Navigating Cash Value and Risk

To understand how whole life insurance works (and how it differs from term insurance), you first need to understand the concept of amount at risk. The amount at risk is the dollar value of the risk the insured represents to the insurer. In other words, it’s the amount the insurer would have to pay to settle a claim.

A person generally represents a greater risk at older ages. Insurers reflect this through a mortality charge that increases with age. With an annually renewable term (ART) policy, the policy owner pays a higher mortality charge each year, which leads to rising premiums. However, most term life insurance sold today is level term, where the premium stays fixed for a set number of years (for example, 10, 20, or 30), even though the risk of death increases with age.

A term policy does not accumulate cash value. With a $100,000 term policy, the insurer’s amount at risk is $100,000. That means if the insured dies while the policy is in force, the insurer would have to pay $100,000. Each year, the insured gets older and the probability of death increases. As a result, the mortality charge increases, and that increase is reflected in the premium.

With permanent insurance, the net amount at risk decreases each year. In a whole life policy, the amount at risk at any point in time is the difference between:

- The face amount of the policy, and

- The cash value

The cash value represents a reserve fund (or excess premiums paid in the early years) that can be used to offset the need for higher premiums later.

As the cash value increases, the insurer’s amount at risk decreases. As the amount at risk decreases, a larger portion of the level premium can be allocated to the policy’s cash value. At the same time, the risk of death (and the mortality charge) increases with age. The net result is that these two forces counterbalance each other, producing a level premium.

Another way to say this is:

- In the early years, insurers charge more than is needed to cover the mortality risk.

- In later years, insurers charge less than the mortality risk would otherwise require.

Cash value features

Cash value builds up in the early years of a policy to subsidize the cost of protection during the later years. There are no federal or state taxes imposed on the accumulation of cash value inside a life insurance policy.

Whole life policies are structured so that the cash value gradually approaches the face amount until age 100 (or 121 in many modern policies), when the two are equal. At that point, the insurer’s amount at risk is $0 and the policy matures. Because the face amount and the cash value are equal, there is no longer a reason for the insurer to hold the cash value, and the insurer will pay the insured the face amount of the policy.

A key feature of cash values is that the policy owner may access them through a policy loan. Insurers charge a nominal interest rate on policy loans, and the maximum rate is regulated by state law. If the insured dies before the policy loan is repaid, the death benefit paid to the beneficiary is reduced by the amount of the loan plus any accrued interest.

In practice, policy loans are an important feature of whole life insurance. For the purpose of the pre-license exam, you should know that:

- A loan provision exists

- It is only available on whole life insurance (not term and not annuities)

- The owner of the policy is the one who has access to cash value via policy loan (not the insured and not the beneficiary)

- Policy loans are generally tax-free while the policy remains in force; however, if the policy lapses with an outstanding loan, the loan may be treated as taxable income

