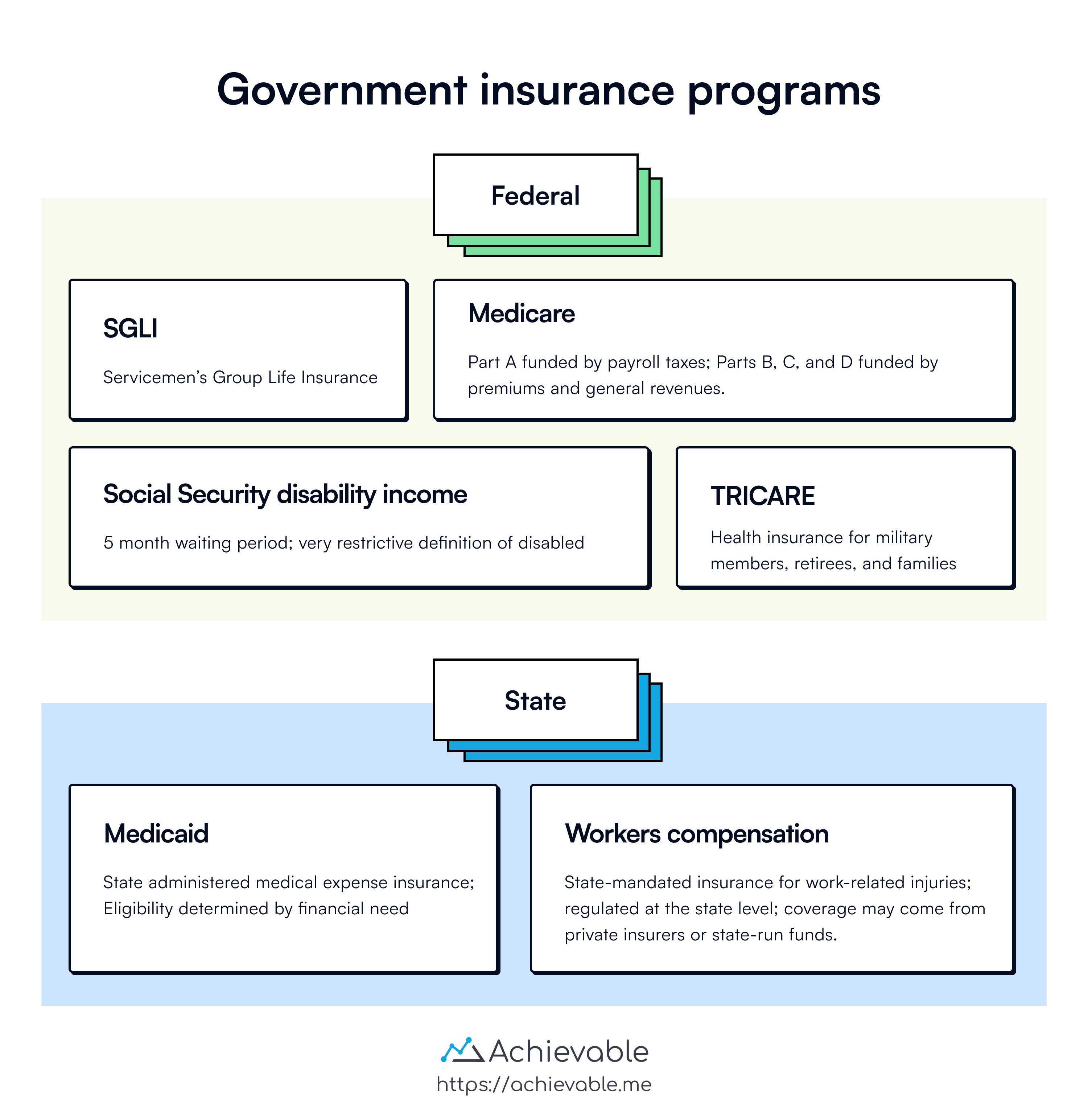

Medicare and Military Insurance

Medicare Part A is the “H” in OASDHI. Medicare is a four-part program: Part A, Part B, Part C, and Part D.

