In California, the Insurance Commissioner isn’t just a bureaucratic official—they are elected directly by the people. This makes California one of the few states where voters themselves choose the top insurance regulator, giving the role an unusual level of accountability to the public rather than to politicians or industry insiders.

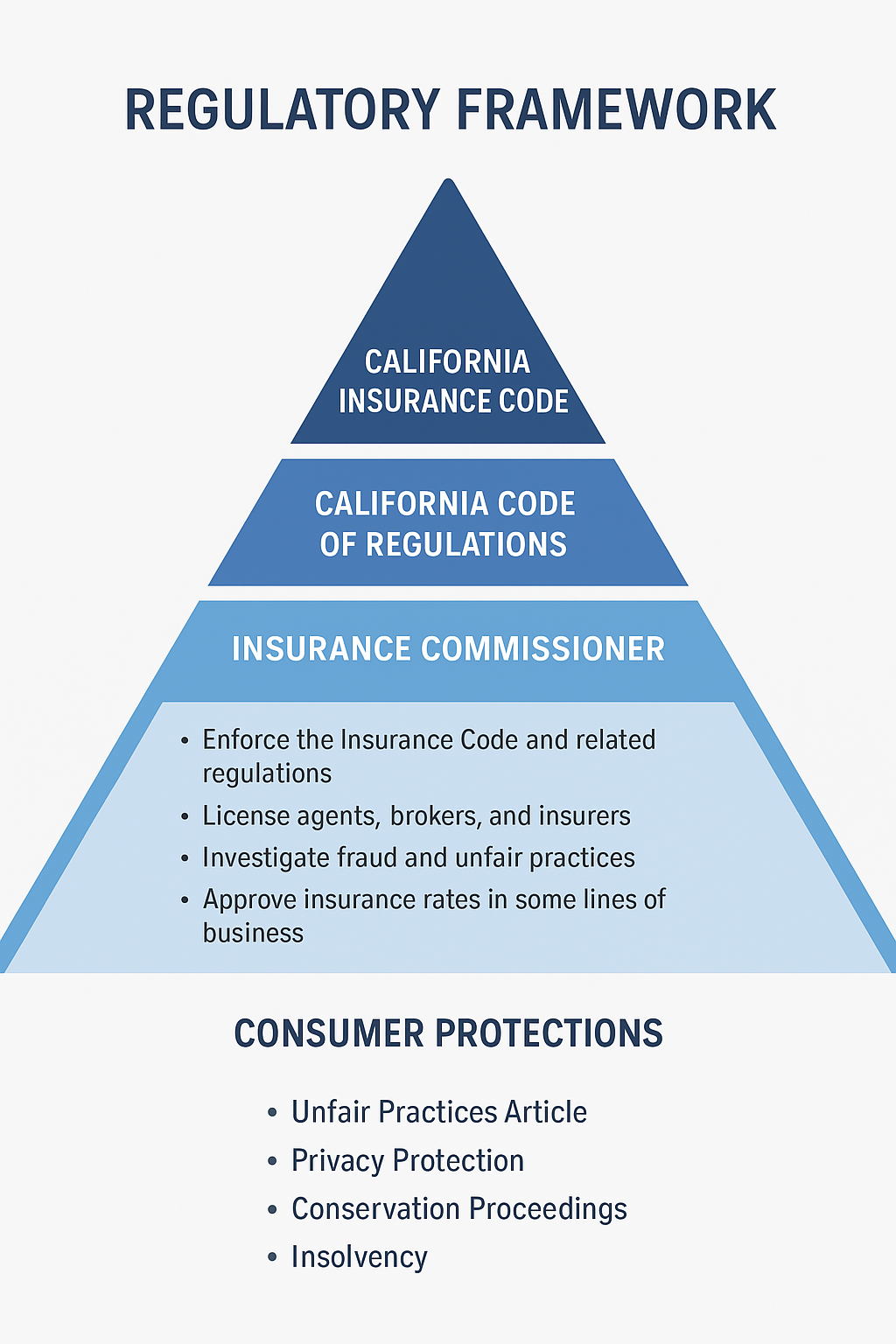

The Commissioner wears many hats. On one hand, they act as a regulator, making sure insurance companies, agents, and brokers are licensed and playing by the rules. On the other hand, they serve as a consumer advocate, ensuring that rates are fair, fraud is investigated, and complaints from everyday policyholders are taken seriously.

The Commissioner also has significant power over rates in certain lines, such as auto and homeowners insurance—meaning their decisions can directly affect how much Californians pay for coverage.

California’s insurance regulation system is designed to balance three goals: consumer protection, insurer solvency, and fair competition. The framework relies on both statutory law and administrative rules, with strong enforcement authority granted to the California Department of Insurance (CDI).

Understanding statutory language is essential. Some of the common legal terms in the California Insurance Code without common sense meanings include: Keypoints are for summarizing sections, chapters, and ideas.

Scope of Coverage:

Licensing requirements for agents, brokers, and insurers

Solvency standards and capital requirements for insurers

Rules for insurance contracts and disclosures

Claims handling and fair claims settlement practices

Anti-fraud provisions (e.g., mandatory SIUs, fraud warning statements)

Consumer protections, including privacy and unfair practice prohibitions

Living Law:

The CIC evolves continuously through legislative updates, ballot initiatives, and regulatory amendments.

This ensures responsiveness to emerging risks (e.g., wildfire coverage rules, cyber insurance, consumer privacy).

Example: CIC requires that every insurance policy contain certain elements (CIC §381), including the parties, subject of insurance, risks insured, coverage period, and premium basis.

Purpose:

The CIC explains what the law requires.

The CCR provides the detailed rules on how to comply.

Enforcement Role:

Failure to comply with CCR requirements can result in regulatory penalties, fines, or license suspension.

Insurers and agents are held accountable not just to the CIC’s broad provisions, but also to the technical details in the CCR.

Example:

CIC requires insurers to maintain Special Investigation Units (SIUs) (Cal. Ins. Code §§1875.20–1875.23).

| Category | California Insurance Code (CIC) | California Code of Regulations (CCR), Title 10, Chapter 5 |

| What it is | Statutory law enacted by the California Legislature | Administrative rules issued by the California Department of Insurance (CDI) |

| Purpose | Defines the legal requirements governing the business of insurance | Explains how to comply with the CIC’s requirements in detail |

| Authority | Legislative authority (laws passed by elected officials) | Regulatory authority (rules created by CDI under CIC delegation) |

| Scope | Covers procedures, operational standards, invalidation | Covers procedures, operational standards, reporting rules, enforcement practices |

| Enforcement | Violations can lead to fines, rescission, policy invalidation | Violations can lead to administrative penalties, sanctions, or loss of license |

| Update Process | Changed through legislation or ballot initiatives | Updated by CDI rulemaking (with public notice and comment) |

Sign up for free to take 5 quiz questions on this topic