Crime and Professional Liability

Commercial Crime Insurance

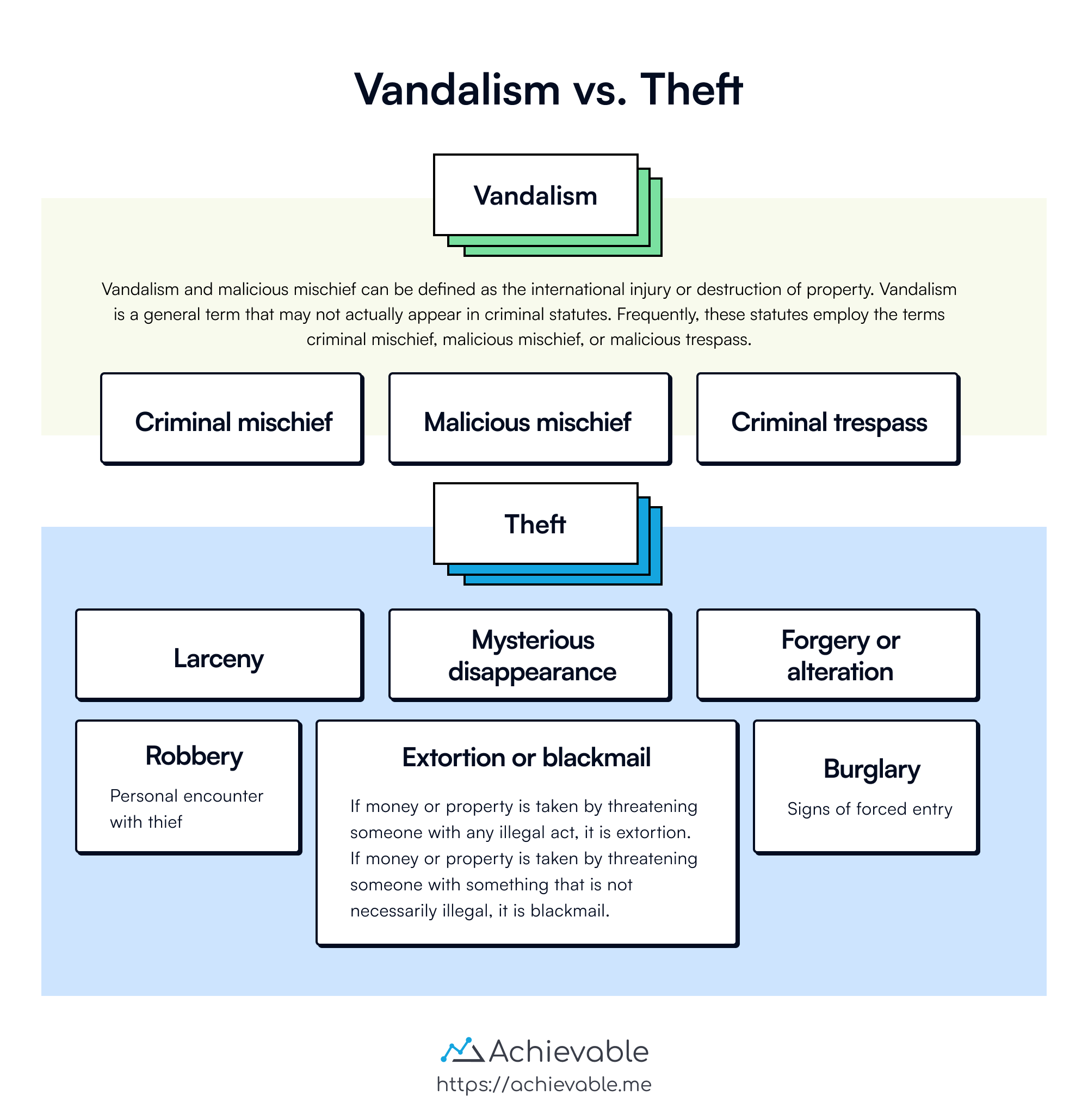

Crime policies use standard definitions to describe the types of crime a policy may cover. You’ll see these definitions in both personal and commercial insurance contracts. Some of the most common definitions include:

Theft

- Theft is a broad term for taking property without the owner’s consent. It’s an umbrella term that includes many dishonest acts involving property.

Burglary

- Burglary is a type of theft involving the illegal taking of property with no person-to-person encounter. To qualify as burglary, there must be visible signs of forcible entry. Burglary often occurs when a business is closed.

Robbery

- Robbery is theft committed by using force or the threat of force. Unlike burglary, robbery involves a face-to-face encounter between the robber and the victim.

Extortion

- Extortion is obtaining money or property through threats or coercion. Blackmail is a form of extortion that typically involves threats to reveal information.

Mysterious Disappearance

- Property is missing, but neither the owner nor the insurer can determine what happened. Coverage for mysterious disappearance may be available, but it’s commonly excluded under policies that protect against theft.

Custodian

- A custodian is the insured or an employee who has care and custody of insured property while inside the premises. A custodian does not include a watchperson or janitor.

Messenger

- A messenger is a person who has custody of insured property while outside the covered area.

