Group Health Underwriting

Some of the rules in this chapter, such as pre-existing condition limitations and COBRA continuation, have been changed or modified by the Affordable Care Act (ACA). However, for exam purposes, these provisions are still tested in their original form. A separate chapter covers ACA-specific updates in detail. This chapter focuses on traditional group health underwriting topics that remain common on exams.

Group underwriting

Group health underwriting evaluates the risk of the group as a whole, not each individual. Underwriters typically don’t require physical exams or individual applications. Instead, they review group-level information such as:

- Size of the group

- Average age

- Type of work performed

- Claims history

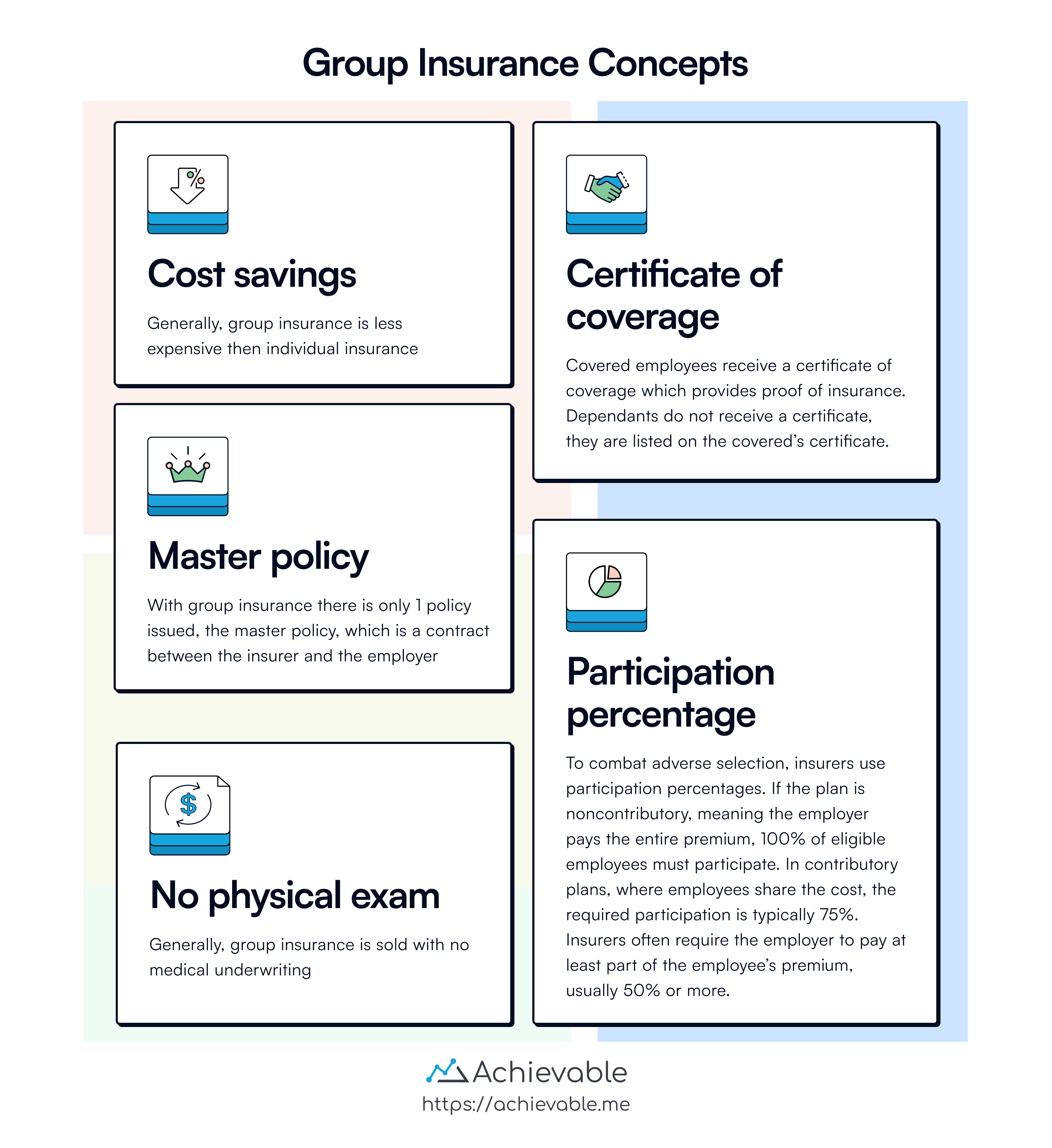

Because working populations are generally healthier than the overall population, group plans usually present lower morbidity risk. If the group qualifies, the insurer accepts or rejects the entire group (not individual members).

On each anniversary date, group underwriters review the previous year’s claims experience. This information is used, to some extent, to help determine the next year’s premium.

