Long straddles

When you can’t confidently predict the market’s direction but you do expect volatility, a long straddle can be a good strategy. It can profit if the stock price moves significantly up or down.

These are the components of a long straddle:

Long call & long put*

*Must be the same strike price and expiration

For example:

Long 1 ABC Jan 60 call

Long 1 ABC Jan 60 put

As you already know, a long call contract provides the “right to buy,” while a long put contract provides the “right to sell.” The long call is bullish (it benefits if the market price rises). The long put is bearish (it benefits if the market price falls). When an investor buys both options, they’re betting on market volatility rather than direction.

If the stock’s market price rises above the call’s strike price (“call up”), the investor can exercise the call and potentially profit. The stock would be purchased at the call’s strike price and sold at the higher market price. If the gain from exercising the call is greater than the total premiums paid (for both options), the investor has an overall profit.

If the stock’s market price falls below the put’s strike price (“put down”), the investor can exercise the put and potentially profit. The stock would be purchased at the lower market price and sold at the higher strike price. If the gain from exercising the put is greater than the total premiums paid (for both options), the investor has an overall profit.

On the surface, long straddles can look appealing because they can profit in either a bull or bear move. The trade-off is cost: you pay two premiums to enter the position. That means the winning option must gain enough intrinsic value to cover both premiums. If the stock stays near the shared strike price, the investor can lose up to the combined premiums.

Let’s take a look at several scenarios to understand long straddles better:

An investor goes long 1 ABC Jan 60 call at $4 and long 1 ABC Jan 60 put at $5 when ABC’s market price is $60. What is the gain or loss if ABC’s market price rises to $100?

Can you figure it out?

Answer = $3,100 gain

| Action | Result |

|---|---|

| Buy call | -$400 |

| Buy put | -$500 |

| Exercise call - buy shares | -$6,000 |

| Sell shares | +$10,000 |

| Total | +$3,100 |

At $100, the call is “in the money” (has intrinsic value), and the put is “out of the money” (no intrinsic value). The put expires worthless, but the call is exercised, allowing the investor to buy ABC shares at $60. The shares are then sold at $100, creating a $40 gain per share, or $4,000 total ($40 x 100 shares). The $900 combined premium paid upfront reduces the gain to $3,100.

This is what the investor wanted: a large move. Even though only one option finished in the money, the call gained enough intrinsic value to more than offset the combined premium of $900.

The maximum gain for a long straddle is unlimited*. The further the market rises, the more intrinsic value the call option gains.

What happens if the market rises by a small amount?

An investor goes long 1 ABC Jan 60 call at $4 and long 1 ABC Jan 60 put at $5 when ABC’s market price is $60. What is the gain or loss if ABC’s market price rises to $69?

Answer = $0 (breakeven)

| Action | Result |

|---|---|

| Buy call | -$400 |

| Buy put | -$500 |

| Exercise call - buy shares | -$6,000 |

| Sell shares | +$6,900 |

| Total | $0 |

At $69, the call is “in the money” (has intrinsic value) and the put is “out of the money” (no intrinsic value). The put expires worthless, but the call is exercised, allowing a purchase of ABC shares at $60. The shares are then sold at $69, creating a $9 gain per share, or $900 total ($9 x 100 shares). The $900 combined premium paid upfront exactly offsets the gain, so the position breaks even.

$69 is one of two breakevens for this example (we’ll discuss the other breakeven later). On the upside, a long straddle breaks even when:

- the stock price is above the strike price by an amount equal to the combined premiums

So the upside breakeven is the shared strike price ($60) plus the combined premium ($9).

Let’s try another example:

What happens if the market rises by a small amount?

An investor goes long 1 ABC Jan 60 call at $4 and long 1 ABC Jan 60 put at $5 when ABC’s market price is $60. What is the gain or loss if ABC’s market price rises to $62?

Answer = $700 loss

| Action | Result |

|---|---|

| Buy call | -$400 |

| Buy put | -$500 |

| Exercise call - buy shares | -$6,000 |

| Sell shares | +$6,200 |

| Total | -$700 |

At $62, the call is “in the money” (has intrinsic value) and the put is “out of the money” (no intrinsic value). The put expires worthless, but the call is exercised, allowing a purchase of ABC shares at $60. The shares are then sold at $62, creating a $2 gain per share, or $200 total ($2 x 100 shares). The $900 combined premium paid upfront more than offsets the gain, resulting in a $700 overall loss.