Medicare Part A

Individuals are eligible for Part A Medicare benefits as of the first day of the month in which they attain age 65, or if they are on dialysis or have been receiving Social Security disability benefits for at least 2 years.

When an individual is eligible for coverage under an employer’s plan as well as under Medicare, Medicare may be the secondary payer to any group health plan provided by an employer.

Part A provides coverage for inpatient hospital services, post-hospital skilled nursing care, and post-hospital home health services during recovery. Part A does not cover physicians’ services.

Enrollment in Part A is automatic for individuals entitled to Social Security benefits. These persons are eligible for Part A benefits on the first day of the month in which they attain age 65.

Part A provides coverage for four different kinds of care:

- Inpatient hospital care

- Skilled nursing

- Home health care

- Hospice care

Inpatient hospital care

Medicare’s inpatient hospital care benefit helps pay the reasonable charges that result from hospitalization in a semi-private room for medically necessary care. This coverage includes meals, regular nursing services, special care units, drugs taken in the hospital, tests, medical supplies, operating room costs, and other supplies and services.

Medicare Part A does not use an 80/20 coinsurance model. Instead, it uses a tiered cost-sharing structure for inpatient hospital care:

- Days 1-60: Fully covered by Medicare after the beneficiary pays the Part A deductible

- Days 61-90: Beneficiary pays a daily coinsurance amount

- Days 91-150: Beneficiary pays a higher daily coinsurance for lifetime reserve days

- After 150 days: No coverage is provided under Part A

Unlike Part B, Medicare Part A provides full coverage (not 80%) for the initial portion of a hospital stay.

Medicare covers up to 90 days of inpatient hospital services in each “benefit period,” plus an additional 60 “lifetime reserve” days. A benefit period begins when a beneficiary is admitted to the hospital and ends when the beneficiary has been out of the hospital for 60 days, or has not received Medicare-covered care in a skilled nursing facility for 60 consecutive days.

These 60 lifetime reserve days are a one-time bank that can be used across multiple hospital stays until they are fully exhausted. (Very few people remain in a hospital for 150 consecutive days. In the rare event this happens, every Medigap policy contains a benefit for an additional 365 hospital lifetime days.)

Skilled nursing care

Medicare defines the skilled nursing facility benefit quite narrowly. The patient must be receiving medically necessary services provided by a skilled staff in a Medicare-approved facility, following a prior hospital stay of at least 3 days. The care must be performed by or under the supervision of licensed nursing personnel under a doctor’s orders.

Any type of custodial (as opposed to skilled) nursing care is not covered. Medicare covers up to 100 days of care in a skilled nursing facility for each benefit period if all of Medicare’s requirements are met.

Home health care

Medicare covers up to 100 home health visits benefit period following a hospital stay under the Part A benefit. If a patient is confined at home, the home health care benefit covers certain services performed by a participating home health care agency. This may be a public or private agency that provides skilled nursing or therapeutic services in the home.

Eligible expenses include:

- Intermittent part-time nursing care

- Physical, occupational, or speech therapy

- Home health aides

- Medical social services

- Medical supplies

- Certain durable medical equipment, such as wheelchairs or hospital beds

Hospice care

A hospice is organized primarily to provide support services to terminally ill patients and their families. For terminally ill patients, the hospice care benefit provides inpatient and outpatient hospice care.

Respite care provides short-term relief for primary caregivers, giving them time to rest, travel, or spend time with others. Care may last a few hours to several weeks, and can take place at home, in a facility, or at an adult daycare center.

Medicare Part A may cover respite care in limited cases - only if the patient is receiving hospice care and meets certain conditions. Otherwise, respite care is typically not covered under Medicare and may be available through long-term care insurance or Medicaid.

What Part A does not cover

- Private duty nursing

- Charges for a private room, unless medically necessary

- Conveniences, such as a telephone or television in a hospital room

- The first 3 pints of blood received during a calendar year

Medicare Part B

Medicare Part B is available to anyone covered under Part A. Medicare Part B covers doctors’ services and outpatient medical services and supplies.

Part B is optional and requires subscribers to pay a monthly premium, deductibles, and a 20% co-pay on all charges for covered services. Part B pays (up to certain limits) for professional medical services and other services if prescribed by a physician.

