Medigap and Medicaid

Medicare supplement (Medigap) policies

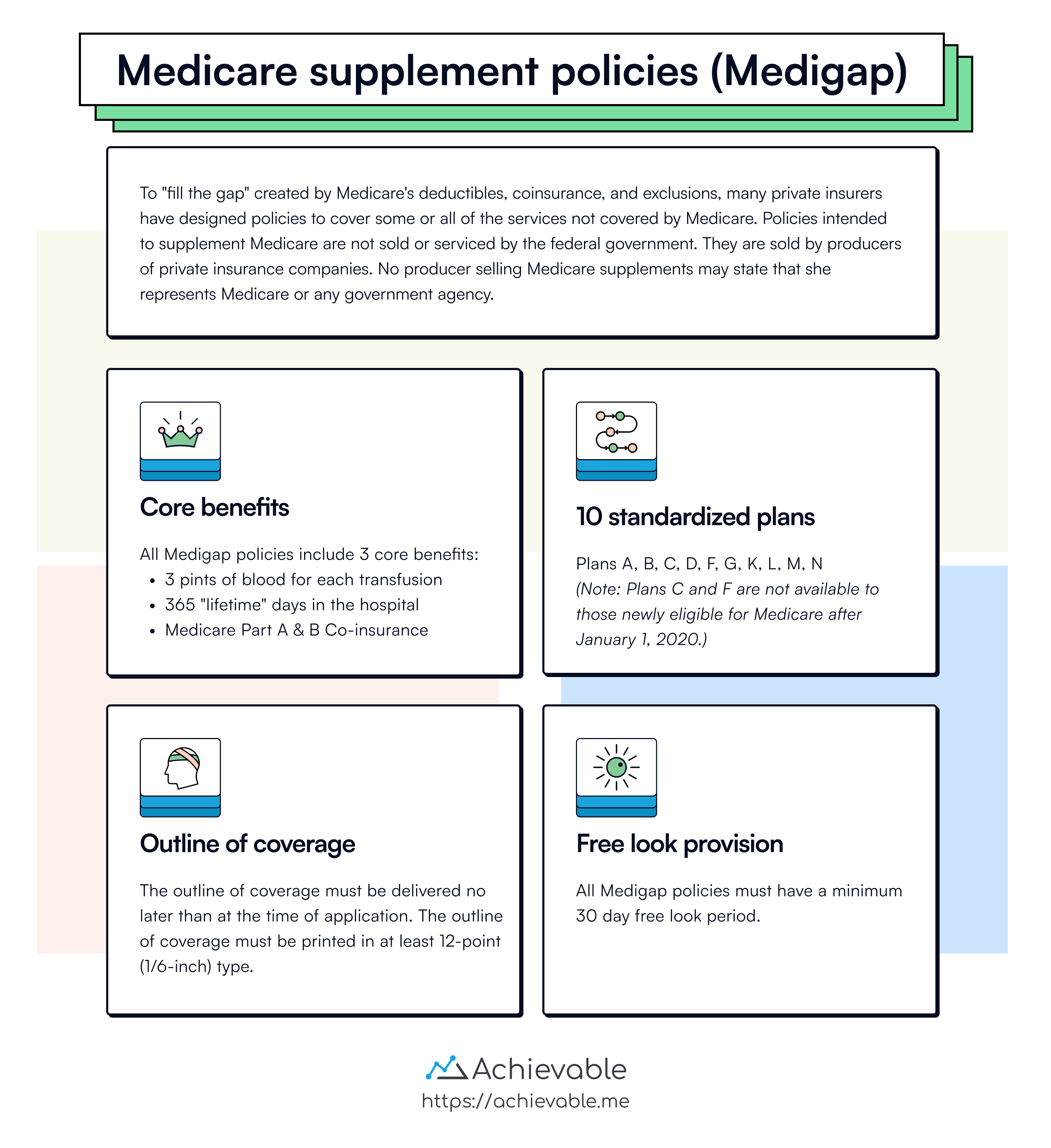

Medicare has deductibles, coinsurance, and exclusions. To “fill the gap” these costs create, many private insurers offer Medicare supplement (Medigap) policies that cover some or all services not covered by Medicare.

Medigap policies are not sold or serviced by the federal government. They’re sold by producers representing private insurance companies. No producer selling Medicare supplements may state that they represent Medicare or any government agency.

