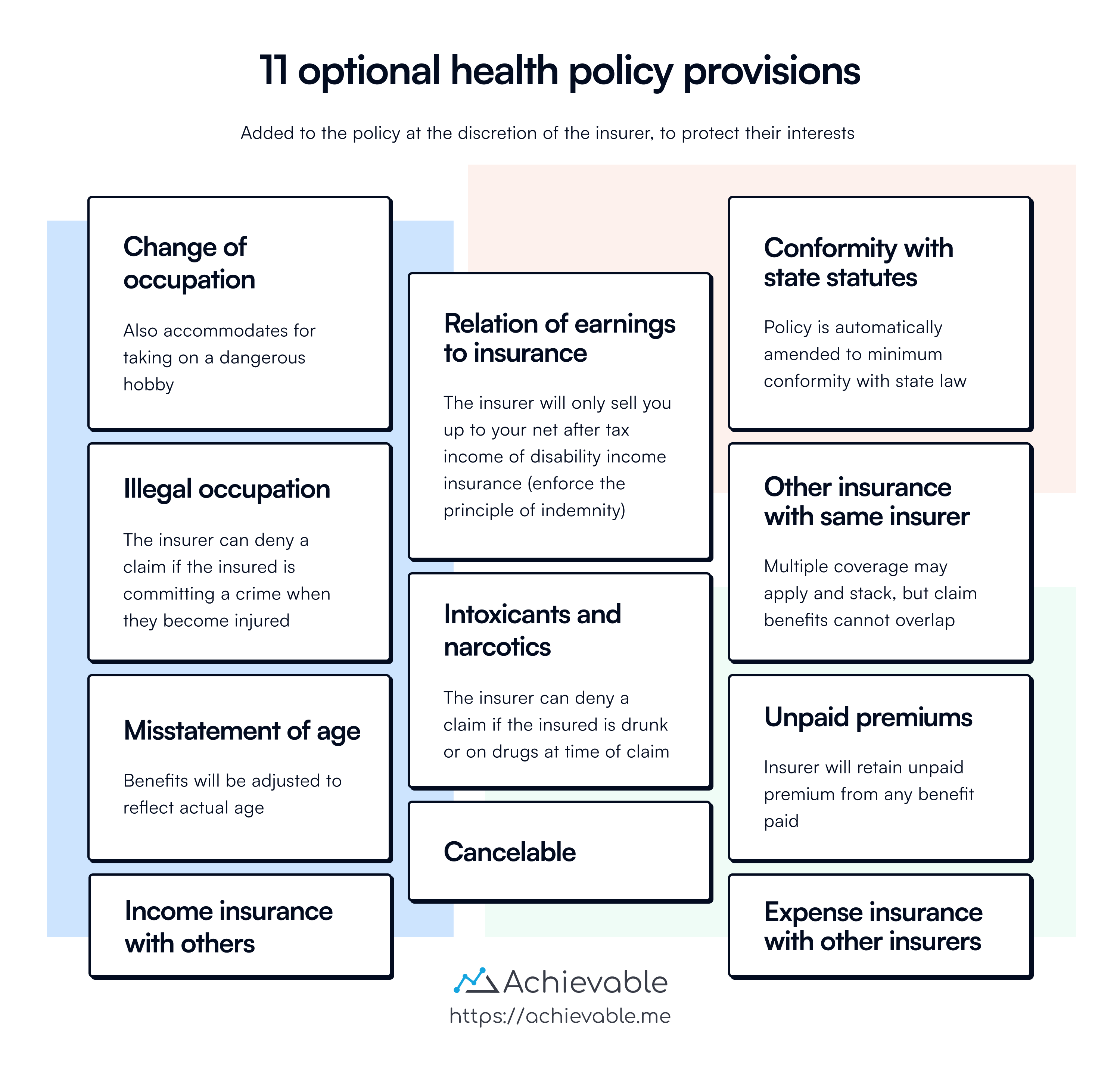

Optional Policy Provisions

Optional provisions are policy provisions the insurer may choose to include or leave out. The 11 optional policy provisions are as follows:

Change of occupation

- If the insured changes to a more hazardous job, benefits may be reduced. If the insured changes to a less hazardous job, premiums may be reduced.

