The IPO process

During an initial public offering (IPO), the issuer and underwriter must follow strict rules. Many of these requirements come from the Securities Act of 1933, which governs the primary market.

In the early 1900s, financial markets saw widespread fraud, deceit, and manipulation, and some of these practices contributed to the Great Depression. To protect investors, Congress passed the Securities Act of 1933. The law requires issuers to fully disclose key information about any securities they plan to sell to the public. Because the rules are detailed, issuers typically hire lawyers and accountants and rely heavily on their underwriter to help ensure compliance.

As we discussed previously, issuers hire underwriters to sell their securities to investors. The issuer and underwriter sign a contract that lays out:

- The fees paid by the issuer

- The liabilities (commitments)

- The general process for how the sale will occur

After the contract is signed, the underwriter guides the issuer through the due diligence phase. The Securities Act of 1933 requires the issuer to disclose a significant amount of information to the public. The issuer completes and files the SEC’s registration form, which requests items such as business history, information on officers and directors, and current financial status. Specific details in the registration form include the following:

- Use of proceeds

- Description of securities

- Risk factors

- Financial statements (e.g. balance sheet)

- Insiders (officers, directors, 10% shareholders)

The filing of the registration form begins the 20-day “cooling off” period. During this time, the SEC reviews the filing to confirm it is complete. This review takes time, which is why the period is set at 20 days.

The SEC’s goal is to make sure the public has access to the required disclosures before any sales activity occurs. As a result, the underwriter (and any other financial firm connected to the IPO) cannot:

- Advertise or recommend the new issue to customers

- Sell the new issue

- Take deposits for future sales

In other words, sales activity is off limits during this 20-day period.

Some activities are allowed during the cooling off period. The information in the SEC registration form is compiled into a document called the prospectus. Investors use the prospectus to learn about the issuer and the security. During the 20-day cooling off period, the SEC registration form is used to create a “preliminary” prospectus, which may be provided to potential investors on a solicited or unsolicited basis.

This preliminary prospectus is sometimes called the “red herring.” It remains preliminary until the SEC officially registers the security. The term ‘red herring’ comes from a message printed in red on the preliminary prospectus:

A Registration Statement relating to these securities has been filed with the Securities and Exchange Commission but has not yet become effective. Information contained herein is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted prior to the time the Registration Statement becomes effective.

In plain English, the preliminary prospectus may still change because the SEC review is not finished.

It’s also important to understand what the SEC does not do. The SEC does not verify the accuracy of the information and does not guarantee anything about the new issue. If the issuer misleads the public or lies in the registration form, the issuer (and any individuals involved) may face significant fines and sanctions. Jail time is also possible for anyone who knowingly provides false information.

The SEC’s job in this process is to determine whether the registration form is complete. If information is missing, the SEC sends a deficiency letter identifying what must be added or corrected. This pauses the registration process until the issuer submits the missing information and re-files.

Part of the underwriter’s job is to price the new security. This is especially challenging with stock, since its market value depends heavily on demand. To estimate demand for the IPO, the underwriter may solicit or receive indications of interest from potential investors during the 20-day cooling off period.

Indications are just indications and are not binding on either party:

- If a customer indicates interest, the customer is not obligated to buy.

- If the underwriter receives an indication of interest, the underwriter is not obligated to sell.

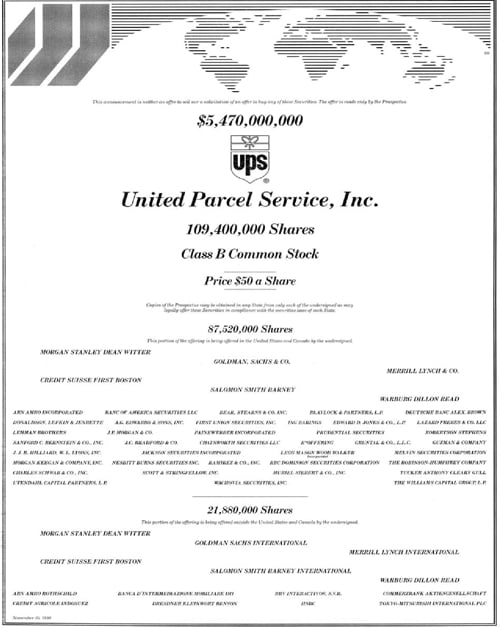

To notify the public of the new issue, a tombstone may be published. The term “tombstone” refers to the ad’s appearance (it resembles a tombstone).

