Yield relationships

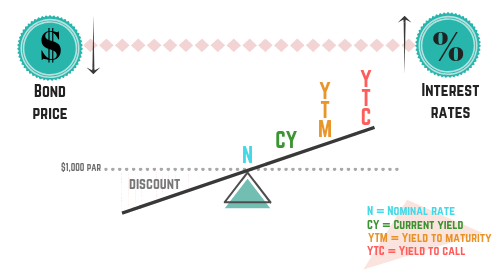

Discount bond yield relationships

Here’s a quick recap of the discount bond example from the previous sections.

A 10-year, $1,000 par, 4% bond is trading at $800. The bond is callable at par after 5 years.

-

Coupon = 4%

-

Current yield = 5%

-

YTM = 6.7%

-

YTC = 8.9%

This order isn’t random. For a discount bond, the yields follow a consistent pattern:

- The coupon is the lowest

- Then current yield

- Then yield to maturity (YTM)

- And yield to call (YTC) is the highest

You can calculate each yield, but on exams it’s often faster to use a common bond visual: the bond see-saw.

The bond see-saw is a quick way to keep the price/yield relationships straight. Many test-takers memorize it and rewrite it on scratch paper at the start of the exam so they can answer most yield relationship questions without doing full calculations.

NASAA tends to focus more on whether you understand which yield is higher or lower, rather than whether you can compute every yield from scratch. You may still be asked to calculate current yield, but the order of yields and how they move with price is usually more important. Knowing the order also helps you eliminate incorrect answer choices on yield questions.

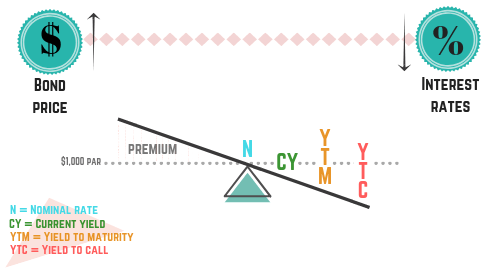

Premium bond yield relationships

Now let’s use the premium bond example from the previous sections.

A 10-year, $1,000 par, 4% bond is trading at $1,100. The bond is callable at par after 5 years.

-

Coupon = 4%

-

Current yield = 3.6%

-

YTM = 2.9%

-

YTC = 1.9%

Again, this order follows a consistent pattern. For a premium bond, the yields line up like this (from lowest to highest):

- YTC

- YTM

- Current yield

- Coupon

You can calculate each yield, or you can use the bond see-saw.

Just like with discount bonds, the see-saw gives you a clear visual of the yield relationships. Here, the price side points upward because premium bonds trade above par. If you remember the yield order shown on the see-saw, yield-based questions become much more straightforward.

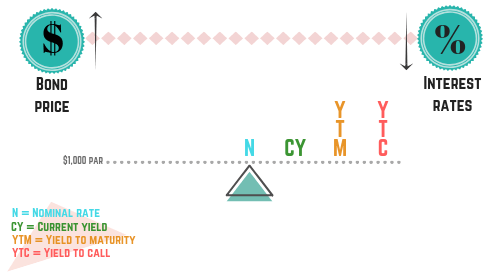

Yield for par bonds

We’ve seen how price affects yields for bonds purchased at a discount and at a premium. What happens if a bond is purchased at par ($1,000)?

This case is simple: when a bond is purchased at par, all yields equal the coupon.

The investor doesn’t gain or lose money from the purchase price. If the bond is bought at par ($1,000), it matures at par ($1,000). The only return comes from the coupon payments. For a par bond, the see-saw looks like this:

Here, the coupon sits at the same level as current yield, YTM, and YTC. If you see a question about yields on a par bond, keep it simple: they’re all the same.

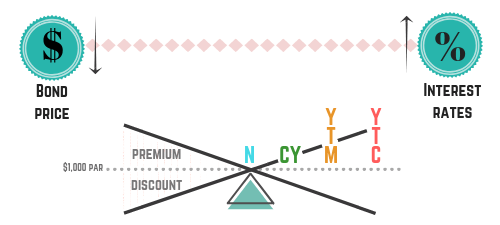

The bond see-saw

Yield is a major topic on the Series 66 exam, and the bond see-saw is a useful way to visualize the relationship between bond prices, interest rate changes, and yields. We’ve looked at the see-saw for discount, premium, and par bonds. Here they are together:

If you plan to use a “dump sheet,” this is a strong candidate to include. A dump sheet is a set of key visuals or reminders you write on scratch paper after the exam begins. Many students memorize the bond see-saw so they can recreate it quickly and use it to answer yield questions.

Some test-takers also use acronyms, like this:

CYM Call

-

CY = Current Yield

-

M = yield to Maturity

-

Call = yield to Call

Use whatever memory tool helps you recall the terms and their order.