While enrollment in Part B is voluntary, when individuals become eligible for Part A they will be enrolled and their premium payment established unless they sign a form indicating they do not want the Part B coverage.

People who choose not to enroll in Part B during their initial enrollment period may do so later. A general open enrollment period occurs each year from January 1st through March 31st.

When enrollment occurs during this period, coverage begins the first day of the month after enrollment (e.g., February 1st for January enrollments).

The most common reason to “opt out” of Part B coverage is that the individual is still working and covered by a group plan that offers better benefits than Part B.

Medicare determines a reasonable charge for a particular service. If the actual charge is more than that, the patient must pay the difference, unless the doctor or supplier agrees to accept an assignment.

Assignment means the doctor or supplier accepts Medicare’s approved amounts as full payment and cannot legally bill the patient for anything above that amount. Doctors and suppliers are not required to accept assignment, but most do.

If Medicare decides that an expense is not necessary, the patient must pay the entire cost.

Doctor’s services

Part B covers most physician’s services and supplies furnished as part of such services. Some of the specific covered services include:

- Medical and surgical services, including anesthesia

- Office visits, house calls, and hospital calls

- Radiological and pathological services provided by a physician

- Medical supplies furnished as part of a physician’s professional services

- Second opinions before surgery

- Diagnostic tests that are part of the patient’s treatment

- Services of the doctor’s office nurse

- Physical, occupational, and speech therapy services

- Blood transfusions

- Drugs that cannot be self-administered

Outpatient medical services and supplies

Medicare Part B will help pay for certain services received as an outpatient from a Medicare-certified hospital including:

- Outpatient clinic services

- Emergency room services

- X-rays, whether for therapy or diagnosis, billed by the hospital

- Medically necessary ambulance services

- Purchase or rental of durable medical equipment used in the patient’s home

- Artificial limbs and eyes

- Artificial replacements for internal organs (for example, colostomy bags and supplies)

- Braces for neck, back, or limbs

- Casts, splints, and surgical dressings

- Blood transfusions (after the first 3 pints)

- Physical, occupational, and speech therapy provided in a therapist’s office, or in the patient’s home

- Drugs that cannot be self-administered

- Mammograms, pap smears, and colon-rectal screenings

- Diabetes glucose monitoring and education

- Flu shots

What Part B does not cover

- Routine physical exams

- Eye exams, fitting of eyeglasses or contact lenses

- Hearing exams, fitting of hearing aids

- Most immunizations

- Routine foot care and treatment of flat feet

- Cosmetic surgery (unless needed due to an accidental injury)

- Skilled nursing home care costs over 100 days per benefit period

- Intermediate nursing home care

Excess charges from providers who do not accept Medicare assignment (up to 15% above the Medicare-approved amount)

- Most outpatient prescription drugs

- Care received outside the United States

- Custodial care received in the home

- Acupuncture

- Orthopedic shoes

- The first 3 pints of blood

Note on Respite Care Respite care provides short-term relief for primary caregivers, giving them time to rest, travel, or spend time with others. Care may last a few hours to several weeks, and can take place at home, in a facility, or at an adult daycare center. Medicare Part A may cover respite care in limited cases - only if the patient is receiving hospice care and meets certain conditions. Otherwise, respite care is typically not covered under Medicare and may be available through long-term care insurance or Medicaid.

Medicare Part C

Advantage plans

Many HMOs and PPOs have contracted with the federal government to offer Medicare advantage plans. These plans often provide broader benefits than Part A and Part B combined.

Medicare beneficiaries who have Part A and Part B can join one of many Part C plans and receive Medicare-covered benefits through the plan. In addition to the monthly Medicare Part B premiums, Medicare advantage plan subscribers pay an additional premium for the extra benefits the advantage plan offers.

The benefits of Part C include eliminating the need to purchase a Medicare supplement (Medigap) policy, since Medicare advantage plans generally cover the same benefits that a Medigap policy would.

Beneficiaries who do not enroll in a Medicare Advantage plan may choose to purchase a standardized Medicare Supplement policy, often called Medigap. (These policies are covered in the next chapter.)