- Death benefits will be reduced by the amount of any outstanding loan

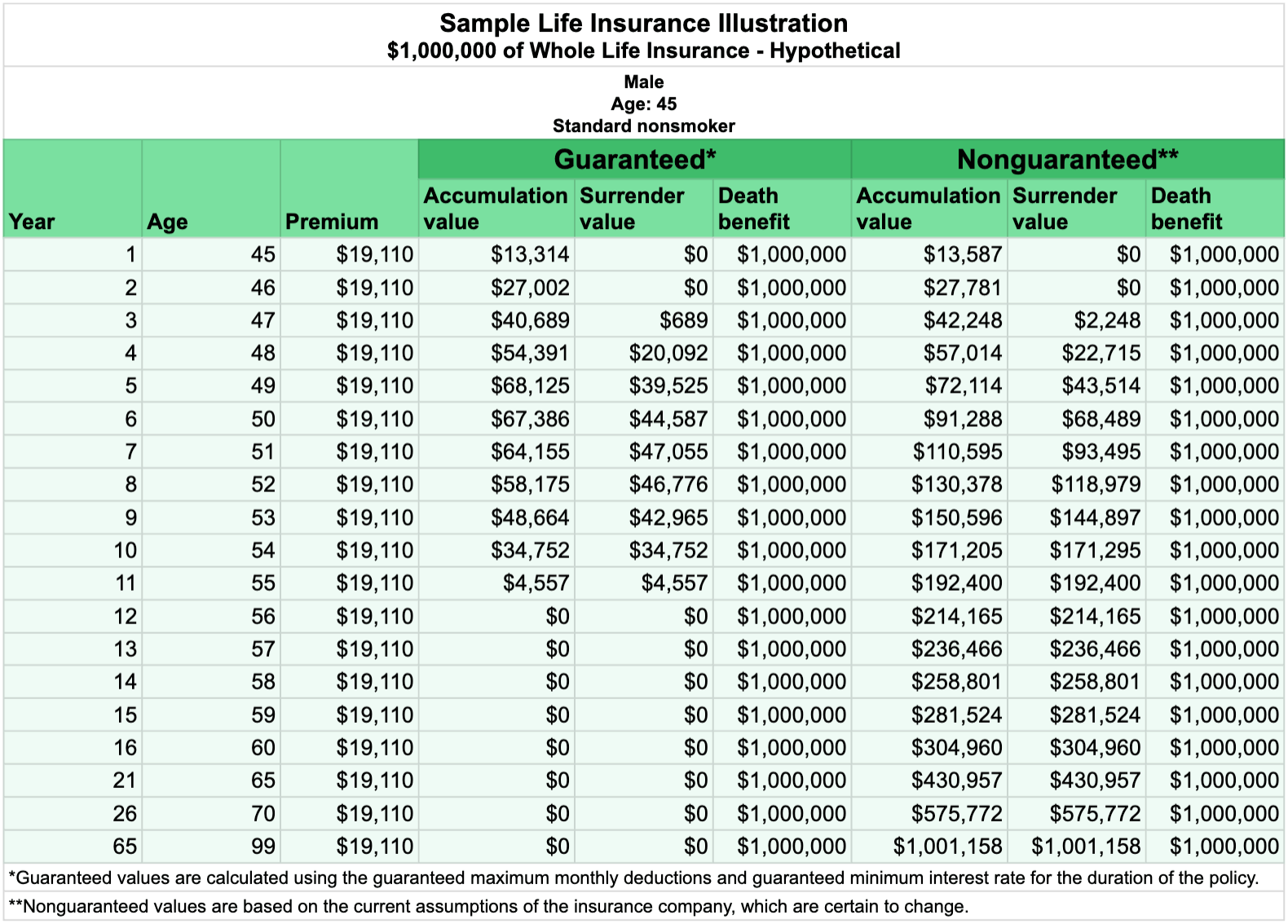

Illustrations

An illustration shows how non-guaranteed benefits may change as interest rates and other factors change, and it also shows what the insurer guarantees.

An illustration typically has two key components:

-

The guaranteed illustration. This is the legally required disclosure of a worst-case scenario. It outlines policy performance based on the carrier’s minimum filed credit rates for a particular policy and the maximum mortality charges using the appropriate commissioner’s standard mortality table (such as the 2001 or 2017 CSO, depending on the policy’s issue date).

-

The current illustration. This is the insurer’s representation of policy performance based on credit rates and mortality charges currently in effect.

Policy terms and features

These provide an overview of the main elements of the policy and a way to confirm that the policy’s premium stream and projected benefits match the client’s needs and ability to pay.

Disclaimer

This advises readers that the illustration is not an estimate of future values and that actual results could be more or less favorable.

Signature page

This shows a numeric summary of the illustration in 5- and 10-year increments. The applicant signs a statement acknowledging that the nonguaranteed elements are subject to change. The producer signs to confirm that he or she has explained that the nonguaranteed elements are subject to change.