A lack of volatility is the enemy of a long straddle. Small moves often aren’t enough to overcome the cost of two premiums.

What happens if the market remains flat?

An investor goes long 1 ABC Jan 60 call at $4 and long 1 ABC Jan 60 put at $5 when ABC’s market price is $60. What is the gain or loss if ABC’s market price stays at $60?

Answer = $900 loss

| Action | Result |

|---|---|

| Buy call | -$400 |

| Buy put | -$500 |

| Total | -$900 |

At $60, both options are “at the money,” so both expire worthless (an option must have intrinsic value to be exercised). The result is an overall loss of $900, which is the combined premiums.

This is the worst-case outcome for the investor because it produces the maximum loss.

To find the maximum loss for any long straddle, you can use this formula:

What happens if the market falls a small amount?

An investor goes long 1 ABC Jan 60 call at $4 and long 1 ABC Jan 60 put at $5 when ABC’s market price is $60. What is the gain or loss if ABC’s market price falls to $57?

Answer = $600 loss

| Action | Result |

|---|---|

| Buy call | -$400 |

| Buy put | -$500 |

| Buy shares | -$5,700 |

| Exercise put - sell shares | +$6,000 |

| Total | -$600 |

At $57, the put is “in the money” (has intrinsic value) and the call is “out of the money” (no intrinsic value). The call expires worthless, but the put is exercised after the shares are purchased at the market price. Shares are purchased for $57 and sold at $60, creating a $3 gain per share, or $300 total ($3 x 100 shares). The $900 combined premium paid upfront more than offsets the gain, resulting in an overall loss of $600.

Again, the issue is insufficient volatility: the move wasn’t large enough to cover the combined premiums.

What happens if the market falls a little further?

An investor goes long 1 ABC Jan 60 call at $4 and long 1 ABC Jan 60 put at $5 when ABC’s market price is $60. What is the gain or loss if ABC’s market price falls to $51?

Answer = $0 (breakeven)

| Action | Result |

|---|---|

| Buy call | -$400 |

| Buy put | -$500 |

| Buy shares | -$5,100 |

| Exercise put - sell shares | +$6,000 |

| Total | $0 |

At $51, the put is “in the money” (has intrinsic value) and the call is “out of the money” (no intrinsic value). The call expires worthless, but the put is exercised after the shares are purchased at the market price. Shares are purchased for $51 and sold at $60, creating a $9 gain per share, or $900 total ($9 x 100 shares). The $900 combined premium paid upfront exactly offsets the gain, so the position breaks even.

$51 is the other breakeven for this strategy. On the downside, a long straddle breaks even when:

- the stock price is below the strike price by an amount equal to the combined premiums

So the downside breakeven is the shared strike price ($60) minus the combined premium ($9).

Here’s the general formula for breakeven on straddles:

You’ll learn more about this in the next section, but the breakeven formula is the same for both long and short straddles.

Straddles are one of the only options strategies with multiple breakevens. To find both quickly:

- Add up the combined premiums.

- Add the combined premiums to the shared strike price (upside breakeven).

- Subtract the combined premiums from the shared strike price (downside breakeven).

In this example, the two breakevens are $51 and $69.

What happens if the market falls significantly?

An investor goes long 1 ABC Jan 60 call at $4 and long 1 ABC Jan 60 put at $5 when ABC’s market price is $60. What is the gain or loss if ABC’s market price falls to $25?

Answer = $2,600 gain

| Action | Result |

|---|---|

| Buy call | -$400 |

| Buy put | -$500 |

| Buy shares | -$2,500 |

| Exercise put - sell shares | +$6,000 |

| Total | +$2,600 |

At $25, the put is “in the money” (has intrinsic value) and the call is “out of the money” (no intrinsic value). The call expires worthless, but the put is exercised after the shares are purchased at the market price. Shares are purchased for $25 and sold at $60, creating a $35 gain per share, or $3,500 total ($35 x 100 shares). The $900 combined premium paid upfront reduces the gain to $2,600.

This is another example of the intended outcome: a large move. Even though only one option finished in the money, the put gained enough intrinsic value to offset the combined premium.

