Retirement Plan Distribution Rules

Distribution/Withdrawal rules

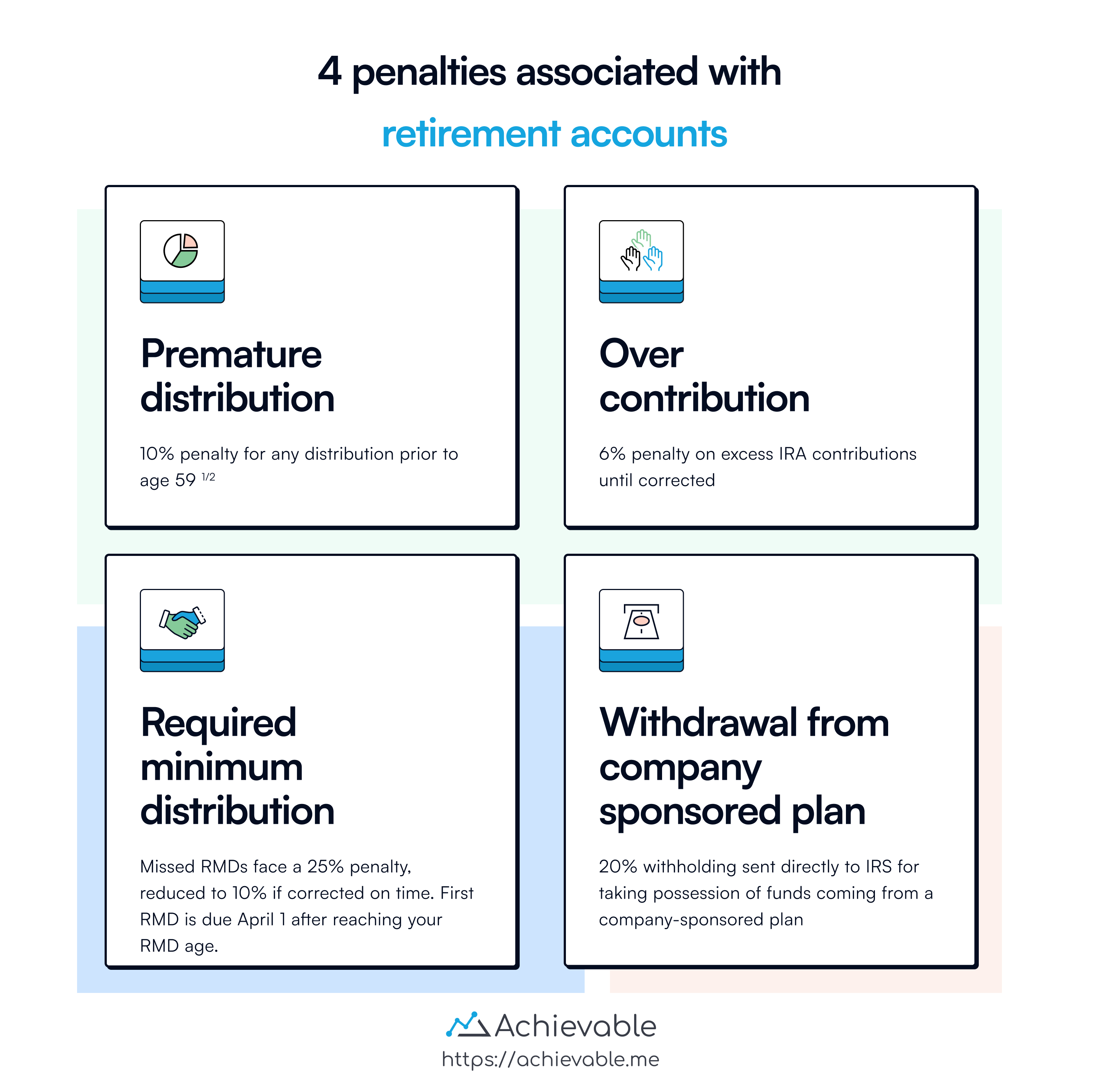

Distributions taken from a qualified retirement plan are taxed as ordinary income. If you take a distribution before age 59½, it’s generally also subject to a 10% early distribution penalty.

You can’t avoid income taxation on a taxable distribution, but the 10% penalty won’t apply if the distribution is due to:

- Death

- Disability

- QDRO distribution (employer plans only)

- Emergency personal expense (up to $1,000/yr) or Domestic abuse distribution, if the plan allows

- Separation from service in or after the year the employee turns 55 (age 50 for public safety workers)

- Qualified Higher Education Expenses (IRA only)

- Medical Insurance Premiums for Unemployed Individuals (IRA only)

- Medical Expenses Exceeding 7.5% of AGI

- First-Time Homebuyer Expenses (up to $10,000, IRA only)

- Substantially Equal Periodic Payments (no age minimum; must continue 5 years or until age 59½, whichever is longer)

- Rollover to another Qualified Plan

- Birth or adoption of a child (qualified birth or adoption distribution)

Under the SECURE Act, a qualified birth or adoption distribution (QBAD) lets an individual withdraw up to $5,000 per qualifying birth or adoption without paying the 10% penalty, though the distribution is still subject to ordinary income tax.

