Exclusions and Cost Containment

Exclusions

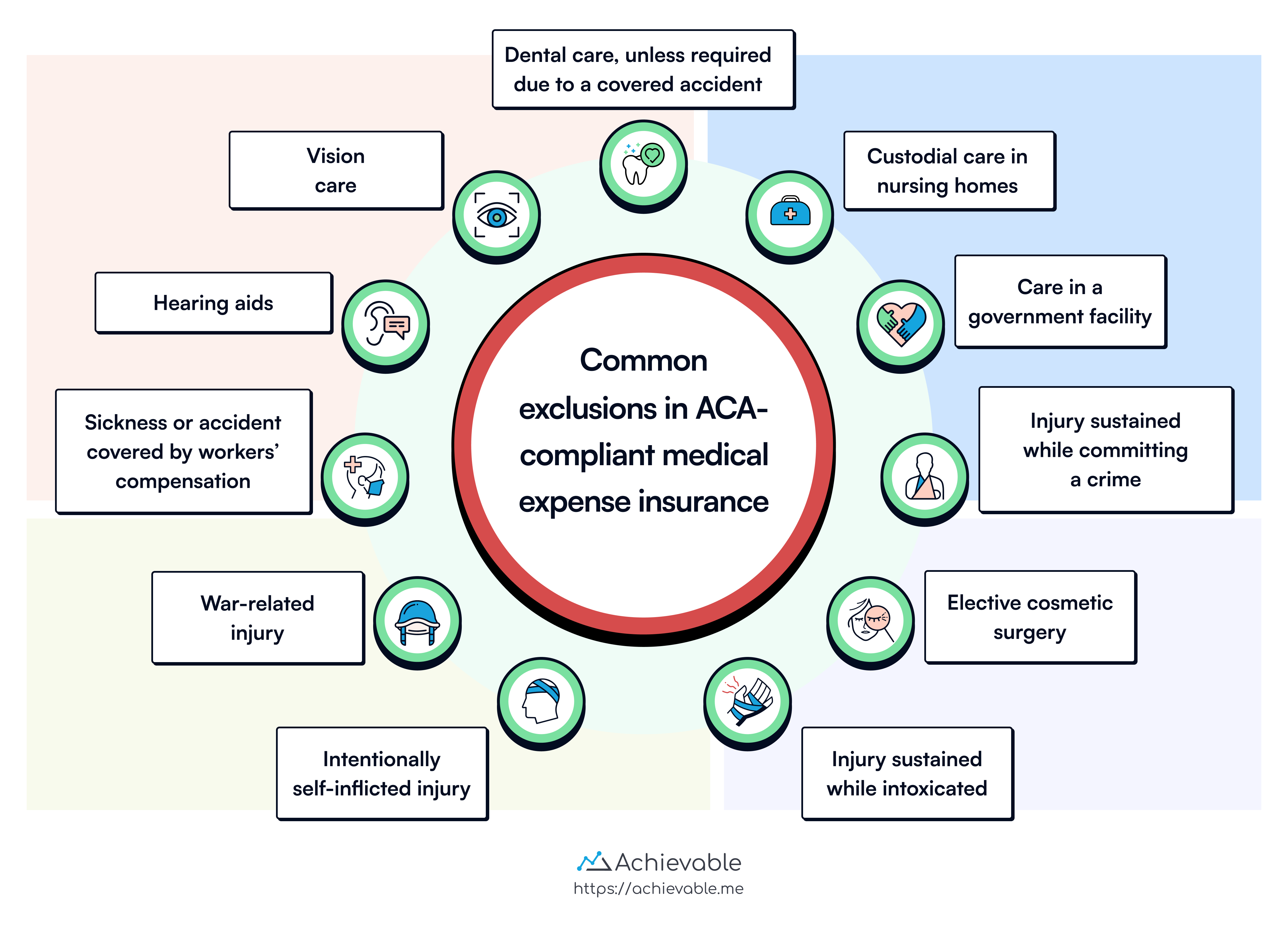

Exclusions that are common to most ACA-compliant medical expense insurance policies include:

- Custodial care in nursing homes

- Dental care, unless required due to a covered accident

- Vision care

- Sickness or accident covered by workers’ compensation

- Hearing aids

- War-related injury

- Intentionally self-inflicted injury

- Injury sustained while committing a crime

- Cosmetic surgery

- Elective cosmetic surgery is not an insurable expense. The only exception is in rare cases where it is required under a physician’s orders.

- Care in a government facility

- Government facilities are operated as an expense of the government, and treatment is provided at the government’s expense.