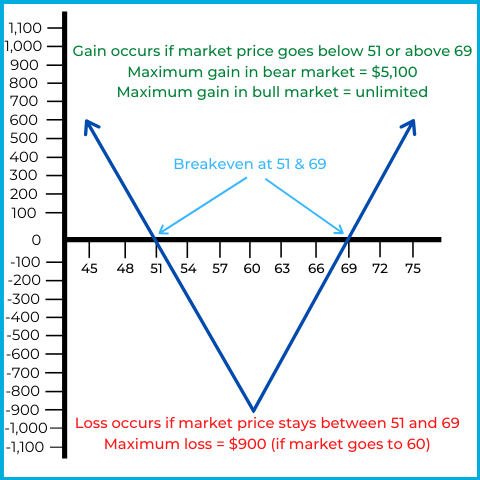

Let’s look at the options payoff chart to summarize the “big picture” of this long straddle. First, let’s re-establish the example:

Long 1 ABC Jan 60 call @ $4

Long 1 ABC Jan 60 put @ $5

Here’s the payoff chart:

The horizontal axis represents the market price of ABC stock, while the vertical axis represents overall gain or loss.

As the long straddle payoff chart shows, the investor reaches their maximum loss of $900 at a market price of $60. At this point, both options expire worthless, and the combined premiums represent the overall loss. If the market price rises above or falls below $60, the call or the put goes “in the money” and gains intrinsic value.

If the market price rises to $69, the long call gains $9 of intrinsic value, offsetting both premiums. Any market price above $69 results in profit, and the gain potential is unlimited. If the market price falls to $51, the long put gains $9 of intrinsic value, offsetting both premiums. Any market price below $51 results in profit, and the investor is eligible for up to $5,100 of gain potential (a $5,100 gain would occur if the market price falls to $0).

In our last few examples, let’s explore what happens if investors close out contracts at intrinsic value. As we’ve learned previously, closing out contracts involves trading the contracts instead of exercising or allowing them to expire.

An investor goes long 1 ABC Jan 60 call at $4 and long 1 ABC Jan 60 put at $5 when ABC’s market price is $60. ABC’s market falls to $45 and the investor closes the contracts at intrinsic value. What is the gain or loss?

Answer = $600 gain

| Action | Result |

|---|---|

| Buy call | -$400 |

| Buy put | -$500 |

| Close call | $0 |

| Close put | +$1,500 |

| Total | +$600 |

At $45, the put is “in the money” (has intrinsic value) and the call is “out of the money” (no intrinsic value). The call has $0 of intrinsic value, so the investor closes the call by selling it for $0 (closing sale). The put has $15 of intrinsic value, so the investor closes the put by selling it for $15 (closing sale). Selling the put for $15 after paying a total premium of $9 results in a $6 per share gain, or $600 overall ($6 x 100 shares).

As a reminder, closing contracts means doing the opposite of the opening transaction. Here, both options were bought to open the long straddle (opening purchases), so both must be sold to close (closing sales). The investor paid $900 for the options and sold them for $1,500, resulting in a $600 gain.

Let’s examine one more scenario involving closing transactions for our last example:

An investor goes long 1 ABC Jan 60 call at $4 and long 1 ABC Jan 60 put at $5 when ABC’s market price is $60. ABC’s market rises to $66 and the investor closes the contracts at intrinsic value. What is the gain or loss?

Answer = $300 loss

| Action | Result |

|---|---|

| Buy call | -$400 |

| Buy put | -$500 |

| Close call | +$600 |

| Close put | $0 |

| Total | -$300 |

At $66, the call is “in the money” (has intrinsic value) and the put is “out of the money” (no intrinsic value). The put has $0 of intrinsic value, so the investor closes the put by selling it for $0 (closing sale). The call has $6 of intrinsic value, so the investor closes the call by selling it for $6 (closing sale). Selling the call for $6 after paying a total premium of $9 results in a $3 per share loss, or $300 overall ($3 x 100 shares).

As in the previous example, both options were bought to open the long straddle (opening purchases), so both must be sold to close (closing sales). The investor paid $900 for the options and sold them for $600, resulting in a $300 loss.

This video covers the important concepts related to long straddles:

For suitability, long straddles should only be recommended to aggressive options traders if volatility is expected. Although the maximum loss is limited to the premiums, losses can add up quickly due to the short-term nature of options. The investor realizes a loss if volatility does not materialize before expiration (9 months or less for standard options).