The variables used to calculate a group health premium are fundamentally the same as those used for an individual health policy. However, health premium calculations are generally more complex than life insurance premium calculations. Key variables include:

- Interest

- Expenses

- Morbidity

- Claims experience

- Policy benefits

Similar to mortality tables (which show how many people are expected to die at a given age), morbidity tables show how many people, out of a large group, are expected to become ill or disabled at a given age.

Insurers also impose requirements on group plans to reduce adverse selection and keep administrative costs low. One common requirement is participation percentage:

- Noncontributory plans (employer pays the full premium) typically require 100% of eligible employees to enroll.

- Contributory plans (employer and employees share the cost) typically require at least 75% participation.

Insurers often require the employer to pay part of the employee’s premium - commonly 50% or more - for the plan to qualify as contributory.

Employers are free to switch insurance carriers for their group coverage or terminate coverage altogether. Statutory rules regulate the terms and conditions that must be followed when this occurs.

The employees must be notified that the policy is being discontinued.

If a group health plan is discontinued, coverage must be extended for at least 31 days for any employee who is totally disabled at the time the plan ends. This gives the disabled employee time to secure new coverage without an immediate loss of benefits.

When one insurer replaces another:

- The prior insurer is liable for all claims incurred during any extension periods.

- The new insurer must cover all employees who were eligible to participate under the prior insurer.

- The new insurer must disregard any pre-existing conditions that would otherwise make a participant uninsurable.

Health insurance portability and accountability act (HIPAA)

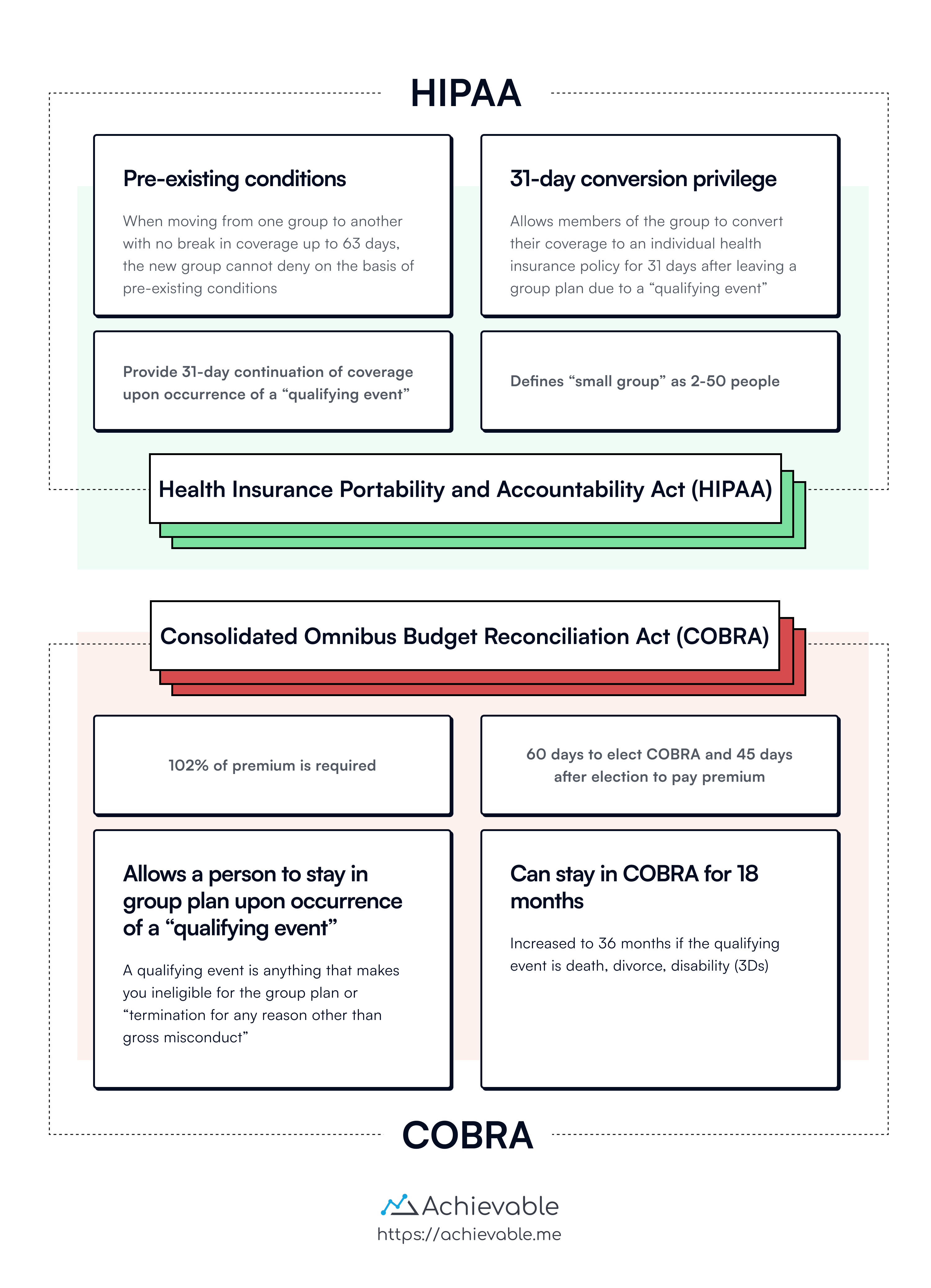

Under HIPAA, any insurer in the business of writing group health insurance must make the product available to small employer groups (2 to 50 employees) without regard to health status.

