Insurance Contracts

Essential elements of an insurance contract

An insurance contract is fundamentally based on the utmost good faith of all parties. The applicant relies on the insurer’s promise to pay. The insurer relies on the truthfulness of the statements the applicant makes on the application.

Insurance is also governed by the law of contract. For any contract to be valid and enforceable, four conditions must be met:

- There must be consideration by both parties.

- An offer must be made by one party and acceptance of that offer made by the other party.

- All parties to the contract must be legally capable of entering into a contract.

- The purpose of the contract must be legal.

Consideration

For a contract to be valid, each party must give something of value.

- The insurer’s consideration is its promise to pay policy benefits if the insured suffers a covered loss (acceptance of the risk).

- The applicant’s consideration is the premium.

Premiums are often calculated on an annualized basis, even when the insured pays in other modes (monthly, quarterly, semiannual). Statutory reserves are maintained to meet future claim obligations.

Offer and acceptance

The offer made by one party must be accepted by the other on an unconditional basis.

- The applicant makes the offer by completing an application.

- The insurer may accept the application as written, or it may make a counteroffer (for example, by proposing a rated policy).

A contract forms only when both parties agree to the final terms. If they don’t agree, there is no contract.

Legal capacity

Both parties must be legally capable of entering into a contract.

- If the insurer is admitted or authorized in the state, it has legal capacity.

- The applicant has legal capacity unless he/she is a minor, mentally incompetent, intoxicated, or under the influence of narcotics.

Certain individuals, such as enemy aliens or others restricted by law, may also lack capacity in specific jurisdictions.

Legal purpose

A valid contract must be for a legal purpose and not against public policy. A life insurance policy purchased with the intent to have the insured killed is an obvious example of an invalid contract.

For an insurance contract to be valid, there must be an insurable interest between the applicant/owner and the insured.

- For life insurance, insurable interest must exist at policy inception.

- For property and casualty insurance, it must exist at the time of loss.