If the distribution is due to the death of the account owner and the beneficiary is the spouse, the spouse may roll the qualified plan assets into:

- the spouse’s own IRA, or

- an employer plan that accepts roll-ins

This can further defer taxes until the beneficiary retires.

The IRS requires distributions from a qualified plan to begin no later than April 1st of the year following the year the account owner turns 73 (for individuals who reach age 72 after 2022). The penalty for failing to take the required minimum distribution (RMD) is 25%, which can be reduced to 10% if corrected in a timely manner.

Rollover and transfer rules

Assets in a qualified retirement plan can be moved to another qualified plan, but there are restrictions. Some payments (such as RMDs or hardship withdrawals) can’t be rolled over.

If the account owner takes possession of the funds, the rollover must be completed within 60 calendar days. This is commonly called a 60-day rollover.

An individual is only allowed one IRA-to-IRA 60-day rollover per 12 months. This limit does not apply to employer-plan rollovers or direct transfers. Further, if the funds are being “rolled” from a company-sponsored retirement plan, the corporation is required to withhold 20% of the distribution to be sent directly to the IRS.

To avoid the 20% withholding, the account owner may consider a direct transfer. In a direct transfer (trustee to trustee transfer), the funds move from one qualified plan directly to another, either electronically or by way of a check made out to the custodian of the receiving plan.

There are no time restrictions or maximum number of direct transfers that can take place in a year. Employer-plan direct rollovers are reported on Form 1099-R (Code G). IRA trustee-to-trustee transfers are generally not reported.

Nonqualified retirement plans

403(b) TSA and 457 Plans:

- A 403(b) is a defined contribution plan that may be established by a public school, state university, or nonprofit service organization. 457 plans are available to state and local government employees. Governmental 457(b) plans are not subject to ERISA, and distributions are not subject to the 10% penalty. Non-governmental 457(b) plans are subject to ERISA “top-hat” rules. Some nonprofit 403(b) plans are ERISA-covered unless they qualify for the Department of Labor’s limited involvement safe harbor. While similar in tax treatment to 401(k)s, these plans are not technically corporate qualified plans.

Deferred Compensation Plan:

- A deferred compensation plan is a nonqualified retirement plan where an employee or business owner defers current compensation in exchange for a larger payout at retirement. Because the plan is nonqualified, it can discriminate, and commonly does. Deferred compensation plans are typically established by business owners for themselves and are not made available to the employees of the business. (Discriminatory–Nonqualified)

Individual Retirement Plans:

-

While not technically qualified plans, many of the same rules apply here. IRAs provide an opportunity to save for retirement on a tax-deferred basis and may provide an immediate tax benefit through deductible contributions.

-

A Traditional IRA may be funded by anybody with earned income. If the individual making the contribution is not covered by a qualified retirement plan, the contribution to a traditional IRA is tax deductible. If the individual making the contribution is covered by a qualified plan, but has income below certain levels, the contribution is deductible in the year it is made. If income is above those limits, the contribution is still allowed but becomes nondeductible.

-

A spousal IRA may be funded for the benefit of the nonworking spouse who has no earned income.

- Traditional and spousal IRA contributions must be made by April 15 of the year after the tax year they apply to. Withdrawals are taxed as ordinary income, and a 10% penalty applies to most distributions taken before age 59½. Required minimum distributions now begin by April 1 of the year after the account owner turns 73. Rollover and transfer rules generally follow the same structure as those used for qualified retirement plans. The one-per-12-month rollover limit applies only to IRA-to-IRA 60-day rollovers, not to direct transfers or employer-plan rollovers.

-

Roth IRAs Roth IRAs are available to individuals under certain income limits. Contributions are made with after-tax dollars and are never deductible. Qualified distributions are tax-free if the account has been open for at least five years and the owner is age 59½ or older. Contribution amounts can be withdrawn at any time without tax or penalty. Anyone can convert a traditional IRA to a Roth IRA - there are no income limits for conversions. Taxes are owed in the year of conversion, but many choose this strategy for the long-term benefit of tax-free growth. Recharacterization of contributions is still allowed, but since 2018, Roth conversions can no longer be recharacterized.

Lesson summary

Distribution/Withdrawal Rules:

- Penalties apply if distributions occur before a specific age and not for qualified reasons

- Rollovers are an option for transferring assets between qualified plans

Nonqualified Retirement Plans:

- 403(b) and 457 Plans, Deferred Compensation Plans

Individual Retirement Plans:

- IRAs provide tax benefits for retirement savings

- Traditional, spousal, and Roth IRAs have different features and taxation rules