Taxation of Life Insurance Products

Tax consequences of annuities

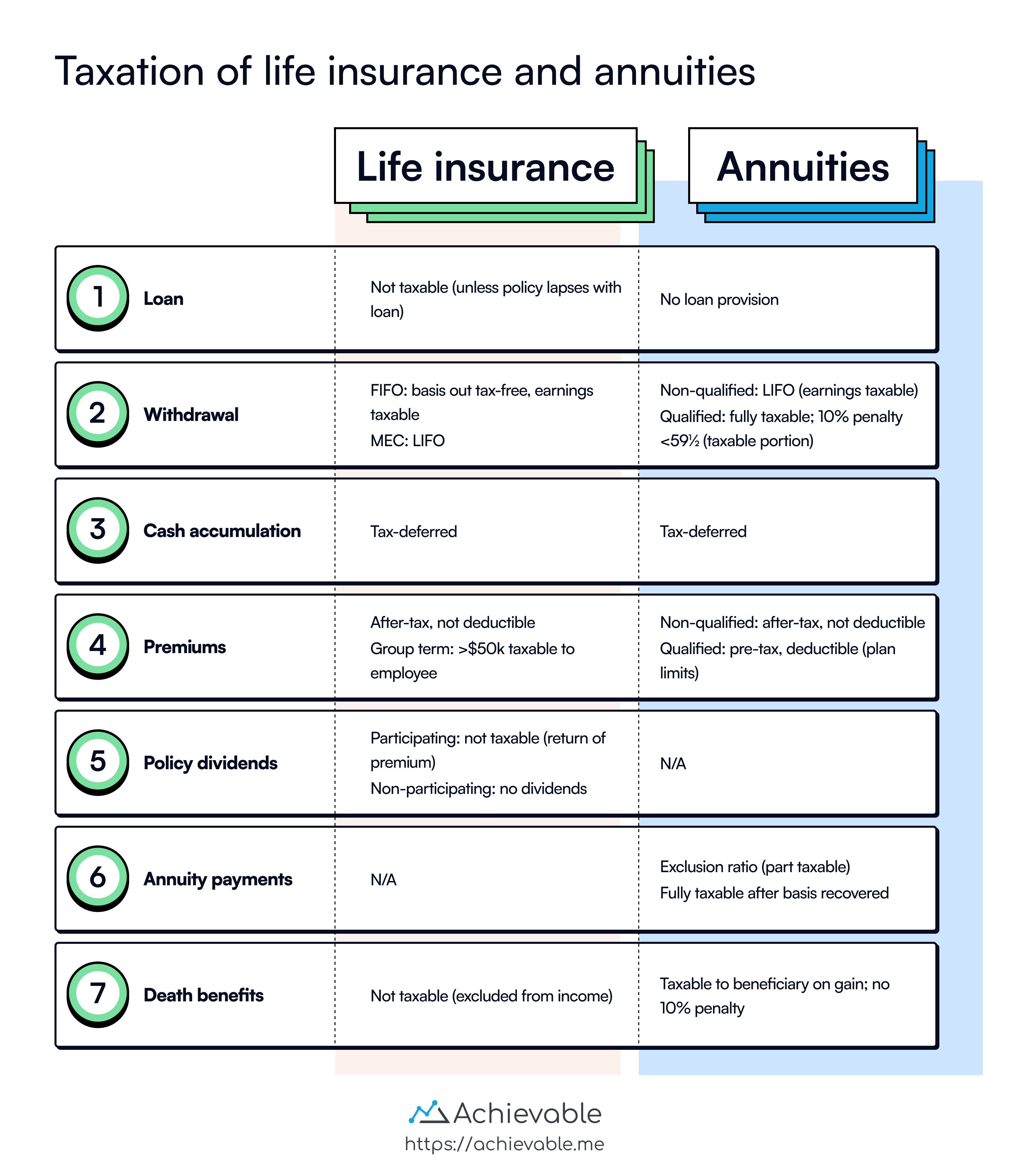

Tax treatment of premiums:

- For non-qualified annuities, contributions are not tax-deductible, and there is no IRS contribution limit.

Tax treatment of cash accumulation:

- All growth in an annuity is tax-deferred until withdrawn.

Tax consequences of a withdrawal:

-

For non-qualified annuities, withdrawals follow the LIFO rule: interest (earnings) comes out first and is taxable, then principal (basis) comes out tax-free. For qualified annuities, withdrawals are generally fully taxable since contributions were pre-tax.