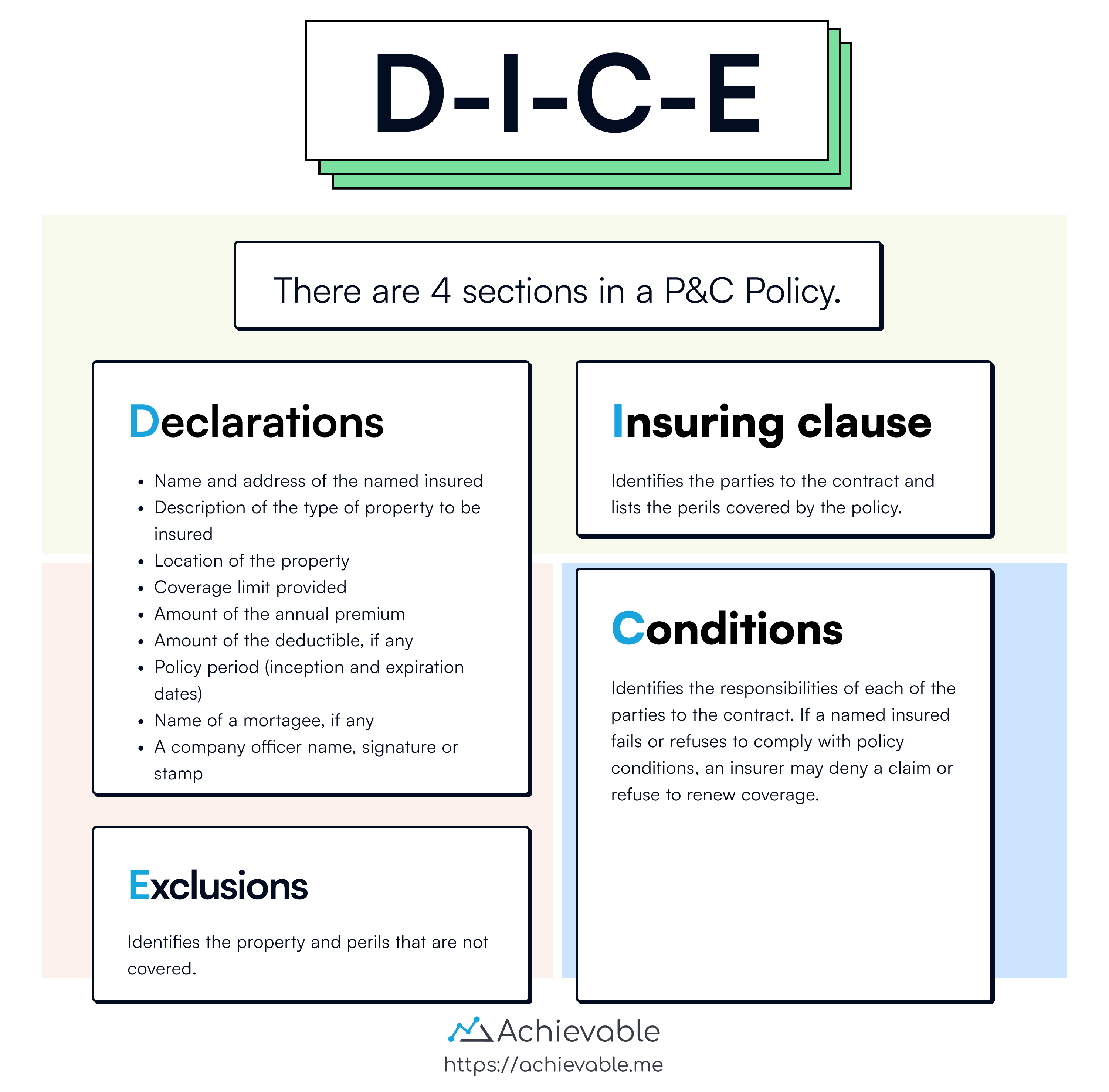

A property and casualty insurance policy is comprised of four basic sections of coverage including:

-

Declarations

-

Insuring agreement

-

Conditions

-

Exclusions

Declarations

The declarations page provides information about the property or exposures being insured. Much of the information in the declarations section is taken directly from the application and include, but are not limited to:

-

Name and address of the named insured

-

A description of the type of property to be insured

-

The location of the property

-

The coverage limit provided

-

The amount of the annual premium

-

Amount of the deductible, if any

-

The policy period (inception and expiration dates)

-

The name of a mortgagee, if any

-

A company officer name, signature or stamp

Insuring clause

This section summarizes the coverage (the agreement) between the named insured and the insurer. More specifically, it identifies the parties to the contract and lists the perils covered by the policy.

Conditions

This section identifies the responsibilities of each party to the contract. If a named insured fails or refuses to comply with policy conditions, an insurer may deny a claim or refuse to renew coverage.

Most policy conditions are placed on the named insured. For example, if a risk is altered or increased (i.e. installing a swimming pool after the policy became effective), the insured is required to notify the insurer.

Exclusions

This section identifies the property and perils that are not covered. Exclusions allow or permit an insurer to protect itself from financial disaster by not providing coverage for catastrophic losses.

Insurance contracts are unique in that the applicant must purchase the policy as written, without any opportunity to modify or clarify the contract language. Over time, courts have used the Doctrine of Adhesion to interpret ambiguous contract terms or conditions in favor of the insured, since the insured had no chance to alter the contract at the time of application.

Insurers go to great lengths to ensure that their contract language is clear and to avoid misunderstandings about the policy’s terms. Still, questions and conflicts do arise, and when they do, they often involve the concepts of warranties and representations.

A warranty is a statement or promise incorporated into the policy that must be true as stated or performed as promised. Under modern insurance law, a breach must be material to affect coverage.

Representations are statements made on the application that are substantially true to the best of the applicant’s knowledge.

If a statement is made on an application that the applicant knows is false, it is a misrepresentation and may constitute fraud. If the insurer can prove that the misrepresentation was made intentionally, it may void the contract and may be punishable as a Class 6 felony.

Lesson summary

An insurance contract is based on utmost good faith: the applicant relies on the insurer’s promise to pay, and the insurer relies on the truthfulness of the applicant’s statements.

To be valid and enforceable, a contract must include:

- consideration by both parties

- offer and acceptance

- legal capacity of the parties

- a legal purpose

Consideration is the exchange of promises:

- The insurer promises benefits for covered losses.

- The applicant pays the premium.

Offer and acceptance require an unconditional agreement. The applicant offers by completing an application, which the insurer can accept as written or change through a counteroffer.

Legal capacity means both parties must be able to enter into a contract. The contract’s purpose must also be legal and not against public policy. A valid insurance contract must establish an insurable interest.

-

Insurance contracts have unique features:

-

Applicants must accept policies as written without modification.

-

The Doctrine of Adhesion favors insured parties in case of ambiguous terms.

Insurers strive for clear contract language to prevent misunderstandings.

A property and casualty insurance policy consists of four parts:

- Declarations: Information about the insured property

- Insuring Clause: Summary of coverage and perils covered

- Conditions: Responsibilities of each party

- Exclusions: Identifies what is not covered

Warranties are promises that must be true as stated; representations are statements believed to be true to the best of the applicant’s knowledge.

Misrepresentations, if intentional, can void the contract and may constitute fraud.