Misstatement of age

- Benefits will be adjusted to reflect what the premiums would have purchased if the insured’s correct age had been stated on the application.

Other insurance with the same insurer

- If the policyowner has two or more policies with the same insurer, the insurer will coordinate benefits so that no more than 100% of the loss is paid. Premiums for coverage in excess of benefits paid will be refunded.

Expense insurance with other insurers

- Applies when the insured has expense-type policies (such as hospital or surgical coverage) with more than one company. The insurers will coordinate benefits so that total reimbursement does not exceed 100% of the actual medical expenses.

Income insurance with other insurers

- Applies when the insured has disability income coverage with more than one company. The insurers will coordinate benefits so the total disability benefits do not exceed the insured’s actual earned income.

Relation of earnings to insurance

- Ensures disability income benefits do not exceed the insured’s actual earned income, reinforcing the principle of indemnity.

Unpaid premiums

- Allows the insurer to deduct any premium due but unpaid from the amount of a claim. This often applies if a claim occurs during the grace period.

Cancellation

- Allows the insurer to cancel the policy with proper notice and requires any unearned premium to be refunded to the policyowner.

Conformity with state statutes

- Any policy provision that conflicts with state law is automatically amended to conform with the statutes of the state where the insured resides.

Illegal occupation

- No coverage is provided if a claim arises from the insured committing a felony or engaging in an illegal occupation.

Intoxicants and narcotics

- No coverage is provided if a claim occurs while the insured is intoxicated or under the influence of non-prescribed drugs.

Other general provisions

Free look (right to examine)

- Under this provision, the insured may return the policy to the agent or the insurer within 10 days of delivery (30 days for LTC and Medigap policies) and receive a full refund of premiums paid.

Insuring clause

- This provision is customarily found on the first page of the policy. It defines the benefits and policy periods and states the insurer’s promise to pay benefits if coverage is provided by the policy and all conditions are satisfied.

Consideration clause

- This provision states the amount and frequency of premium payments and the representations made by the applicant. It also describes the insurer’s obligation to pay the benefits.

Assignment of benefits provision

- This provision defines the benefit amounts to be paid in the event of a covered loss. In many cases, the beneficiary of a health reimbursement policy prefers that the insurer pay the doctor or hospital directly. If either will accept assignment of benefits, the insurer will pay them directly in the name of the insured.

Waiver of premium

- Disability income policies usually include this option, which exempts the insured from paying premiums if totally and permanently disabled. Other types of policies may also make this option available, for an additional premium.

Lesson summary

In an insurance policy, optional provisions can be included or excluded at the discretion of the insurer.

Optional policy provisions:

- Change of occupation: Benefits or premiums may be adjusted if the insured changes to a job with a different risk level.

- Misstatement of age: Benefits are adjusted to what the correct age and premium would have purchased.

- Other insurance with the same insurer: Prevents double recovery if the insured has more than one policy with the same company.

- Expense insurance with other insurers: Coordinates medical expense coverage between insurers so payments don’t exceed actual bills.

- Income insurance with other insurers: Coordinates disability income coverage between insurers so total benefits don’t exceed earnings.

- Relation of earnings to insurance: Disability benefits cannot exceed the insured’s actual earned income.

- Unpaid premiums: Any unpaid premium may be deducted from a claim payment.

- Cancellation: Insurer may cancel with proper notice and must refund any unearned premium.

- Conformity with state statutes: Policy automatically amends to meet state insurance laws.

- Illegal occupation: No coverage if the insured is injured while committing a felony or engaging in illegal work.

- Intoxicants and narcotics: No coverage if the insured is injured while intoxicated or using non-prescribed drugs.