Transferring Losses

The concept of risk is why insurance exists. In a good year, an insured person may have no medical expenses at all. But if they’re hit by a bus, medical bills could easily exceed $500,000. You can’t eliminate risk from life, even at extraordinary expense.

For example, the only way to eliminate auto-related injuries is to eliminate automobiles. So an effective response to risk usually combines two elements:

- Efforts to reduce the risk

- Insurance to cover the risk that remains

In exchange for a premium, the insurer will pay a claim if a specified contingency occurs, such as death or medical bills. The insurer can offer this protection against financial loss by pooling the risks of a large group of similarly situated individuals (called exposure units). With a large pool, the laws of probability indicate that only a small fraction of the insured population will die or be hospitalized in a given year.

For example, if each of 100,000 individuals independently faces a 0.5% risk in a year, then on average 500 will have losses. If each of the 100,000 people paid a premium of $1,000, the insurance company would collect a total of $100 million - enough to pay $200,000 to each person who had a loss (assuming 500 people had a loss).

Insurance works through the statistical concept of the Law of Large Numbers. This law says that when a large number of people face a low-probability event, the actual proportion experiencing the event tends to be close to the mathematical probability. For instance, with a pool of 100,000 people who each face a 0.5% risk, the Law of Large Numbers indicates that 500 people or more will have losses during the same period only 1 time in 1,000.

Insurance is a business. However, it’s only a viable business for companies that can maintain financial strength while paying out claims. Insurance helps you manage risk by protecting you from events that would significantly affect your financial future. At the same time, the Law of Large Numbers helps insurers by making the number of claims they’ll pay from year to year reasonably predictable.

When you flip a coin, the probability it will land on heads is 50%, and the probability it will land on tails is 50%. Now suppose you flip a coin 10 times and it lands on heads 9 times. Does that mean the calculated probability was wrong?

No. In a small sample, such as 10 coin tosses, actual results can vary a lot from predicted results. But if you flipped the coin 10 million times (a very large sample), the calculated probability of 50% heads and 50% tails would be extremely accurate.

Although being able to predict future losses with some degree of accuracy is critical to insurance, certain types of perils are less predictable. When these perils cause losses, they may not create a stable pattern that can be used to estimate future losses. In a hurricane, airplane crash, or epidemic, many people may suffer losses at the same time.

Insurance companies manage these risks by spreading them:

- Across individuals

- Across time (good years and bad years), by building reserves in good years to handle heavier claims in bad years

- Across lines of insurance (for example, selling health insurance as well as homeowners insurance)

