ERISA: Corporate Retirement Plan Standards

The Employee Retirement Income Security Act of 1974 (ERISA) established standards that corporate retirement plans must meet to receive favorable tax treatment. If a corporate retirement plan meets ERISA requirements, it’s a qualified plan, and the employer may deduct contributions to the plan as a business expense.

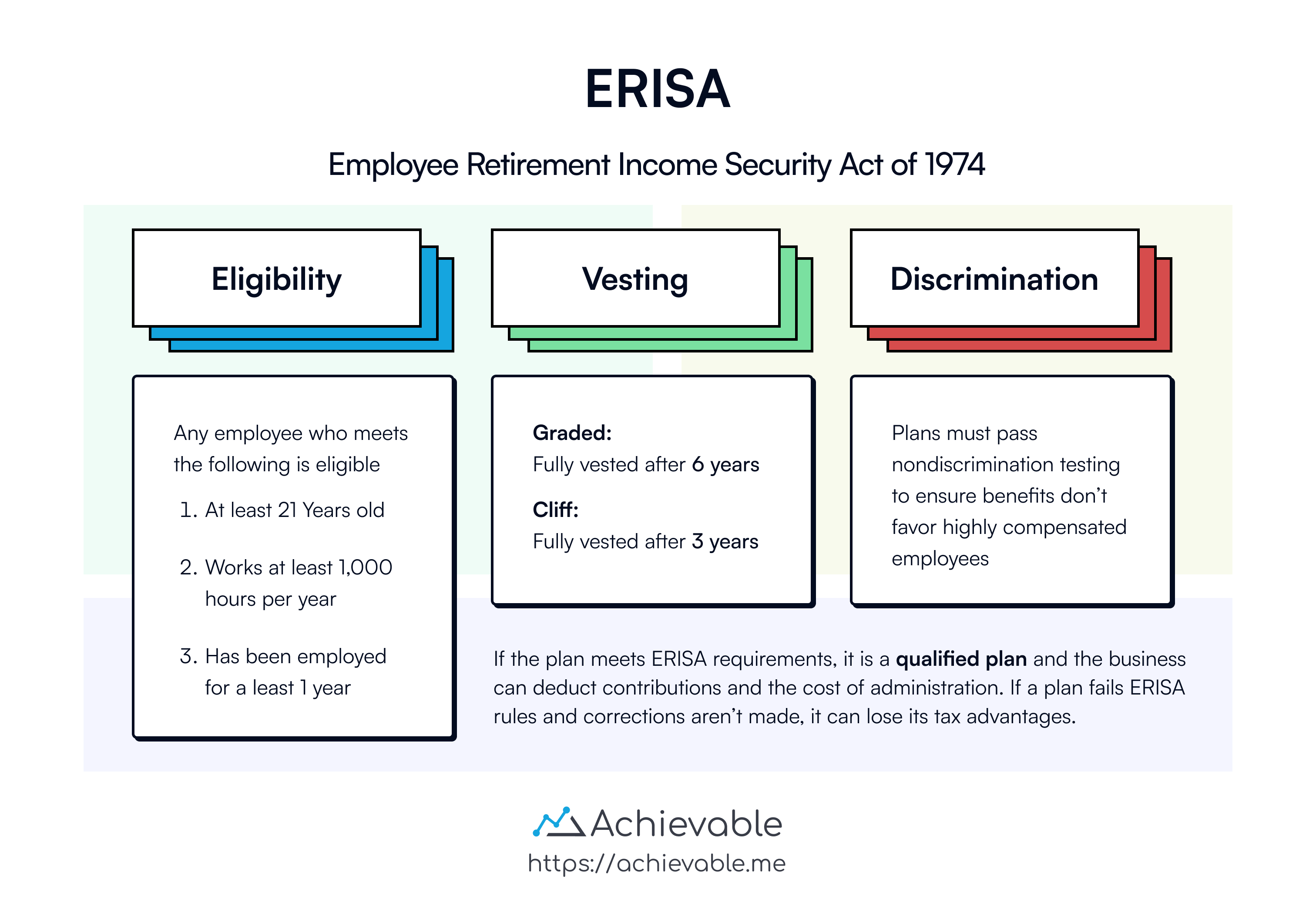

ERISA focuses on three core issues: vesting, eligibility, and discrimination.

Vesting provisions

Vesting is the amount of time that must pass before a plan participant has a non-forfeitable right to benefits under the plan.

- Employees are always 100% vested in their own contributions.

- ERISA limits how restrictive an employer can be with vesting schedules for employer (company) contributions.

Two common vesting schedules are:

- Graded vesting: A portion of the employer contribution vests each year, and the employee must be fully vested no later than the end of the sixth year.

- Cliff vesting: If the employer keeps vesting at 0% for the first two years, then the employee must become 100% vested at the end of year 3.

Eligibility

ERISA limits how long an employer can make employees wait before they’re allowed to participate in a corporate-sponsored retirement plan. At most, an employer can require an employee to be:

- At least 21 years of age, and

- Employed by the organization for one year (working at least 1,000 hours in that year)

These are maximum conditions, not requirements every plan must impose - an employer may allow participation on more lenient terms, such as immediate eligibility. Plans may also require up to 2 years of service as an alternative rule, but only if participants are 100% immediately vested.