Tombstones are typically published in newspapers and online outlets. They are the only form of advertising the SEC allows during the cooling off period. A tombstone is limited to factual information and cannot “pump up” or recommend the issue.

Typical tombstone information

- Name of issuer

- Type of security

- Number of shares or units to be sold

- Gross proceeds of the offering

- Name of lead underwriter

- Name of syndicate members

- Estimated public offering price

To summarize, here’s what can and cannot be done during the 20-day cooling off period.

Legal during 20-day cooling off period

-

Distribute the preliminary prospectus

-

Take indications of interest

-

Publish a tombstone

Illegal during 20-day cooling off period

-

Recommend the new issue

-

Advertise the new issue

-

Sell the new issue

-

Take a deposit for the new issue

After the SEC reviews a completed registration form, the security becomes effectively registered. At some point during the cooling off period, an effective date is announced. The effective date is the first day the security may be legally sold to the public.

Once the registration is effective, the underwriter contacts customers who submitted indications of interest. If demand is high, the underwriter must decide which customers receive shares. There are few formal guidelines here, so underwriters often allocate shares to their most profitable customers.

A FINRA rule requires underwriters to avoid selling common stock IPOs to industry insiders. The purpose is to help ensure the public has access to IPO shares. Without this rule, an underwriting syndicate could sell the issue to insiders and/or keep shares for itself, especially when demand is high.

FINRA member firms (financial firms), their employees, and their immediate family members are considered restricted persons and are prohibited from purchasing common stock IPOs. Immediate family members include parents, siblings, and children, plus anyone who is financially dependent on the industry insider. Some people use the “rule of 1” to remember the family members covered:

- “1 up” (parents)

- “1 down” (children)

- “1 over” (siblings and spouses)

In-laws are also included. For example, a father-in-law or sister-in-law of a registered representative would be prohibited from participating in a common stock IPO. This restriction applies only to common stock IPOs. It does not apply to IPOs of preferred stock, debt offerings, or other types of securities.

Professionals connected to the offering are also barred from purchasing common stock IPOs. This includes consultants of the underwriter (sometimes called finders) and professionals working for the issuer (accountants, lawyers, and other fiduciaries). Portfolio managers (e.g. mutual fund managers) are also barred from purchasing the IPO for their personal accounts. However, portfolio managers may purchase the IPO for the funds they manage. Finally, passive owners of broker-dealers are barred as well. A passive owner is not involved in day-to-day operations and is not a registered representative, but is still treated as an insider for purposes of this rule.

New issues are sold at the public offering price (POP). You probably remember this term from the Investment Companies chapter. Similar to an investor buying a mutual fund, IPO shares are purchased at the POP.

The Securities Act of 1933 requires the underwriting syndicate to deliver a prospectus to each customer buying the IPO. The prospectus contains the information filed in the registration statement, plus the POP. The prospectus must be delivered in its original, unaltered form. Firms cannot highlight, summarize, or modify a prospectus in any way.

Prospectus delivery requirements can also apply in the secondary market for a limited time after the IPO closes. A prospectus must be delivered by financial firms (like securities dealers and broker-dealers) for these time frames after the IPO is closed:

| Type of offering | Prospectus timeframe |

|---|---|

| Listed IPO | 25 days |

| Unlisted APO | 40 days |

| Unlisted IPO | 90 days |

| Listed APO | No requirement |

Listed securities are eligible to be traded on exchanges (e.g. the NYSE, while unlisted securities only trade in the OTC markets. APOs (additional public offerings), also known as follow-on offerings, occur when an issuer already has shares outstanding and plans to sell more shares.

The SEC maintains an “access equals delivery” rule, which allows a prospectus to be delivered electronically to investors. Issuers comply by posting prospectuses to the SEC’s Electronic Data Gathering, Analysis, and Retrieval system, better known as EDGAR. Investors can visit EDGAR to retrieve a prospectus. For example, here’s Instacart’s prospectus for the company’s 2023 IPO.

After a security is sold in the primary market, investors trade it in the secondary market. Some IPO customers hold shares long term, while others sell quickly to try to lock in a profit. We’ll cover the secondary market in the next chapter.