Collars

A collar (sometimes called a hedge wrapper) combines two strategies you’ve already seen: hedging and income strategies. In practice, it’s a long stock position protected by a long put, with the put’s cost often offset by selling a covered call.

A collar, in specific terms, is:

- Short call (“out of the money”)

- Long stock

- Long put (“out of the money”)

The key position in a collar is the long stock. The stock is the “dominant” part of the strategy: the stock’s market price drives the overall result and determines whether either option will be exercised.

Let’s look at an example:

Short 1 ABC Jan 45 call @ $3

Long 100 shares of ABC stock @ $40

Long 1 ABC Jan 35 put @ $3

The long put is the hedge (protection) for the long stock, even though it starts “out of the money.” If the market price falls below $35, the investor can exercise the put and sell the shares at $35. That protection isn’t free: the put costs $3 per share, or $300 total.

In this example, the put’s $300 cost is offset by the $300 premium received from selling the call. That’s why collars are sometimes described as “free” (or cheap) insurance.

The call premium comes with a trade-off. A short call creates an obligation: if assigned, the investor must sell the stock at the call’s strike price.

- If the market price rises above $45, the short call becomes “in the money” and will be assigned.

- No matter how high the stock goes, the investor’s best possible sale price is $45.

So, the investor is effectively using the $300 call premium to pay for the $300 put hedge, but that also places a ceiling on the stock’s upside (an obligation to sell at $45).

This is an example of a “cashless” collar: the cost of the long put is completely offset by the premium received from the short call. When the collar (long put + short call) is established for no net cost, it’s considered “cashless.”

Let’s work through a few examples to see how collars behave at different stock prices.

An investor buys 100 shares of ABC stock at $40, goes short 1 ABC Jan 45 call at $3, and long 1 ABC Jan 35 put at $3 when the market price is $40. What is the gain or loss if the market rises to $75?

Answer = $500 gain

| Action | Result |

|---|---|

| Buy shares | -$4,000 |

| Sell call | +$300 |

| Buy put | -$300 |

| Call assigned - sell shares | +$4,500 |

| Total | +$500 |

At $75, the call is “in the money” (“call up”) and the put is “out of the money” (“put down”). The put expires worthless, but the call is assigned, forcing the ABC shares to be sold at $45.

- Stock gain: buy at $40, sell at $45 = $5 per share = $500

- Option premiums: +$300 (call) and -$300 (put) offset to $0

So the overall profit is $500.

The investor reaches the maximum gain once the market rises to $45 or higher. Because of the short call, the best possible sale price is $45. Whether the stock goes to $45 or $45,000, the gain stays locked at $5 per share.

This also highlights the strategy’s trade-off. Without the options, the stock would have gained $35 per share (buy at $40, sell at $75), or $3,500 overall. If the investor had bought the put but not sold the call, the result would have been $32 per share ($35 stock gain minus $3 put premium), or $3,200 overall.

The short call limits upside. Gains above $45 are given up, which is an example of opportunity cost (introduced in the income strategies section).

What if the market rises by a small amount?

An investor buys 100 shares of ABC stock at $40, goes short 1 ABC Jan 45 call at $3, and long 1 ABC Jan 35 put at $3 when the market price is $40. What is the gain or loss if the market rises to $42?

Answer = $200 gain

| Action | Result |

|---|---|

| Buy shares | -$4,000 |

| Sell call | +$300 |

| Buy put | -$300 |

| Share value | +$4,200 |

| Total | +$200 |

At $42, both the short call and long put are “out of the money,” so both expire worthless.

- Stock gain: buy at $40, worth $42 = $2 per share = $200

- Option premiums offset to $0

When the market is between $35 and $45, both options are out of the money and expire worthless. With the premiums offsetting each other, the overall gain or loss comes entirely from the stock.

What happens if the market is flat?

An investor buys 100 shares of ABC stock at $40, goes short 1 ABC Jan 45 call at $3, and long 1 ABC Jan 35 put at $3 when the market price is $40. What is the gain or loss if the market stays at $40?

Answer = $0 (breakeven)

| Action | Result |

|---|---|

| Buy shares | -$4,000 |

| Sell call | +$300 |

| Buy put | -$300 |

| Sell value | +$4,000 |

| Total | $0 |

At $40, both options are “out of the money” and expire worthless. The shares are worth what the investor paid, so there’s no stock gain or loss. With the option premiums offsetting, the overall result is breakeven.

Again, when the market is between $35 and $45, both options expire worthless and the result is driven by the stock.

What happens if the market falls by a small amount?

An investor buys 100 shares of ABC stock at $40, goes short 1 ABC Jan 45 call at $3, and long 1 ABC Jan 35 put at $3 when the market price is $40. What is the gain or loss if the market falls to $37?

Answer = $300 loss

| Action | Result |

|---|---|

| Buy shares | -$4,000 |

| Sell call | +$300 |

| Buy put | -$300 |

| Sell value | +$3,700 |

| Total | -$300 |

At $37, both options are still “out of the money” and expire worthless.

- Stock loss: buy at $40, worth $37 = $3 per share = $300

- Option premiums offset to $0

So the overall result is a $300 loss.

As long as the stock stays between $35 and $45, both options expire worthless and the stock determines the outcome.

What happens if the market falls significantly?

An investor buys 100 shares of ABC stock at $40, goes short 1 ABC Jan 45 call at $3, and long 1 ABC Jan 35 put at $3 when the market price is $40. What is the gain or loss if the market falls to $10?