-

Withdrawals made before age 59½ are subject to a 10% IRS penalty in addition to ordinary income tax. Exceptions include annuitization, death, disability, certain medical expenses, substantially equal periodic payments (SEPPs), and a qualified birth or adoption distribution (QBAD). Under the SECURE Act, a QBAD lets an individual withdraw up to $5,000 per qualifying birth or adoption without the 10% penalty, though the distribution is still subject to ordinary income tax.

Tax consequences of annuity payments:

- Taxation of annuity payments differs from withdrawals during the accumulation stage. The 10% penalty does not apply to an annuity contract that has been annuitized, regardless of the annuitant’s age. When an annuitant receives an annuity payment, the tax liability is proportional to the percentage of the payment attributable to growth. The exclusion ratio is the portion of an annuity payment that is not subject to income tax when received, because it’s treated as a return of the original principal.

Tax treatment of life insurance

Tax treatment of premiums:

-

Premiums paid for any individual life insurance policy are a personal expense and are not tax-deductible.

-

Premiums paid to fund group life insurance plans are tax-deductible by the employer, and generally, employees covered under a group health plan are not taxed on benefits received from group insurance. There is one exception:

-

Employer-paid premiums for group term life insurance are deductible to the employer. The cost of up to $50,000 of coverage is excluded from the employee’s income; the cost of coverage over $50,000 is taxable to the employee (imputed income).

Tax treatment of cash value accumulation:

- The growth of a life insurance policy’s cash value accumulates on a tax deferred basis.

Tax treatment of policy dividends:

- In a participating policy, dividends paid to the policy owner are considered by the IRS to be a return of excess premium and are not taxable. Non-participating policies do not pay dividends to policyholders at all.

Tax treatment of death benefits:

- The IRS generally excludes life insurance policy proceeds from the beneficiary’s gross income. This is perhaps the most significant tax advantage of life insurance. It allows a person to provide for the economic security of a spouse or business associate without creating an income tax liability for the beneficiary.

- Exception - estate inclusion rule: If the insured transfers ownership of a policy and dies within three years of the transfer, the death benefit may be included in the insured’s gross estate for federal estate tax purposes.

Tax consequences of a policy surrender/withdrawal:

- Withdrawals from a standard (non-MEC) life insurance policy follow FIFO: premiums paid (basis) come out first tax-free, then any earnings are taxable. If the policy is classified as a Modified Endowment Contract (MEC), withdrawals follow LIFO: taxable earnings first, then basis.

Tax treatment of policy loans:

- Policy loans are an important feature of any whole life policy. When a policy loan is made by the insurer, it is made with interest, but it is not a taxable event.

Lesson summary

Life insurance products and annuities have specific tax consequences that individuals should be aware of:

-

Annuities premiums: Contributions are not tax deductible, and there is no maximum contribution limit.

-

Annuities cash accumulation: Growth in an annuity is tax-deferred until withdrawal.

-

Annuities withdrawal:

- For non-qualified annuities, withdrawals are taxed LIFO (interest first).

- For qualified annuities, withdrawals are fully taxable as ordinary income.

- Withdrawals before age 59½ may incur a 10% IRS penalty on the taxable portion, unless an exception applies (annuitization, death, disability, medical expenses, SEPPs, a qualified birth or adoption distribution up to $5,000, etc.).

-

Annuity payments:

- Payments are taxed proportionally to the growth percentage.

- The 10% penalty doesn’t apply to annuitized contracts.

-

Life insurance premiums:

- Individual policy premiums are not tax-deductible.

- Group life insurance premiums are tax-deductible for the employer, and the cost of coverage above $50,000 is taxable to employees.

-

Life insurance policy dividends: Dividends in participating policies are considered return of excess premium and are not taxable. Non-participating policies do not pay dividends to policyholders.

-

Life insurance death benefits: Usually excluded from the beneficiary’s gross income, making it a significant tax advantage.

-

Life insurance policy surrender/withdrawal: Life Insurance Policy Surrender/Withdrawal: Withdrawals are tax-free up to the cost basis in standard (non-MEC) policies; MECs are taxed on a LIFO basis (earnings first).

-

Life insurance policy loans: Policy loans are not taxable events, though interest may apply.