Benefits and Provisions

Disability income insurance can solve the financial problem created by a disability. This type of health insurance pays monthly income benefits if the insured becomes unable to work and earn a living because of sickness or injury.

Disability income insurance includes some logical restrictions. To discourage malingering (faking an illness or disability to collect insurance benefits), insurers place strict controls on how much disability income a person can receive. In general, insurers limit disability income benefits to less than 100% of the insured’s gross income.

Because benefits paid from a policy for which the insured pays the premium are not taxed, it’s usually sufficient to insure your net earned (after-tax) income. Policy limits seldom exceed 70% of gross income, because allowing more may violate the principle of indemnity.

Elimination period

The elimination period, also called the waiting period, is the amount of time that must pass after a disability begins before benefit payments start.

Conceptually, the elimination period is similar to a deductible in other policies. In both cases, the goal is to reduce the number of small claims (and therefore keep premiums lower) by requiring the insured to absorb relatively minor losses.

Benefit period

Disability income policies include a provision that states how long benefits will be paid. Although many benefit periods are available, the most common arrangement is for benefits to be payable until the insured reaches age 65.

- Short-term policies typically pay benefits for up to 6 months, and sometimes as long as 1 year.

- Long-term policies generally pay benefits for 2 years, 5 years, to age 65, or even for life.

It’s common for an insured to have two disability income policies: one short-term and one long-term.

- The short-term policy typically has a 7-day waiting period before coverage begins and pays benefits for up to 13, 26, or 52 weeks.

- The long-term policy is designed to take over when short-term benefits end and to continue benefit payments for a specified number of years, to age 65, or for life.

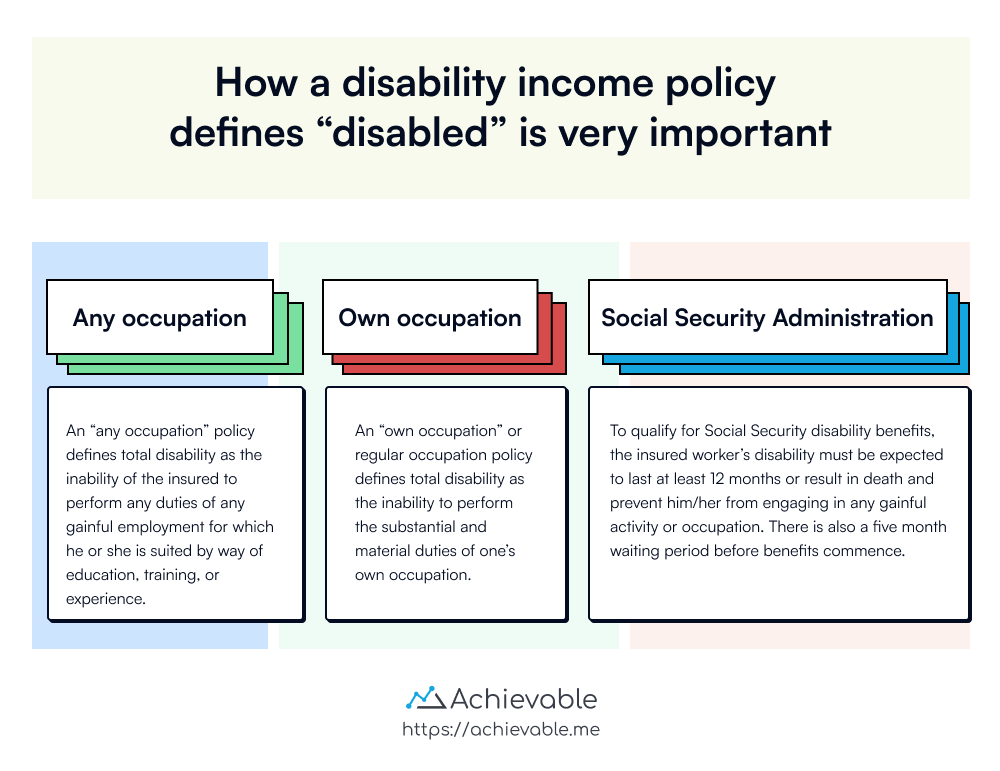

A typical disability income policy pays benefits when the insured becomes totally disabled. As the name implies, total disability means being unable to perform the duties of one’s occupation. Policies generally use one of two definitions of total disability. One definition is less restrictive than the other and, as a result, is more expensive. Because of this, the policy’s definition of disability is a key provision.