Answer = $500 loss

| Action | Result |

|---|---|

| Buy shares | -$4,000 |

| Sell call | +$300 |

| Buy put | -$300 |

| Exercise put - sell shares | +$3,500 |

| Total | -$500 |

At $10, the put is “in the money” (“put down”) and the call is “out of the money” (“call up”). The call expires worthless, but the investor exercises the put and sells the shares at $35.

- Stock loss: buy at $40, sell at $35 = $5 per share = $500

- Option premiums offset to $0

So the overall loss is $500.

This is where the collar’s protection shows up. If the investor only owned the stock, the loss would have been $30 per share (buy at $40, sell at $10), or $3,000 overall. The long put limits the downside, and the call premium helps pay for that hedge.

When the market price falls to or below the put’s strike price, the investor reaches the maximum loss for the strategy.

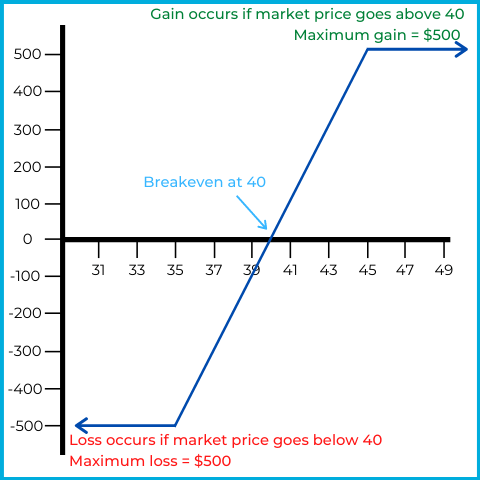

For visual learners, an options payoff chart can help you see the strategy’s “big picture.” Here’s the same position again:

Long 100 shares of ABC stock @ $40

Short 1 ABC Jan 45 call @ $3

Long 1 ABC Jan 35 put @ $3

Here’s the payoff chart:

The horizontal axis represents the market price of ABC stock, while the vertical axis represents overall gain or loss.

As the payoff chart shows:

- Between $35 and $45, gains and losses vary with the stock price, with breakeven at $40.

- Below $35, the loss is locked at $500, no matter how low the stock falls.

- Above $45, the gain is locked at $500, no matter how high the stock rises.

The last two examples show what happens when the investor closes the option contracts and sells the shares at the market price.

An investor buys 100 shares of ABC stock at $40, goes short 1 ABC Jan 45 call at $3, and long 1 ABC Jan 35 put at $3 when the market price is $40. The market price rises to $50, the contracts are closed at intrinsic value, and the shares are sold at the market price. What is the gain or loss?

Answer = $500 gain

| Action | Result |

|---|---|

| Buy shares | -$4,000 |

| Sell call | +$300 |

| Buy put | -$300 |

| Close call | -$500 |

| Close put | $0 |

| Sell shares | +$5,000 |

| Total | +$500 |

At $50, the call is in the money (has intrinsic value) - “call up.” The put is out of the money (no intrinsic value) - “put down.”

- Closing the call: buy to close at $5 intrinsic value

- Short call result: sold at $3, bought at $5 = $2 per share loss = $200 loss

- Closing the put: sell to close at $0 intrinsic value

- Long put result: bought at $3, sold at $0 = $3 per share loss = $300 loss

Total options result: $500 loss.

With the options closed, the stock is sold at the market price:

- Stock gain: buy at $40, sell at $50 = $10 per share = $1,000 gain

Combine them:

- $1,000 stock gain + $500 options loss = $500 overall gain

Let’s try one last example involving closing the option contracts and selling the shares:

An investor buys 100 shares of ABC stock at $40, writes 1 ABC Jan 45 call at $3, and holds 1 ABC Jan 35 put at $3 when the market price is $40. The market price falls to $36, the contracts are closed at intrinsic value, and the shares are sold at the market price. What is the gain or loss?

Answer = $400 loss

| Action | Result |

|---|---|

| Buy shares | -$4,000 |

| Sell call | +$300 |

| Buy put | -$300 |

| Close call | $0 |

| Close put | $0 |

| Sell shares | +$3,600 |

| Total | -$400 |

At $36, both options are out of the money and have no intrinsic value.

- Closing the call: buy to close at $0 intrinsic value

- Short call result: sold at $3, bought at $0 = $3 per share gain = $300 gain

- Closing the put: sell to close at $0 intrinsic value

- Long put result: bought at $3, sold at $0 = $3 per share loss = $300 loss

The gain on the call and loss on the put offset, so the options break even overall.

With the options closed, the stock is sold at the market price:

- Stock loss: buy at $40, sell at $36 = $4 per share loss = $400 loss

With the options netting to $0, the final result is a $400 loss.

To summarize, collars let investors reduce the cost of hedging a long stock position by using call premium to help pay for a protective put.

- If the market falls far enough, the put can be exercised, allowing the investor to sell shares at the put’s strike price (higher than the market).

- If the market rises far enough, the call can be assigned, forcing the investor to sell shares at the call’s strike price (lower than the market).

A simple way to remember the idea is the “dog collar” analogy. A dog on a collar and leash can’t move too far away. Similarly, a collar on a stock position keeps the outcome within a range: the stock can’t fall too far without the put protection kicking in, and it can’t rise too far without the call obligation limiting gains. In the examples above, the effective sale range is limited to $35-$45.