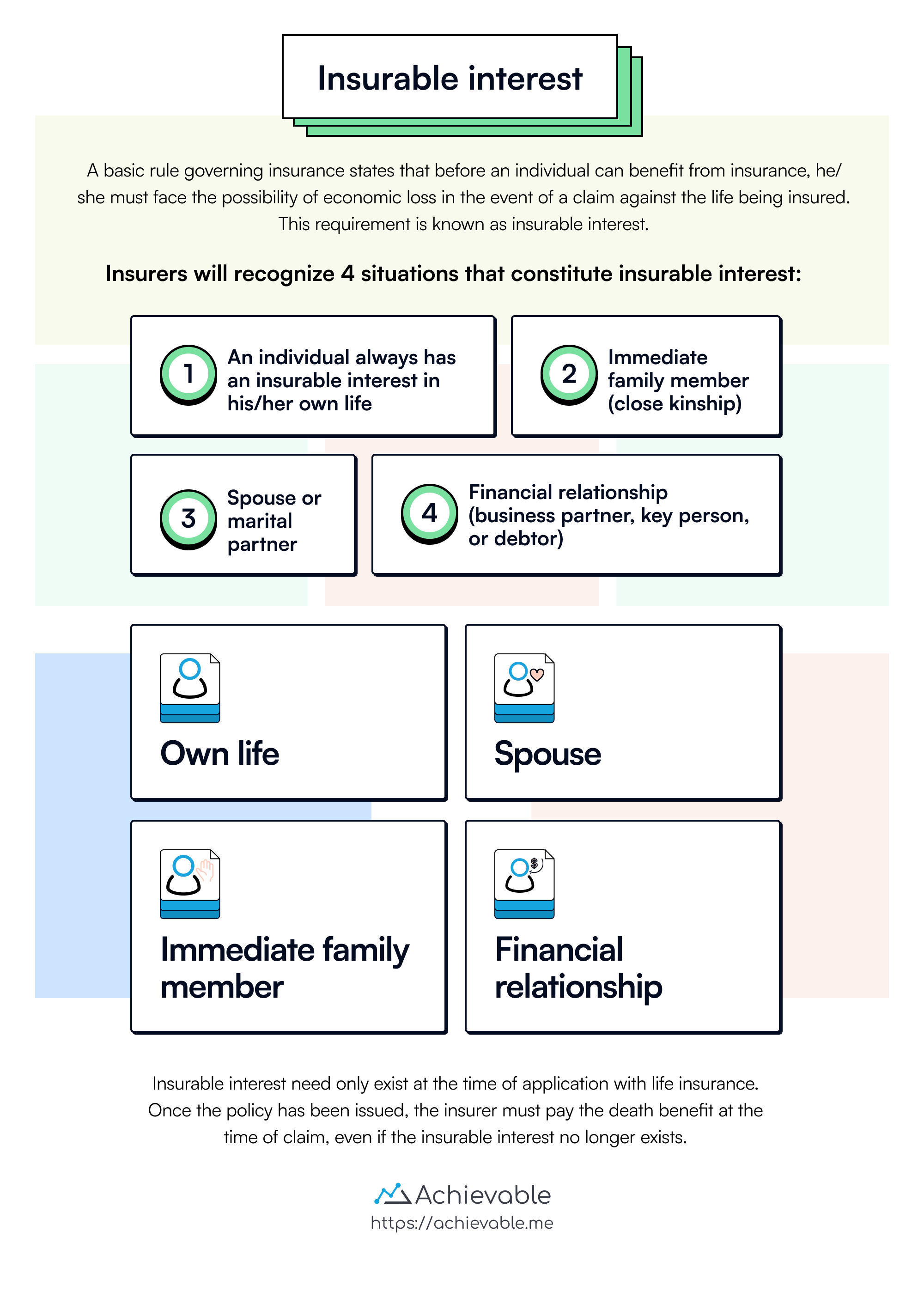

Another basic rule governing insurance is that before an individual can benefit from insurance, they must face the possibility of economic loss if a claim occurs against the life or property being insured. This requirement is known as insurable interest.

Insurers recognize several common situations in which insurable interest exists:

-

Own life - A person always has an insurable interest in their own life.

-

Spouse or marital partner - Marriage or legal partnership establishes insurable interest.

-

Immediate family members - This includes close blood relatives such as parents, children, or siblings.

-

Financial relationships - Insurable interest also exists when there is a financial stake in the continued life of another, such as a business partner, key employee, or debtor.

Important: For life insurance, insurable interest must exist at the time of application. It does not need to exist at the time of the claim.

Certain risks can’t be transferred through insurance. Insurable risks have characteristics that make the rate of loss fairly predictable, allowing insurers to prepare for the losses that do occur. For a risk to be acceptable to a conventional insurance company, it must meet the following criteria:

1) Loss must be uncertain

The purpose of insurance is to offset the financial loss of a covered event. The need for insurance comes from not knowing what will happen to a particular exposure unit. If a future loss is certain, it isn’t insurable.

With life insurance, the uncertainty isn’t whether an individual will die. Instead, it’s when the individual will die and what financial obligations will be left behind when death occurs.

2) Large number of exposure units

Insurance companies can’t predict who will die and when. But by using data from a large number of people, they can predict with reasonable accuracy how many people in a given population are likely to die during a certain period of time. The larger the group, the more accurately the insurer can predict losses for the group.

This is why the Law of Large Numbers helps insurance companies set appropriate premium charges so they can maintain financial strength while paying out claims.

3) Loss must pose an economic hardship

If the potential loss doesn’t justify the premium and the insurer’s underwriting expenses, the risk isn’t insurable.

4) Loss must be ascertainable

With life insurance, monetary value is placed on the insured’s ability to earn an income or on the needs of the insured’s survivors. With health insurance, economic loss is measured by lost wages or by actual medical expenses incurred.

Perils and hazards

Perils and hazards are related to the concept of risk.

- A peril is the specific cause of a loss. It’s the event being insured against. With life insurance, the peril being insured against is death.

- A hazard is a condition or factor that promotes the peril. Hang gliding, for example, is a hazard that promotes the peril of death.

When a person applies for life or health insurance, the insurer considers the hazards the applicant may encounter and how those hazards relate to the peril being insured against. There are 3 types of hazards that insurers are concerned about:

- Physical

- Moral

- Morale

Physical hazards include factors such as a person’s weight, medical history, and occupation. A moral hazard involves dishonesty - for example, an applicant who lies about their medical history, occupation, or hobbies. Morale hazards are more subjective and include behaviors such as road rage, or a tendency to drink alcohol to excess or use drugs, which can increase the risk of health problems or premature death.

Indifference is also a morale hazard. For example, not locking a car because insurance will cover theft reflects a casual or careless attitude that increases risk.

Lesson summary

Insurance operates by pooling funds from many individuals facing similar risks to cover financial losses from specific events through contractual agreements. Key concepts in insurance are:

-

The Law of Large Numbers forms the statistical basis for insurance operations by enabling companies to predict claims with reasonable accuracy by pooling risks across a large group.

-

Insurable interest is needed for a person to benefit from insurance, with requirements including having a financial stake in the insured event.

-

Perils are the causes of losses, while hazards are factors promoting these losses, with insurers considering physical, moral, and morale hazards in assessing risks.

While insurance is essential for managing risks, insurance companies rely on statistical principles and pooling of risks to maintain financial viability while ensuring that covered individuals can recover from unforeseen events without incurring significant economic losses.