Suitability

Fixed income debt securities come in many shapes and forms. We’ve learned about corporate, US government, and municipal securities in this unit. Now, we’ll discuss the benefits, risks, and typical investors involved with these investments.

Benefits

The primary benefit of bonds is interest income. Most bonds pay interest semiannually, and those interest payments are a legal obligation of the issuer. Unlike stock dividends, interest payments don’t require approval by the Board of Directors (BOD). If an issuer misses an interest or principal payment, bondholders can take legal action, including forcing the issuer into bankruptcy. Because of this legal obligation, bond income is generally more predictable than stock dividends.

Capital appreciation can occur, especially if interest rates fall. However, interest rate movements are difficult to predict, and bonds mature at par. If you hold a bond to maturity, you’ll receive the face (par) value back at maturity. For that reason, most bond investors focus on income rather than price appreciation, unless the bond is convertible.

While it’s not always true, bond prices are often less volatile than stock prices. Since bond interest is a legal obligation and isn’t tied directly to a company’s profitability, price swings are typically smaller. There are important exceptions:

- If interest rates move sharply, bond prices can move sharply.

- If an issuer is close to bankruptcy, its bonds can become highly volatile.

Some benefits depend on the type of issuer:

- US Government securities are considered among the safest securities in the world, especially since the government can create its own currency to repay its debts.

- Municipal securities typically provide tax-free income if purchased by a resident.

- Corporate bonds offer a wide range of choices, from large, established companies to small start-ups.

Systematic risks

As a reminder, systematic risks affect a large portion of the overall market. For bonds, the two key systematic risks are interest rate risk and inflation (purchasing power) risk.

Earlier in this chapter, we discussed price volatility and duration, both of which relate to interest rate risk. Bonds with long maturities and low coupons tend to move the most in price when market conditions change. In practice, bond prices are most commonly influenced by changes in interest rates.

Interest rate risk (sometimes called market risk for bonds) is the risk that interest rates rise, causing bond market prices to fall. Prices fall because older bonds with lower coupons must become cheaper to compete with newly issued bonds offering higher interest rates. Interest rate risk applies to all fixed-income investments, including preferred stock.

We discussed inflation (purchasing power) risk in the preferred stock suitability chapter. This risk occurs when inflation reduces the real value of an investment’s cash flows. Bonds are especially exposed because their coupons are fixed: investors receive a fixed dollar amount of interest over the life of the bond. If the prices of goods and services rise, that fixed interest payment buys less.

When inflation rises, the Federal Reserve (the central bank of the US) often raises interest rates to reduce borrowing and slow demand, which can help stabilize prices. This is one reason purchasing power risk and interest rate risk are closely connected: when interest rates rise, bond market prices fall.

Just like interest rate risk, purchasing power risk generally increases as maturity increases. One common way to reduce inflation exposure is to use short-term bonds. When a short-term bond matures, you can reinvest the proceeds at then-current (potentially higher) interest rates instead of being locked into a lower rate for a long time.

Non-systematic risks

Non-systematic risks affect specific issuers or securities rather than the entire market. Bonds have several important non-systematic risks.

Default risk (also called credit risk or repayment risk) is the risk that an issuer can’t make required interest and/or principal payments. The most common cause of default is bankruptcy.

Bankruptcy isn’t common, but it does happen. Corporations and even governments can default (though government defaults are rare). For example, the city of Detroit declared bankruptcy and defaulted on its bonds in 2013. It was (and still is) the largest default by a municipal (local government) issuer in US history. If you held a Detroit bond at the time, you likely lost a substantial amount of money.

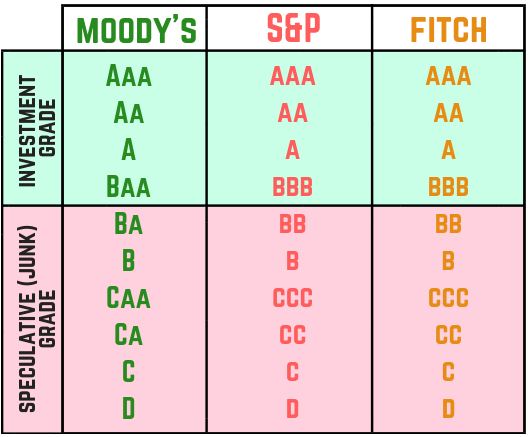

Rating agencies help investors evaluate default risk. Standard & Poors (S&P), Moody’s, and Fitch are the three rating agencies to know for the exam. Their rating symbols differ slightly, but each focuses on the issuer’s likelihood of default. Here’s how their ratings appear:

It’s important to distinguish between investment grade and speculative bonds:

- Investment grade bonds have little to no default risk. Investment grade bonds have ratings of BBB (Baa for Moody’s) or higher.