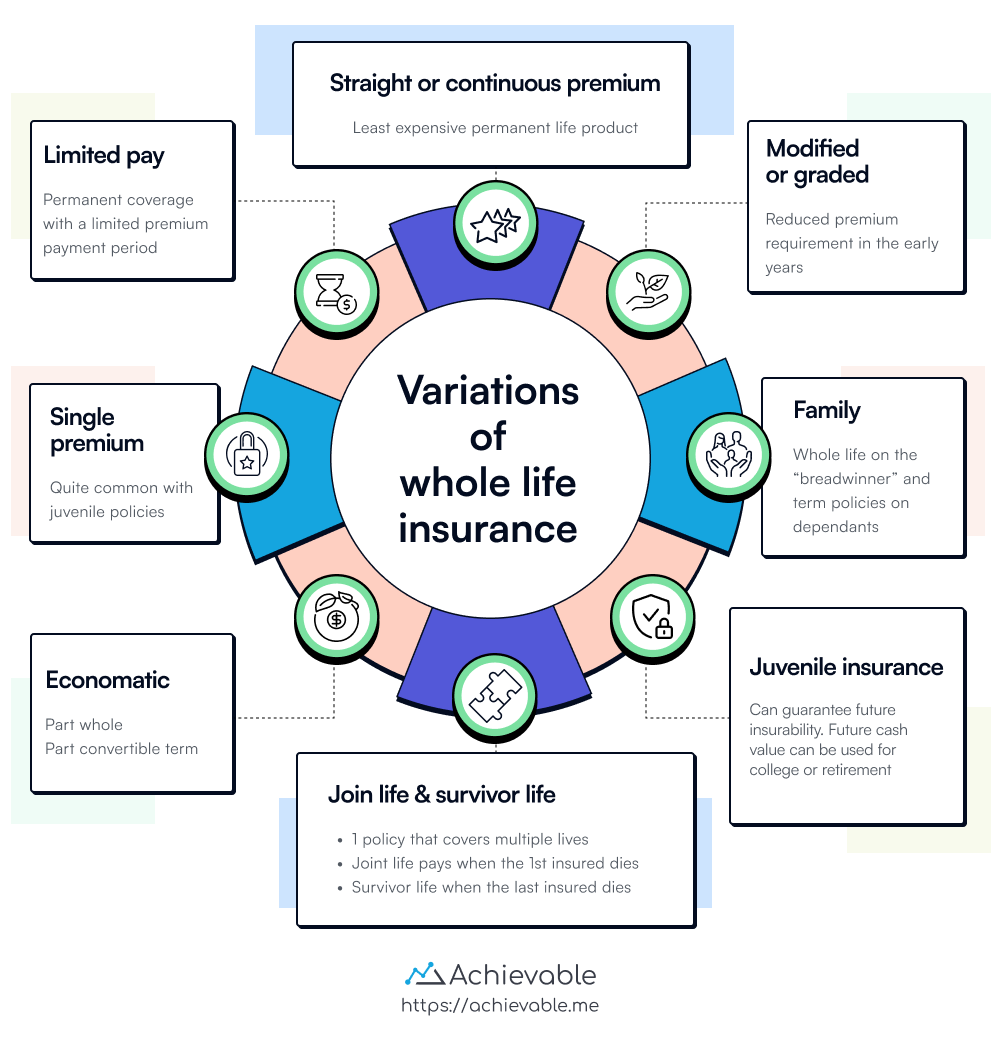

Straight life

The most common form of whole life insurance is the straight life policy, with equal premium payments spread out for the life of the insured (or to age 100 for most older policies, or 121 for many newer policies).

Modified life

This is a form of whole life insurance in which premiums are lower for a specified period of time (for example, 5 years). After that period, the premium increases for the remainder of the policy term. This is popular with people who have a smaller budget in their younger years. Because early premiums are reduced, cash values accumulate more slowly than with a straight life policy.

Graded premium whole life

This is a form of modified whole life, except that premiums increase steadily rather than in one single jump. Cash values accumulate very slowly because the premium in the early years can be as much as 50% less than that of a comparable straight life policy.

Limited pay whole life

With a limited pay whole life policy, the premium-paying period is shorter than with a straight life policy, although coverage continues for the insured’s entire life. Premium payments are higher than with a straight life policy of comparable face amount. As a result, cash values accumulate faster than they do with a straight life policy.

The most common forms of limited pay policies are the 20-pay life, in which premiums are paid for 20 years, and LP65, in which premiums are paid to age 65.

Single pay life

It’s rare, but it is possible to pay up a policy with one premium payment, which creates an immediate cash value.

Combination policies

Although term and whole life insurance are the two basic forms of life insurance, insurers have developed policies that combine features of both. Known as combination policies, they are designed to meet specific life insurance needs.

Economatic whole life is a whole life policy with a convertible term rider that uses dividends to convert the term to paid-up whole insurance over time.

Family policy

The most common form of combination policy is the family policy. A whole life policy is issued to the breadwinner, and level term policies are issued on the spouse and each child. As new children are born, they are automatically covered. A convertibility option is added to each term policy to protect the children’s insurability.

Family income

The purpose of a family income policy is to guarantee that income will be provided to surviving family members if the breadwinner dies prematurely. It uses a decreasing term policy attached as a rider to an underlying whole life policy. The rider provides the funds needed to pay a predetermined income to the beneficiary for the remainder of a specified period of time.

For example, if Zack Luna buys a 15-year family income policy and dies 2 years later, the monthly income benefit would be paid for the following 13 years. Death 7 years after issuance would result in payments for the remaining 8 years. Death at or after 15 years would produce no income benefit payments.

Family maintenance

A family maintenance policy is similar to a family income policy, but it provides monthly income for a set period of time. It uses a level term policy rider added to the underlying whole life rather than a decreasing term rider.

Using the example above, the family maintenance policy would provide monthly income for 15 years, whether the breadwinner dies today or in 14 years. In the example above, if the breadwinner died in 14 years, the family would receive monthly income for one year. With a family maintenance policy, it would continue for 15 years from the date of death.

Lesson summary

To understand whole life insurance, you need to understand the concept of amount at risk. Key points include:

- The amount at risk is the monetary value the insured represents to the insurer.

- With an annually renewable term policy, premiums rise each year as the mortality charge increases. With a level term policy, premiums remain fixed for a set number of years.

- Unlike term insurance, whole life insurance accumulates a cash value over time.

- The cash value acts as a reserve fund and offsets the need for higher premiums in later years.

- As cash value increases, the amount at risk decreases, which helps support a level premium.

Cash value features include tax advantages and policy loans:

- Cash value builds up early on to support later premium costs.

- Cash value accumulation is tax-deferred while the policy remains in force.

- Policy owners can access cash value through policy loans with regulated interest rates.

Whole life policies come in several forms, including Straight Life, Modified Life, Graded Premium Whole Life, Limited Pay Whole Life, and Single Pay Life. Each type has different premium patterns and cash value accumulation. These features are shown in policy illustrations, which include guaranteed and current illustrations. Combination policies such as Family Policy, Family Income, and Family Maintenance meet specialized needs by combining features of term and whole life insurance.