Medicare Part D

Prescription drug insurance

Medicare Part D prescription drug plans are open to all people who are eligible for Medicare. Although participation is voluntary, no one may be denied coverage for health reasons. Part D plans are underwritten by private insurance companies.

Medicare Part D coverage phases

Medicare Part D plans divide prescription drug coverage into four phases. These cost-sharing stages determine how much the beneficiary pays at different levels of total spending:

-

Deductible Phase

The beneficiary pays 100% of the drug costs until the annual deductible is met.

(This amount varies by plan and changes yearly. For example, the standard deductible was $545 in 2024.) -

Initial Coverage Phase

After meeting the deductible, the plan covers a portion of the drug costs and the beneficiary pays a copayment or coinsurance. This phase continues until the total drug costs hit the annual threshold. -

Coverage Gap (Donut Hole)

After the threshold is reached, the beneficiary enters a temporary limit on coverage.

Beneficiaries pay a percentage of brand-name and generic drug costs (usually 25%). -

Catastrophic Coverage Phase

After total out-of-pocket costs reach the catastrophic threshold, the beneficiary pays $0 for covered Part D drugs, as mandated by the Inflation Reduction Act (effective 2024).

Additional Medicare concepts and definitions

To better understand how Medicare works in real-world situations - and to avoid penalties or gaps in coverage - it’s important to understand these related concepts:

Initial Enrollment Period (IEP)

The Initial Enrollment Period is a 7-month window:

-

Begins 3 months before the month a person turns 65

-

Includes the month of their 65th birthday

-

Ends 3 months after that month

Failing to enroll during this time can result in late penalties.

Special Enrollment Period (SEP)

A Special Enrollment Period allows a person to sign up for Medicare or switch plans outside the usual enrollment windows, if they experience qualifying life events such as:

-

Losing employer-sponsored coverage

-

Moving to a new service area

-

Becoming eligible for Medicaid or Extra Help

Late enrollment penalties

If you don’t sign up for Medicare on time, you may face permanent premium penalties:

-

Part B Penalty: 10% added to the monthly premium for each 12-month period you delayed enrollment (without qualifying coverage)

-

Part D Penalty: 1% of the national base premium multiplied by the number of uncovered months

Benefit period

A benefit period is how Medicare measures your use of inpatient hospital and skilled nursing services:

-

It begins the day you’re admitted to a hospital

-

It ends when you’ve been out of the hospital or skilled care for 60 consecutive days

-

A new benefit period can start again, resetting deductibles and limits

Example: If you’re hospitalized in January and again in April (after 60+ days out of the hospital), Medicare considers this a new benefit period.

TRICARE

TRICARE is regionally managed health care for domestic active duty military personnel and their families, retirees and their families, and survivors of all military service personnel who are not eligible for Medicare.

TRICARE offers eligible beneficiaries 3 choices for their health care:

- TRICARE Prime, with military treatment facilities being the principal source of health care.

- TRICARE Extra, which is a preferred provider option similar to PPO.

- TRICARE Standard, which is a fee-for-service option.

Active duty personnel and family members may enroll in TRICARE Prime. TRICARE Prime coverage for active duty members and their families is first dollar (meaning the plan pays before any out-of-pocket costs apply) coverage with no deductibles or co-payments.

Active and retired military personnel are also eligible for life insurance benefits through SGLI (Servicemen’s Group Life Insurance).

Lesson summary

Medicare is part of OASDHI with four parts: Part A, Part B, Part C, and Part D.

Medicare Part A covers:

- Inpatient hospital care

- Skilled nursing care

- Home health care

- Hospice care

Part B covers doctors’ services and outpatient medical services and supplies, with enrollment being optional. Medicare Part C Advantage Plans offer broader benefits, eliminating the need for a Medigap policy. Part D provides prescription drug coverage and includes four phases of cost-sharing: deductible, initial coverage, coverage gap, and catastrophic coverage.

TRICARE offer health care for active duty military personnel, retirees, survivors, and their families, with options like TRICARE Prime, Extra, and Standard. These programs are also supplemented by SGLI for life insurance benefits for active and retired military personnel.