Commercial crime insurance typically includes:

- A commercial crime declarations page

- A crime general provisions section (which includes definitions like those listed above)

- A crime coverage form

There are fourteen crime coverage forms, identified as Forms A through N. The five most commonly used forms are A, B, C, D, and E.

Form A

Employee Dishonesty

This form protects an employer against fraudulent acts committed by employees. It covers loss of the insured’s property, including money and securities.

There are three formats for employee dishonesty coverage:

- Name Schedule. Only covers individuals named in the Declarations. If a named employee leaves, the insurer must be notified so the former employee can be removed and the new employee added.

- Position Schedule. Covers whoever holds the listed position. You don’t need to notify the insurer when an employee leaves and a replacement is hired.

- Blanket Coverage. Covers loss caused by any employee. Under blanket coverage, the employer must establish a reasonable case that the employee(s) caused the loss.

Form B

Forgery or Alteration

This form protects the insured for loss caused by forgery or alteration of financial documents. It does not cover employee dishonesty.

Form C

Theft, Disappearance, and Destruction

This form may be added to the commercial crime coverage part to provide open-peril coverage for loss of money and securities.

There are two sections of coverage under this form:

- Coverage A protects against loss of money and securities inside the premises.

- Coverage B protects against loss of money and securities while being transported by the insured or an employee outside or away from the premises.

Form D

Robbery and Safe Burglary

This form covers property other than money and securities. It’s generally written to protect the insured against three exposures:

- On premises robbery

- Off premises robbery

- Safe burglary

This form covers robbery inside or outside the insured premises. It also covers burglary of a safe, including damage done to the safe by burglars.

Form E

Premises Burglary

This form covers loss of merchandise, furniture, fixtures, and equipment within the covered premises as a result of burglary. It also covers damage to the premises and to windows caused by burglars.

Premises burglary coverage applies to theft of covered property from inside the insured premises. It also applies if property is taken from a guard who is inside the premises at the time of the loss. Money and securities are not covered under this form.

The Discovery Condition

Burglary and robbery losses are often discovered right away. Other crime losses - such as extortion and embezzlement - may not be discovered until weeks, months, or even years after they occur.

The Discovery Clause in the Loss Sustained Form states that losses that occur during the policy period, but are not discovered for up to one year after the policy expires, can still be covered under the expired policy.

Other Coverage Forms Available

Additional coverage forms may be attached to the commercial crime coverage part, including:

- Computer fraud

- Safe depository liability

- Lessees of safe deposit boxes

- Liability for guest’s property

- Premises theft or robbery occurring on the insured’s premises or at certain designated locations outside the building

Professional Liability

Professional liability insurance is a specialized type of liability coverage for individuals such as physicians, attorneys, certified public accountants, insurance producers, or directors or officers of corporations.

Professional liability refers to liability arising from a failure to use care (negligence) at the level of skill expected from the professional.

Several forms of professional liability insurance are common.

Malpractice

Medical malpractice insurance is available to physicians, surgeons, dentists, and hospitals. It protects against legal action brought by an injured third party due to the insured’s negligence in performing professional duties.

Coverage applies to the insured’s responsibility for bodily injury or property damage to others. Many policies also cover personal injury, such as mental anguish suffered by the injured third party due to the insured’s negligence or non-performance.

Many malpractice policies include a “consent to settle” clause. This requires the insurer to obtain the insured’s permission before settling a claim, which helps protect the professional’s reputation.

Errors and Omissions

Many professions use errors and omissions (E&O) policies. Examples include accountants, insurance producers or adjusters, architects, attorneys, stockbrokers, real estate brokers, and engineers.

Coverage is tailored to the profession. It pays for liability arising out of the performance of professional duties when the insured is alleged to have been negligent.

For example, if an insurance agent makes an inadequate recommendation that causes a customer financial harm, a resulting lawsuit will likely be covered by the agent’s E&O policy.

Directors and Officers

Another type of professional liability contract provides legal liability protection to a corporate director or officer for errors and/or omissions. This type of policy protects corporate leadership from lawsuits by stockholders or others alleging mismanagement.

Other profession-specific policies are also available, including:

- Druggists Liability

- Fiduciary Liability

- Employee Benefit Plan Liability

- Professional Architects Liability

Lesson Summary

Commercial Crime Insurance includes various definitions and coverage forms:

- Theft - a broad term for taking property without consent

- Burglary - theft with no person-to-person encounter

- Robbery - theft involving a person-to-person encounter

- Extortion - taking property by threatening with an illegal act

- Mysterious Disappearance - unexplained loss of property

- Custodian and Messenger definitions

There are 14 crime coverage forms; the most commonly used are:

- Form A - Employee Dishonesty

- Form B - Forgery or Alteration

- Form C - Theft, Disappearance, and Destruction

- Form D - Robbery and Safe Burglary

- Form E - Premises Burglary

Commercial Crime Insurance covers discovery of losses and additional coverage forms like Computer fraud, Safe depository liability, and more.

Professional Liability Insurance includes forms for Malpractice, Errors and Omissions, and Directors and Officers coverage tailored to different professions.

- Malpractice - for physicians, surgeons, dentists, etc.

- Errors and Omissions - for various professions

- Directors and Officers - for legal liability protection