A qualified plan also can’t discriminate in favor of highly compensated employees or owners - for example, it can’t be offered only to executives. Even so, a plan doesn’t have to cover every employee: an employer may exclude certain groups of employees (by job classification, location, and similar factors), as long as the plan still passes the IRS’s minimum coverage tests.

Discrimination

Employers may design different contribution formulas, but ERISA requires qualified plans to pass nondiscrimination testing so benefits don’t disproportionately favor highly compensated employees.

A plan is considered “top-heavy” if more than 60% of its assets benefit key employees. Top-heavy status does not automatically disqualify the plan. Instead, it generally requires the employer to:

- Provide special minimum contributions (generally 3% of compensation) for non-key employees

- Use accelerated vesting for non-key employees

Loans may be permitted, but they must be available on a nondiscriminatory basis.

ERISA also requires the plan document to be in writing. The plan must be funded, with plan assets segregated from other corporate assets. Participants must receive statements at least annually and have the right to name a beneficiary.

Defined benefit vs. defined contribution

Corporate retirement plans are generally structured as either defined benefit or defined contribution plans.

A defined benefit plan promises a specific benefit at retirement. The benefit is determined by a formula that typically uses factors such as:

- Age at retirement

- Compensation level

- Years of service

Defined benefit plans tend to favor older employees because larger contributions may be made for employees who are closer to retirement.

Defined contribution plans are more prevalent and generally easier to administer. The benefit a participant ultimately receives is not predetermined; it depends on the investment return earned by the funds in the plan.

With a defined contribution plan, the IRS limits allowable contributions. There is also a “catch-up” provision that allows people over age 50 to contribute more to a qualified plan. If a person exceeds the maximum allowable contribution, a 6% per year penalty is assessed on the excess contribution.

Types of qualified plans

401(k):

- A 401(k) is the most common type of qualified defined contribution plan. Employees may allocate a portion of their salaries to this plan, and contributions are excluded from their income for federal income tax purposes. Contributions reduce taxable income for federal income tax but remain subject to Social Security and Medicare (FICA) taxes. Contributions and earnings grow tax deferred until withdrawn. Withdrawals from a 401(k) plan are taxed as ordinary income and may be subject to an additional 10% federal tax penalty if withdrawn prior to age 59½.

Roth 401(k):

- Roth 401(k) plans must be funded with after-tax contributions. Withdrawals are tax-free if the participant is at least age 59½ and the account has been held for at least five years (the “5-year rule”).

Profit sharing/money purchase plans:

-

Profit sharing plans are popular with companies in cyclical industries because they do not require a fixed contribution. The company can increase, decrease, or even skip a contribution as long as the contributions are “substantial and recurring.”

-

With a money purchase plan, the employer contributes a fixed percentage of the employee’s salary regardless of the company’s profitability. The company must make contributions or pay a penalty.

SIMPLE (Savings Incentive Match Plan for Employees):

- A SIMPLE plan is established by the employer. Each eligible employee has a SIMPLE IRA, into which the employer deposits salary deferrals and required/matching contributions. SIMPLEs are only available to small employers (100 or fewer employees). A SIMPLE plan eliminates the administrative work and costs associated with other plans. A participant in a SIMPLE plan will “simply” open an IRA account at the brokerage firm of their choice; the employer will make appropriate salary deductions and deposit them, along with any match the company may make, into the employee’s IRA.

SEP (Simplified Employee Pension Plan):

- An SEP is established by the employer, usually through IRS Form 5305-SEP. Contributions are made by the employer to SEP-IRAs owned by the employees. With high contribution limits and immediate vesting, SEPs are generally appropriate for small, family-owned businesses looking to fund a retirement plan with company profits, lowering the tax liability of the company.

Keogh (HR-10):

- Keoghs are qualified retirement plans for self-employed individuals and owners of unincorporated businesses, such as lawyers or doctors. They may be structured as defined contribution or defined benefit plans. If the owner has employees, the plan is subject to ERISA eligibility and nondiscrimination rules.

Lesson summary

The Employee Retirement Income Security Act of 1974 (ERISA) established standards for corporate retirement plans to qualify for tax benefits:

- A qualified plan allows employers to deduct contributions as a business expense

- Core issues of ERISA include vesting, eligibility, and discrimination

Vesting provisions:

- Vesting determines when a participant gains a non-forfeitable right

- Employees are 100% vested in their contributions

- Options include graded vesting and cliff vesting

Eligibility:

- Age 21 and one year of service (1,000 hours) are the maximum conditions an employer may impose before allowing participation - a plan may set more lenient terms, and may exclude certain employee groups as long as it passes IRS minimum coverage tests

Discrimination:

- ERISA requires nondiscrimination testing to ensure benefits do not favor highly compensated employees.

- Top-heavy plans can lead to loss of qualified status

Defined benefit vs. defined contribution:

- Defined Benefit provides specific retirement benefits

- Defined Contribution depends on plan investments

Types of qualified plans:

- 401(k), Roth 401(k), Profit Sharing/Money Purchase Plans, SIMPLE, SEP

- Keogh plans are for self-employed individuals