To reduce confusion from the many types of Medicare supplement policies, federal law requires national standardization of Medigap policies. Insurers may offer only standardized Medigap plans developed by the National Association of Insurance Commissioners (NAIC). Currently, there are 10 standardized plans (A, B, C, D, F, G, K, L, M, N). Each plan offers a different combination of benefits.

Plan A provides “core” benefits:

- Parts A and B co-payments

- 365 additional days of hospitalization

- The first 3 pints of blood

Plans C and F are not available to individuals newly eligible for Medicare on or after January 1, 2020.

No Medicare supplement policy may be sold unless a Buyer’s Guide and an Outline of Coverage are delivered at the time of application, before accepting any premium payment. If the policy is sold by direct response (correspondence or television), with no producer involved, the Buyer’s Guide and Outline of Coverage must be delivered no later than when the policy is delivered. The Outline of Coverage must be printed in at least 12-point (1/6-inch) type.

If the producer is replacing one Medicare supplement with another, the producer must also give the applicant a Notice Regarding Replacement of Health Insurance before delivering the policy. In addition, a producer may not sell a Medicare Supplement to anyone who already has a policy if the new policy duplicates coverage of the first one. If a Medicare Supplement policy replaces another Medicare Supplement policy that has been in force for at least 6 months, the new policy must waive any probationary or pre-existing condition clauses.

All Medigap policies must be guaranteed renewable. While “non-cancellable” is a term used in other types of health insurance, it does not apply to Medicare supplement (Medigap) policies. The law requires that every Medigap policy clearly state its renewability or continuation provisions on the first page of the contract. In addition, all Medicare supplement policies must include a minimum 30-day free look period.

Federal law establishes a 6-month open enrollment period for buying Medigap coverage from private insurers. For the 6 months immediately following enrollment in Medicare Part B, people age 65 or older cannot be denied a Medigap policy because of health problems. However, the company selling the Medicare supplement policy may apply a pre-existing condition clause and probationary period for the first 6 months of the new policy.

A Medicare supplement health insurance product called Medicare SELECT is an established type of Medigap plan available in some states. Medicare SELECT, which may be offered by insurance companies or HMOs, is the same as standard Medigap insurance in nearly all aspects. If you buy a Medicare SELECT policy, you are buying one of the standardized Medigap plans.

The key difference is network use. Medicare SELECT policies will only pay or provide full benefits if covered services are obtained through specified health care professionals and facilities. Because of this, Medicare SELECT policies generally have lower premiums.