HIPAA limits how pre-existing conditions can be handled:

- The look-back period for pre-existing conditions is limited to 6 months.

- The maximum probationary period is 12 months (pre-existing conditions will be covered 12 months after enrollment).

- If an individual enters a group plan within 63 days of leaving another group plan, the new insurer cannot assign a probationary period for pre-existing conditions.

Pregnancy is not a pre-existing condition, and newborn children must be covered from the moment of birth. HIPAA guarantees coverage for:

- A 48-hour hospital stay after a vaginal delivery

- A 96-hour hospital stay after a caesarean birth

The newborn may be enrolled within 30 days without any pre-existing condition limitations.

Mandated by HIPAA, most group health policies include a conversion privilege. This allows members of the group to convert their coverage to an individual health insurance policy for 31 days after leaving a group plan due to a qualifying event.

The key value of this provision is that evidence of insurability is not required. This can be especially important for someone who has health problems or pre-existing conditions at the time of the qualifying event.

Qualifying events include:

- Termination for any reason other than gross misconduct

- Reduction in hours

- Cancellation of plan

- Disability

- Death or divorce (qualifying event for dependent spouse or child)

- Dependent child attaining age 19 (23 if attending school full time)

- Employer insolvency

Under HIPAA, employers must make full health care coverage available immediately (upon eligibility) to newly hired employees who were previously covered by a group policy for at least 12 months, with no break in coverage greater than 63 days. Coverage must be made available with no probationary, look back, or waiting periods.

Consolidated omnibus budget reconciliation act (COBRA)

COBRA is a federal law that requires, upon the occurrence of a qualifying event, employers with 20 or more employees to provide continuation of benefits under the employer’s group insurance plan for former employees and their dependents (at 102% of the required premium). COBRA provides transitional health care coverage until the employee and dependents can obtain coverage elsewhere.

Generally, the maximum period of coverage continuation is 18 months. However, if the qualifying event was death, divorce, disability, or a dependent child attaining age 19, the maximum period of coverage continuation is 36 months.

Upon the occurrence of a qualifying event, the employee or dependent has 60 days to notify the group insurer or plan administrator of their election to stay in the group plan through COBRA.

In effect, former employees may use the 60 days as a period of “free coverage,” by electing COBRA and paying the premium only if a claim arises. If the employee takes a new job (and enrolls in a new group plan), their new group coverage will most likely take effect before the transitional period allowed under COBRA expires. However, if COBRA is elected, the premium must be paid within 45 days.

HIPAA requires that every insurer who offers individual health insurance must offer at least two plans on a guaranteed issue basis to any individual who has elected and exhausted COBRA and is not eligible for coverage under any other group plan, Medicare, or Medicaid.

Other means of covering groups

Blanket disability insurance provides definite, ascertainable benefits to a changing, nameless group of people (the class). Anyone who enters the covered class is automatically covered. When they leave the class, coverage ends.

For example, a scout camp could purchase a blanket disability policy that pays a flat dollar amount (maybe $5,000) to anyone who sustains an injury requiring medical care while attending the camp.

Franchise insurance is similar to the concept of METs (Multiple Employer Trusts), but with franchise insurance, each eligible participant is issued an individual policy. Premium levels are reduced somewhat from those of regular individual policies because of savings in underwriting expenses and plan administration costs.

Another form of group coverage similar to the MET is the Multiple Employer Welfare Association (MEWA), which is an alternative to true group insurance. MEWAs provide self-funded health care benefits to employees of several large employers. In recent years, the growth of MEWAs has slowed due to increased requirements governing legal reserves.

Lesson summary

- Group underwriting does not assess individuals but considers group data like size and claims history.

- Group premiums are determined by factors such as morbidity, claims experience, and policy benefits.

- Requirements like participation percentages reduce adverse selection in group plans.

Under the Health Insurance Portability and Accountability Act (HIPAA), insurers must offer group health insurance to small employers without regard to health status. HIPAA also mandates coverage for pre-existing conditions, maternity care, and continuation privileges for members.

- Qualifying events like termination or death enable conversion to an individual policy without requiring evidence of insurability.

- The Consolidated Omnibus Budget Reconciliation Act (COBRA) demands that employers provide continuation of benefits after qualifying events.

Alternative group coverage includes blanket disability insurance and franchise insurance, catering to nameless groups with specific benefits. Multiple Employer Welfare Associations (MEWA) offer self-funded benefits to employees of large companies.