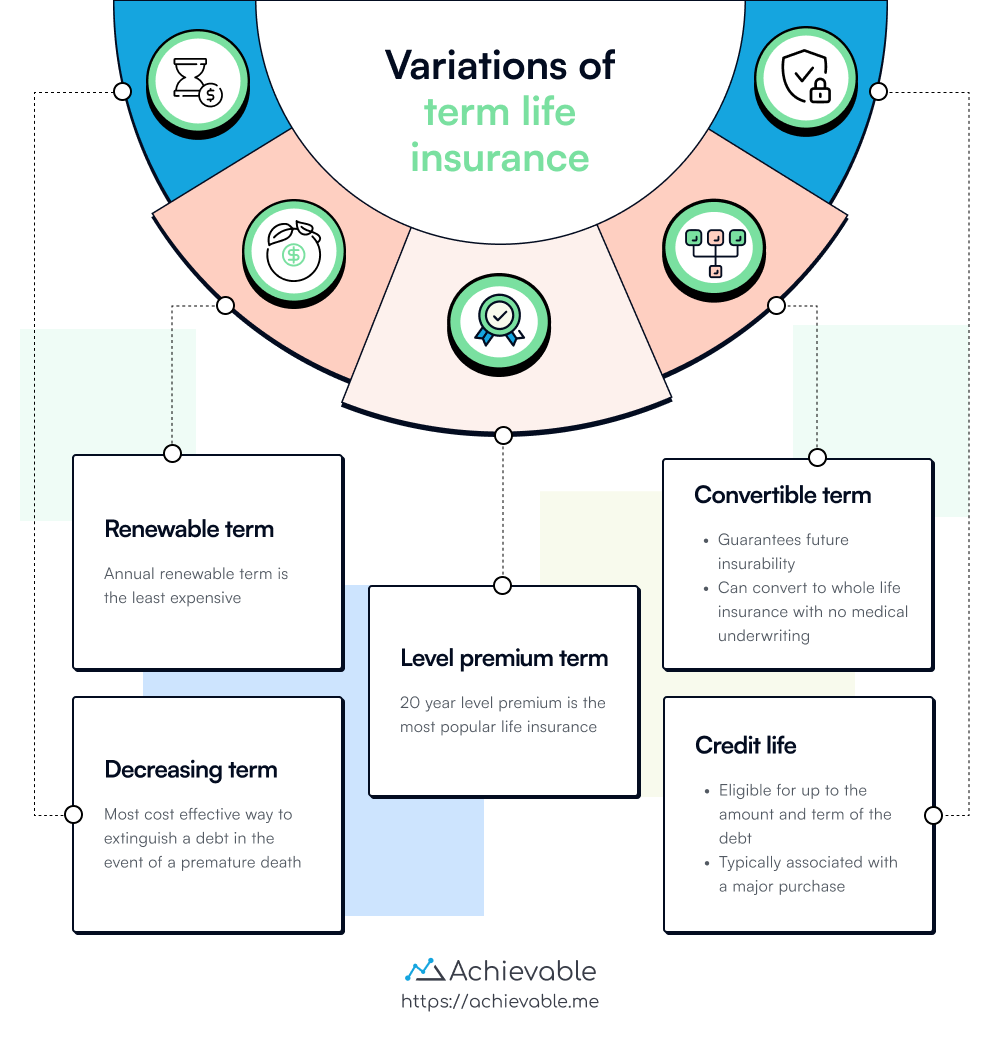

Renewable term

All term policies are issued with a stated termination date. That date may be specified as a number of years or to a stated age. Term policies may be issued for a period as short as one year (annual renewable term).

Term policies with a renewability feature allow the policy owner to renew the policy at the end of the term without providing evidence of insurability. Because the insurer is taking on the risk that the insured’s health may have changed, a renewable term policy is more expensive than a non-renewable policy.

This renewability feature is especially valuable in 20- or 30-year policies. There is always the risk that the policy owner’s health will deteriorate, making them uninsurable. When a policy is renewed, the new premium rate is based on the insured’s attained age.

Level premium term

Level premium term insurance maintains a level face amount and level premiums during the policy’s lifetime. Level term insurance is appropriate when the amount of required insurance stays the same, but only for a limited period of time.

For example, it’s ideal for a parent who wants extra financial protection while their children live at home, but won’t need that extra protection once the children mature and leave home.

Convertible term

Convertibility is a feature that may be added to a term policy. It gives the policy owner the right to convert the term policy to a whole life policy without providing evidence of insurability.

Decreasing term insurance

With this type of policy, the premium remains level, but the death benefit decreases each year. The most common use of decreasing term insurance is with mortgages and loans. As the loan balance decreases, the need for protection decreases as well.

Credit life insurance

Using decreasing term insurance to cover a debt is the basic principle behind credit life insurance. Written on the life of the debtor, the coverage may be individual or group, but it is usually written on a group basis.

Proceeds are payable to the creditor to extinguish a debt. This type is often sold by car dealers, banks, and other creditors. The maximum policy period cannot exceed the life of the loan, and the policy benefit cannot exceed the amount owed. If the loan is paid off early, excess premiums are refunded to the policy owner.

Lesson summary

Life insurance products generally fall into two basic forms: term insurance and permanent (whole life) insurance. These forms have evolved over the years to meet various needs, resulting in a wide array of products. Here’s a breakdown:

- Term insurance:

- Provides pure life insurance protection for a limited period.

- Best for temporary insurance needs due to its lower cost compared to permanent insurance.

- No cash accumulation; expires without financial return.

- Premiums are lower in younger years but increase with each renewal.

- Permanent (whole life) insurance:

- Provides coverage for the insured’s entire life or until age 100 (or 121 many in modern policies).

- Includes a cash value accumulation feature.

Further details on term insurance:

- Renewable term:

- Policy can be renewed without proof of insurability, but at a higher cost.

- Level premium term:

- Maintains constant face amount and premiums during the policy’s lifetime.

- Suited for situations where insurance needs are temporary and static.

- Convertible term:

- Option to convert term policy to whole life without evidence of insurability.

- Decreasing term insurance:

- Premium remains level but death benefit decreases annually, commonly used for mortgages.

- Credit life insurance:

- Decreasing term insurance used to cover debts, often sold by creditors with proceeds payable towards debt.

- Policy period matches the loan term and benefits are capped at the owed amount.

- Excess premiums are refunded if the loan is paid off before the policy term.