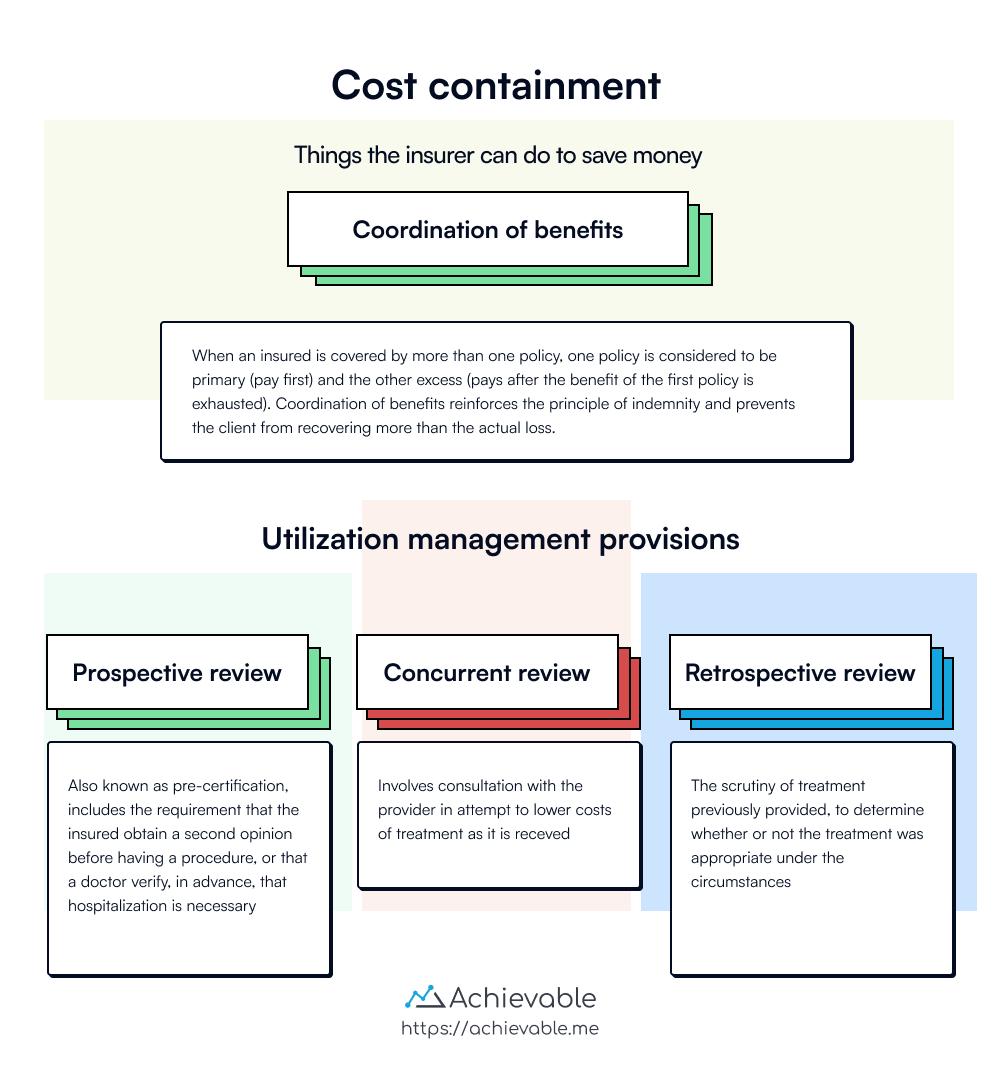

Cost containment

Most medical expense policies include a coordination of benefits provision. This provision applies when an insured is covered by more than one policy:

- One policy is primary (it pays first).

- The other policy is excess (it pays after the primary policy’s benefits are exhausted).

Coordination of benefits supports the principle of indemnity by preventing the insured from collecting more than the actual loss.

As health care costs rise, many policies include administrative controls designed to contain costs. These are commonly called utilization management provisions.

Utilization management uses specific criteria to review whether care is appropriate. Reviews may be performed on a prospective, concurrent, or retrospective basis.

Prospective review

- Also known as pre-certification. This may require the insured to obtain a second surgical opinion before elective surgery, or require a doctor to verify in advance that hospitalization is necessary and recommend outpatient treatment when appropriate.

Concurrent review

- This involves consultation with the provider while treatment is being received, with the goal of reducing costs. Some plans require the use of ambulatory services or require insureds to use outpatient services instead of hospitalization when possible.

Retrospective review

- This is a review of treatment that has already been provided to determine whether the treatment was appropriate under the circumstances.

Lesson summary

Exclusions common in medical expense insurance policies include:

- Custodial care in nursing homes

- Dental care, unless due to a covered accident

- Vision care

- War-related injuries

- Intentionally self-inflicted injuries

Cost containment measures include coordination of benefits and utilization management provisions, such as prospective, concurrent, and retrospective review, to help ensure care is appropriate.