Annuity Basics and Accumulation

Annuities originated from the life income settlement option offered by a life insurance policy. Annuities are insurance products, but they aren’t designed to provide protection in the event of premature death. Instead, an annuity protects you against living too long and outliving your financial resources. The payments from an annuity are guaranteed for a fixed period - commonly for life - so the annuitant can’t outlive the stream of monthly payments.

Annuities are often used to accumulate funds for retirement. As with life insurance, premiums paid aren’t tax-deductible, but they grow tax-deferred until withdrawn. Because of tax-deferred growth and unlimited contribution amounts, annuities are popular with people in high tax brackets.

Annuities may be purchased with a lump sum investment (single premium annuity) or with periodic payments. A single premium annuity may also be an immediate annuity if the owner elects to begin receiving payments right away. More commonly, an annuity is purchased over time with periodic payments and payments begin at a future date. This is a flexible premium deferred annuity.

The accumulation stage is the period when the owner is investing money into the contract.

- In a variable annuity, the value is measured in accumulation units tied to separate account investments (insurance-dedicated mutual funds).

- In a fixed or indexed annuity, the account value grows based on the insurer’s general account interest or an index formula - not accumulation units.

During the accumulation stage, the terms of the contract are flexible. Unlike life insurance, there’s no required premium schedule with an annuity, though most contracts impose minimum initial and subsequent contributions. The owner can choose how much and how often to invest, may withdraw funds, and may also terminate the contract during the accumulation stage.

A withdrawal during the accumulation stage is a taxable event. The owner of the annuity contract has an ordinary income tax liability on any withdrawal from an annuity in excess of his/her cost basis. Any taxable withdrawal is also subject to a 10% penalty if the owner is under age 59½.

If the owner of an annuity dies during the accumulation stage, the beneficiary will receive the greater of:

- The cash value of the contract on date of death

- The decedent’s cost basis

If the cash value exceeds the cost basis, the beneficiary will owe ordinary income tax on the excess amount above the decedent’s cost basis. However, the 10% early withdrawal penalty does not apply.

When the owner of an annuity elects to begin receiving guaranteed monthly payments from the annuity, the contract is annuitized. The accumulation units are converted into annuity units, and the contract enters the annuity stage.

Annuitization shouldn’t be taken lightly because it’s irreversible and can’t be altered or canceled. When the contract is annuitized, the owner gives up all rights to the cash value in the contract in exchange for the insurance company’s payout guarantee.

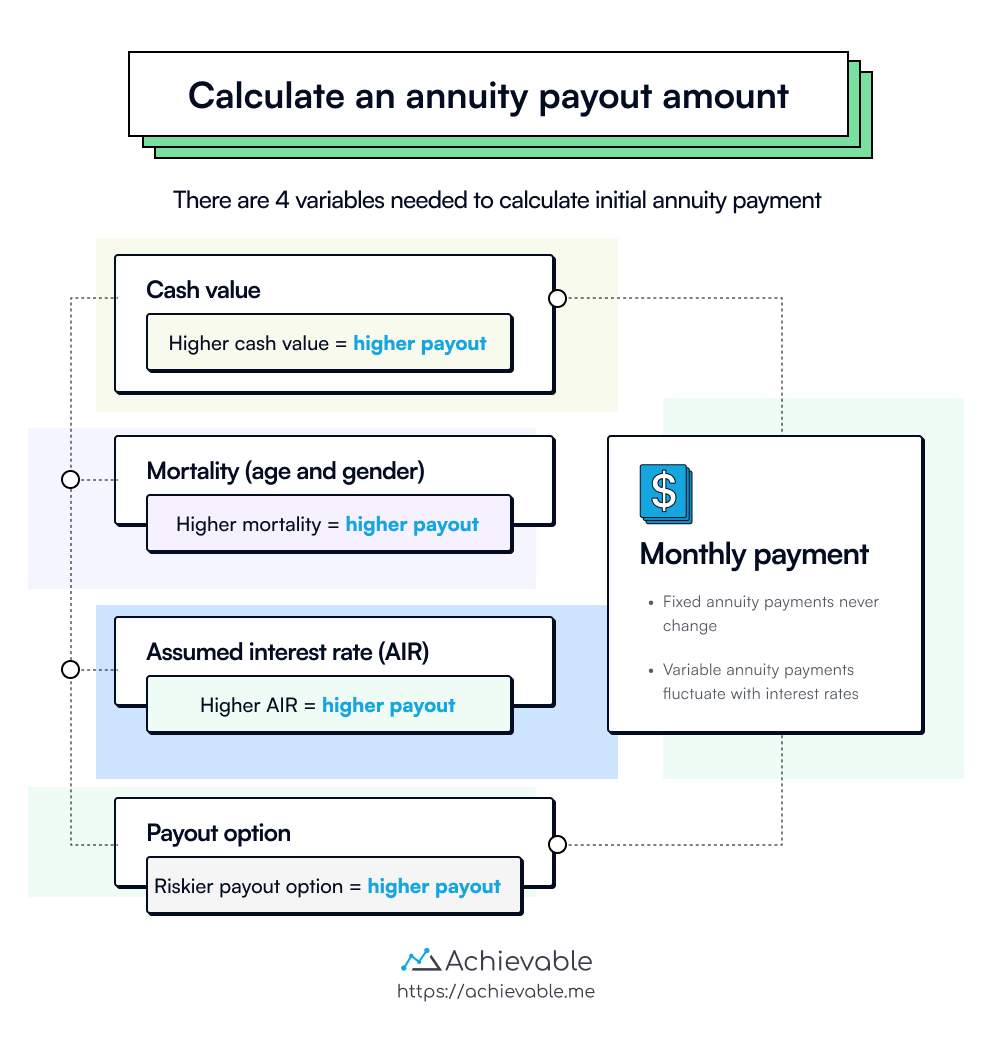

The four variables required to calculate the amount of an annuitant’s initial payment are:

- Life expectancy of the annuitant (age and gender)

- Assumed interest rate (AIR)

- Cash value of the annuity contract

- Payout option

:::

Lesson summary

Annuities originated as a life income settlement option from life insurance policies. They’re designed to protect against outliving financial resources by offering guaranteed payments for a fixed period (commonly for life). They aren’t designed to protect against premature death.

- Annuities can help accumulate funds for retirement. Premiums aren’t tax-deductible, but they grow tax-deferred until withdrawn, which makes annuities popular with individuals in high tax brackets.

- Annuities can be purchased with a lump sum or periodic payments, including single premium immediate annuities and flexible premium deferred annuities.

- During the accumulation phase, the owner has flexibility in how much and how often to invest. There’s no required premium schedule (though minimums apply). The owner may withdraw funds, but withdrawals are taxable events.

- If the owner dies during the accumulation phase, the beneficiary generally receives the greater of the account value or the total premiums paid (cost basis, adjusted), with tax implications.

When the annuity owner chooses to receive guaranteed payments, the contract is annuitized. At that point, the owner gives up access to the cash value in exchange for a payout guarantee from the insurance company.

-

Calculating initial annuity payments involves life expectancy, assumed interest rate, cash value, and payout option.

-

Annuity payments are taxed differently based on annuitization status, with no 10% penalty post-annuitization.

Annuities are complex financial products with tax implications and various options for investors seeking to manage retirement income and risk.