- Speculative bonds (also called junk bonds) have considerable default risk. The lower the rating, the higher the default risk. Speculative grade bonds have ratings of BB (Ba for Moody’s) or lower.

Liquidity risk (also called marketability risk) is the risk that a security can’t be sold quickly without a significant price concession. In general, the less desirable a bond is to other investors, the higher its liquidity risk. For example, if a company is close to bankruptcy, you may only be able to sell its bonds at a steep discount (or possibly not at all).

Some investments tend to have higher liquidity risk. Municipal bonds are known for liquidity risk, largely because of their tax status. Since residents may receive tax-free income, trading often concentrates among investors in the same area. The smaller the municipality, the fewer potential buyers. In contrast, US Government securities trade globally and are among the most liquid investments in the world.

Legislative risk is the risk that a new law or regulation (usually domestic) harms an investment. For example, the tariffs imposed by the Trump administration starting in 2018 increased the cost of doing business with certain foreign companies. Investors holding securities tied to international trade experienced legislative risk when markets responded negatively to the trade war.

Political risk is the risk that government instability or a sudden change in government harms an investment. For example, suppose you own a Ukrainian bond. If an unexpected military coup replaces the government, the bond could default. If the new government doesn’t plan to honor the old government’s debts, you could lose a significant amount of money.

Political instability can happen anywhere, but it’s generally considered a foreign risk. The United States has political disagreements, but it has a relatively stable political structure.

Reinvestment risk occurs when interest rates fall. You can think of it as the risk that future cash flows (interest payments, or returned principal) must be reinvested at lower rates. While it could be argued that reinvestment risk is systematic, it tends to matter most for bonds with high coupons, frequent interest payments, and callable bonds.

Even though bond prices typically rise when interest rates fall, reinvestment risk focuses on what happens to the cash you receive. Many long-term investors keep their money invested continuously. When a bond pays interest, that cash is often reinvested into new bonds (or more of the same bond). If interest rates have fallen, the reinvested money earns a lower return.

Earlier in this chapter, we reviewed callable bonds. Call risk is a type of reinvestment risk that occurs when a callable bond is likely to be called (or is called). Bonds are most likely to be called when interest rates fall, because issuers can refinance by issuing new bonds at lower rates.

Call risk is often considered the worst form of reinvestment risk. Instead of reinvesting only the interest payments at lower rates, you must reinvest both the interest and the principal returned when the bond is called. Since more money is being reinvested at the lower rate, the impact can be substantial.

The last risk to discuss relates to yield. We’ve already discussed the benefit of tax-free income from municipal bonds, but that benefit comes with a tradeoff: lower yields. Issuers can offer lower yields because investors don’t pay taxes on the interest. While it’s not the most severe risk, an investor in a low tax bracket should generally avoid municipal investments. Otherwise, they may face opportunity cost if other investments could provide a higher after-tax return.

Typical investor

There are many types of bonds, with different combinations of risks and benefits. Here, the goal is to describe the typical bond investor in general terms.

Compared with stocks, bonds are often preferred by older, more conservative investors. Because interest payments are a legal obligation of the issuer, bonds typically involve less risk than stocks, which usually means lower expected returns. Investors who want predictable income often choose debt securities over equity (stock) securities.

Remember the Rule of 100? As a general guideline, the older an investor is, the more they tend to allocate to fixed-income securities like bonds. Here’s the table from the suitability section of common stock:

| Age | Stock % | Bond % |

|---|---|---|

| 30 | 70% | 30% |

| 45 | 55% | 45% |

| 60 | 40% | 60% |

| 70 | 30% | 70% |

The Rule of 100 is often applied by matching an investor’s age to the percentage of bonds in the portfolio. This is a general guideline, not a rule that always fits. Some older investors can afford to take more risk (for example, an 80-year-old billionaire may choose a higher stock allocation). Some younger investors are more risk-averse and prefer more fixed income. Use the Rule of 100 as a starting point, and expect exceptions.

You’ll also see that some bonds carry significant risk. Junk bonds and other high-risk debt securities often offer higher yields, but investors can lose substantial amounts of money if a default occurs.

Interest income is the primary reason most investors buy bonds. If an investor isn’t seeking income, another asset class may be more appropriate. One exception is zero coupon bonds, which pay interest only at maturity. If an investor wants a predictable lump-sum payout years in the future and doesn’t need income along the way, a long-term zero coupon bond may be suitable.