An “any occupation” policy defines total disability as the inability of the insured to perform the duties of any gainful employment for which he or she is suited by education, training, or experience. Under this definition, the person must be so disabled that they cannot engage in any employment they could reasonably be expected to perform.

The second, less restrictive definition is “own occupation.” An own occupation policy defines total disability as the inability to perform the duties of one’s own occupation.

Here’s why this is less restrictive for the policy owner. Suppose a dentist buys a policy and later loses a hand. The dentist will never again be able to perform the duties of dentistry, but could reasonably be expected to work in other occupations. With an own occupation policy, benefits would be payable; an any occupation policy would not pay benefits in this situation.

It’s also common for policies to combine these concepts. For example, a policy may define total disability as:

- the inability to perform your own job for the first 2 years after the sickness or injury begins, and

- the inability to perform any job for which you are reasonably suited by education, training, or experience after that.

Other definitions of disability

Partial disability

- Many disabilities improve gradually. During recovery, a person may be able to return to work on a limited basis before fully recovering. A policy with a partial disability provision pays reduced benefits during this period.

- Partial benefits are typically limited to a short period to discourage malingering.

- Although partial disability often follows a period of total disability, partial disability benefits may also be paid at the onset of a disability.

Residual disability

- With residual disability provisions, benefits are tied to the proportion of earnings lost while the insured is disabled.

- Unlike a partial disability provision (which focuses on limited work hours), a residual benefit is based on the percentage of pre-disability income the insured is no longer receiving.

- Example: If an insured returns to work full time but earns only 60% of pre-disability income, the policy might pay 40% of the total disability benefit (because earnings have dropped by 40%).

- The objective of the residual benefit is to encourage people to return to work, even on a partial basis, without fear of losing income.

- A key feature of residual benefits is that the policy owner can return to work in any occupation (even a lower-paying job) without losing all disability income benefits.

Recurrent disability

- A disability may recur after the policy owner appears to have recovered.

- If the disabled individual returns to work and then suffers a relapse within 90 days, it is treated as a continuation of the original disability, and a new elimination period will not be imposed.

Presumptive disability

- In most cases, disability income benefits are payable only while the insured is under a physician’s care.

- Insurers commonly require regular physician statements to support the continuing disability.

- Some conditions are presumed to be totally disabling based on their nature. Examples include loss of sight, loss of use of 2 limbs, or loss of hearing and speech.

- In these cases, the insured is not required to provide continuing proof of disability.

A disability income policy may also distinguish between confining and non-confining disability.

- A confining policy requires the insured to be confined in a hospital or other facility to qualify for income benefits.

- Most policies are non-confining. If the insured meets the policy’s definition of disabled, there is no confinement requirement.

Disability income policies may also use different definitions of “accident.”

A policy with an accidental means clause covers accidents only if the cause was unintentional. This can be restrictive. For example, you are riding a bus that is pulling up to the curb but has not come to a complete stop. You choose to jump from the bus and break your leg. Because you intended to jump, a policy with an accidental means clause would not cover the injury. However, if you slipped and fell off the bus, the act leading to the injury would have been unintentional, and you would be covered.

Most policies use an accidental bodily injury clause, which is less restrictive. Any injury that results from an accident is covered, even if the action that led to the injury was intentional.

Lesson summary

Disability income insurance is designed to provide financial assistance if the insured becomes unable to work due to sickness or injury. Below are the key features and considerations of disability income insurance:

- Restrictions on disability income insurance:

- Benefits are typically limited to less than 100% of the insured’s gross income to deter malingering.

- Policy limits usually do not exceed 70% of gross income to adhere to the principle of indemnity.

- Elimination period:

- The waiting period before benefit payments begin after the onset of disability.

- Similar to a deductible, it aims to minimize claims and premiums by making the insured wait.

- Benefit period:

- Specifies the duration for which benefits will be paid.

- Most common benefit period lasts until the insured reaches age 65.

- Types of disability:

- Total disability: Inability to perform one’s occupation, with variations like “any occupation” or “own occupation.”

- Partial disability: Allows for reduced benefits during recovery.

- Residual disability: Benefits are tied to the earnings lost while disabled.

- Recurrent disability: Covers relapses of the original disability without imposing a new elimination period.

- Presumptive disability: Provides benefits without requiring ongoing proof of disability for certain conditions like loss of sight or limbs.