State government programs

Medicaid

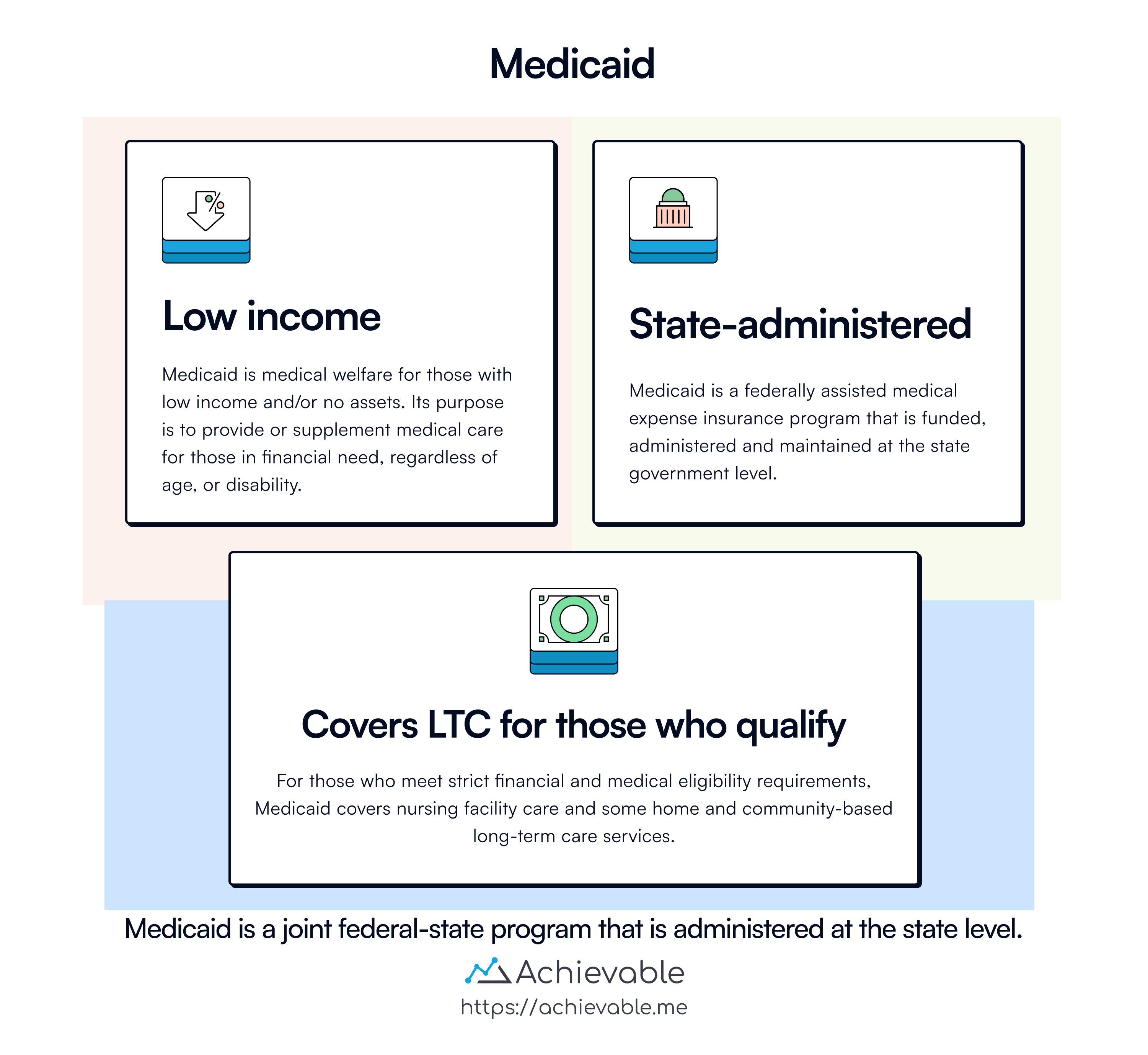

Medicaid is medical welfare for people with low income and/or few assets. It’s a federally assisted health insurance program that is administered at the state government level. Its purpose is to provide or supplement medical care for people in financial need, regardless of age or disability. The coverage provided is quite extensive and generally covers all normal medical needs. Medicaid is not part of the Social Security system.

Workers’ compensation

Workers’ comp is a liability policy. You can’t sell it with a life or health insurance license; you need a P&C license. Even so, it appears on this exam.

Workers’ compensation is mandated by state law for all employers. If an employer has one or more employees, they must be covered. The business owner, however, may opt out of coverage.

Based on the concept of liability without fault, these laws hold the employer liable for injury or illness that “arises out of and in the course of employment.” Benefits for medical expenses are automatically available in all states, but benefits for loss of income and/or loss of limb vary by state.

Most health insurance policies are non-occupational, meaning they cover you only off the job. If a health policy does not exclude on-the-job injuries, it may be described as having occupational coverage - but this is unusual, since workers’ compensation is designed to cover job-related risks.

Lesson summary

Medicare supplement (Medigap) policies are designed by private insurers to cover services not included in Medicare. Here are some key points about Medigap policies:

- Private insurers, not the federal government, sell and service Medigap policies.

- Federal law mandates national standardization of Medigap policies, with insurers offering no more than 10 standardized plans (A, B, C, D, F, G, K, L, M, N).

- Each plan offers a different combination of benefits, and Plans C and F are not available to new Medicare enrollees after January 1, 2020.

- A buyer’s guide and an outline of coverage must be provided at the time of application.

- Replacement of a Medigap policy must adhere to specific notice requirements.

- Medigap policies must be guaranteed renewable and include a minimum 30-day free look period.

Medicare SELECT is a Medigap insurance option with specific requirements for receiving full benefits.

Medicaid is a medical welfare program at the state level for individuals with low income and/or no assets. Some key features of Medicaid include:

- Coverage is comprehensive and extends to all normal medical needs.

- Medicaid is not part of the Social Security system.

- Medicaid covers nursing home and some home-based long-term care services for those who qualify.

Workers’ compensation is a liability policy mandated by state law for employers. Here are some important points about workers’ compensation:

- Employers must have coverage for employees, but business owners may choose to opt out.

- Workers’ comp is based on holding the employer liable for work-related injuries or illnesses.

- Health insurance generally does not cover on-the-job injuries if covered by Workers’ comp.

- Workers’ comp policies are sold by private commercial insurers, not government programs.